| Tweet |

Is a Fixer Upper Right for You?

Is a Fixer Upper Right for You?

Looking to buy a home but feeling like almost everything is out of reach? Here’s the thing. There’s still a way to become a homeowner, even when affordability seems like a huge roadblock – and it might be with a fixer upper. Let’s dive into why buying a fixer upper could be your ticket to homeownership and how you can make it work.

What Is a Fixer Upper?

A fixer upper is a home that’s in livable condition but needs some work. The amount of work varies by home – some may need cosmetic updates like wallpaper removal and new flooring, while others might require more extensive repairs like replacing a roof or updating plumbing.

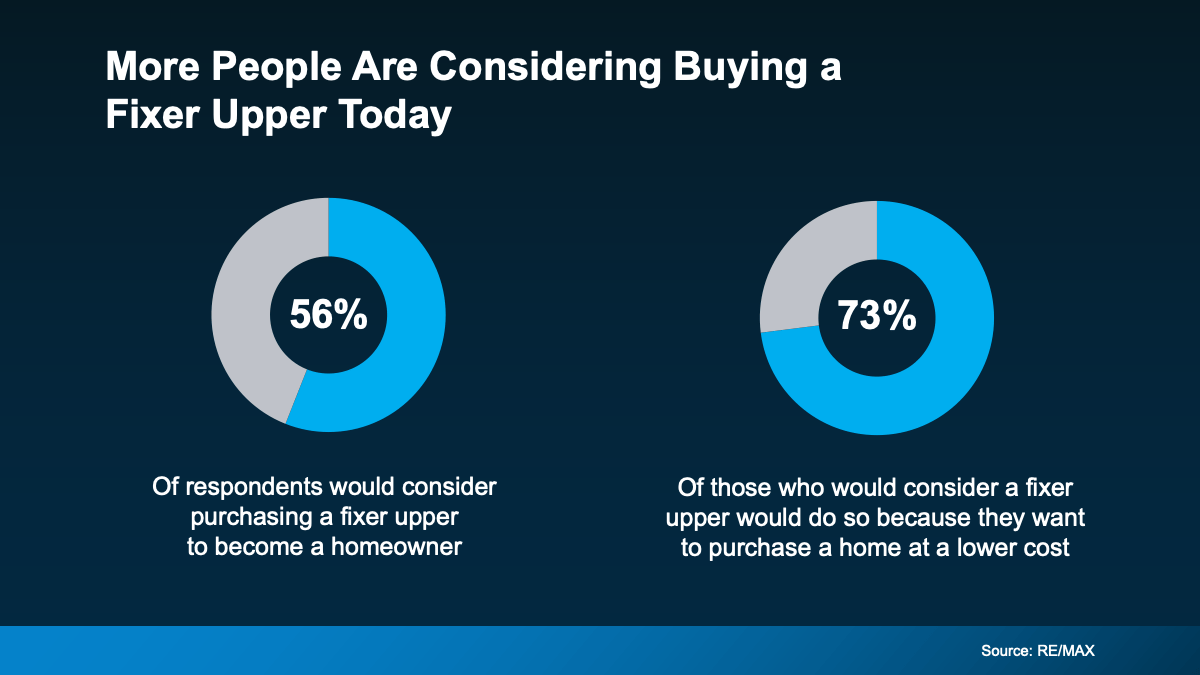

Because they need some elbow grease, these homes typically have a lower price point, based on local market value. In fact, a survey from StorageCafe explains that fixer uppers generally cost about 29% less than move-in-ready homes.

And that’s why, according to a recent survey, more buyers are considering homes that need a little extra work right now (see below):

If you’re looking for an option to get your foot in the door, and you’re willing to roll up your sleeves and do a bit of work, a house with untapped potential may be a good option.

If you’re looking for an option to get your foot in the door, and you’re willing to roll up your sleeves and do a bit of work, a house with untapped potential may be a good option.

Tips for Buying a Home That Needs Some Work

Before you buy a home that may need a makeover, here are a few things to keep in mind:

- Choose a Good Location: You can repair a house, but you can’t change where it is. Make sure the home is in a neighborhood you like or one with increasing property values and a growing number of local amenities. This way, even after you spend money fixing it up, the house will be worth more later.

- Budget for Surprises: Fixing up a house can take more time and money than you might think. Make sure you save room in your budget for unexpected repairs or other unknowns that might come up while you’re working on the house.

- Get a Home Inspection: Before you buy, hire an inspector to check out the house. They’ll help you determine the necessary repairs, so you don’t end up with expensive surprises later.

- Plan Your Priorities: When deciding what to tackle first, it helps to categorize your goals. Think of your home in three ways: the must-haves (essential repairs), the nice-to-haves (upgrades that would make life easier), and the dream-state features (luxuries you can add later). This will help you prioritize and stick to your budget.

Remember, the perfect home is the one you perfect after buying it. By starting with a fixer upper, you have the opportunity to customize a home to your liking while saving money on the initial purchase price. With careful planning, budgeting, and a little bit of vision, you can turn a house that needs some love into your perfect home.

Real estate agents are great at finding homes with potential. They know the local market and can guide you to homes where smart upgrades can add value. With their help, you’re more likely to find a house that fits your total budget and has room for worthwhile improvements.

Bottom Line

In today’s market, where the cost of homeownership can be intimidating, finding a move-in-ready home that fits your budget can feel like a real challenge. But if you’re open to putting in a little work, you can transform a fixer upper into your ideal home over time. Let’s explore what’s possible and find a place that’ll work for you.

Avoid These Top Homebuyer Mistakes in Today’s Market

Avoid These Top Homebuyer Mistakes in Today’s Market

No one likes making mistakes, especially when they happen in what’s likely the biggest transaction of your life – buying a home.

That’s why partnering with a trusted agent is so important. Here’s a sneak peek at the most common missteps buyers are making in today’s market and how a great agent will help you steer clear of each one.

Trying To Time the Market

Many buyers are trying to time the market by waiting for home prices or mortgage rates to drop. This can be a really risky strategy because there’s so much at play that can have an impact on those things. As Elijah de la Campa, Senior Economist at Redfin, says:

“My advice for buyers is don’t try to time the market. There are a lot of swing factors, like the upcoming jobs report and the presidential election, that could cause the housing market to take unexpected twists and turns. If you find a house you love and can afford to buy it, now’s not a bad time.”

Buying More House Than You Can Afford

If you’re tempted to stretch your budget a bit further than you should, you’re not alone. A number of buyers are making this mistake right now.

But the truth is, it’s actually really important to avoid overextending your budget, especially when other housing expenses like home insurance and taxes are on the rise. You want to talk to the pros to make sure you understand what’ll really work for you. Bankrate offers this advice:

“Focus on what monthly payment you can afford rather than fixating on the maximum loan amount you qualify for. Just because you can qualify for a $300,000 loan doesn’t mean you can comfortably handle the monthly payments that come with it along with your other financial obligations.”

Missing Out on Assistance Programs That Can Help

Saving up for the upfront costs of homeownership takes some careful planning. You’ve got to think about your closing costs, down payment, and more. And if you don’t work with a team of experienced professionals, you could miss out on programs out there that can make a big difference for you. This is happening more than you realize.

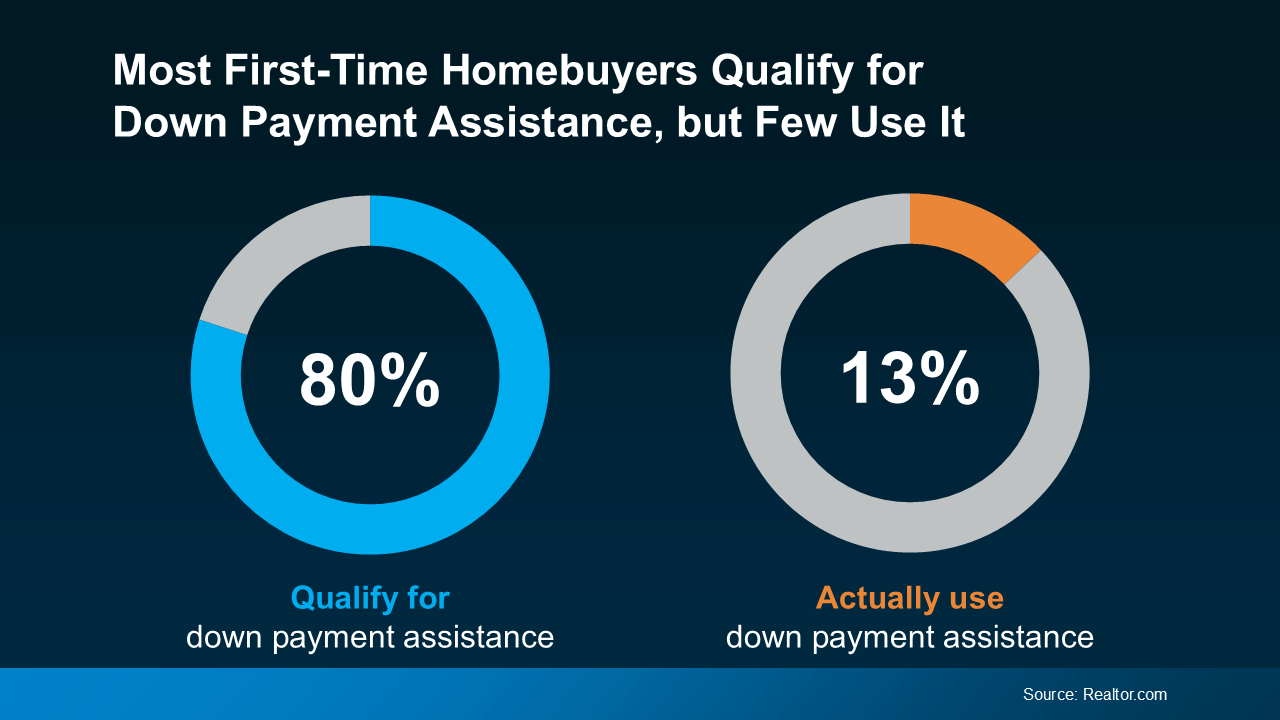

According to Realtor.com, almost 80% of first-time buyers qualify for down payment assistance – but only 13% actually take advantage of those programs. So, talk to a lender about your options. Whether you’re buying your first house or your fifth, there may be a program that can help.

Not Leaning on the Expertise of a Pro

This last one may be the most important of all. The very best way to avoid making a mistake that’s going to cost you is to lean on a pro. With the right team of experts, you can easily dodge these missteps.

Bottom Line

The good news is you don’t have to deal with any of these headaches. Let’s connect so you have a pro on your side who can help you avoid these costly mistakes.

Why an Agent Is Essential When Buying a Newly Built Home

Why an Agent Is Essential When Buying a Newly Built Home

For some buyers, there’s a misconception that newly built homes aren’t made to last or fall short of the quality you can find in older homes. Unfortunately, this is turning some buyers away from what may be one of their best options in today’s housing market. As Builder Online says:

“As resale inventory remains limited and the price spread between new and resale homes narrows, new homes are increasingly an attractive value proposition for buyers, with incentives such as rate buydowns a way to help address ongoing affordability challenges.”

So, is there any merit to the myth? Let’s break down the best way to make sure you feel good about looking into new home construction. That way, you’re not missing out on such a great option today.

Choosing the Right Builder

The key to making sure you get a quality newly built home is to choose a good builder. Reputable builders adhere to strict building codes and standards, use advanced construction techniques, and often offer warranties that cover structural issues for several years. That’s why the Mortgage Reports offers this advice:

“When embarking on the journey of buying a new construction home, one of the most important steps is selecting the right builder. This decision can significantly impact the quality and satisfaction you derive from your new home.”

And while you could dig into research about all the builders in your area, there’s an easier option to get the job done: lean on a pro. When you work with a local real estate agent, they already know about the builders and the new home communities under construction in your area.

Beyond that, maybe they’ve even worked with other buyers who opted for a home in one of those neighborhoods. Here are just a few of the things your agent will help you with:

1. The Builder’s Reputation: Your agent will help point you toward builders with strong reputations and positive reviews from previous buyers. Additionally, your agent will make sure the builder is licensed and insured. Membership in professional organizations, such as the National Association of Home Builders (NAHB), is also a good sign of a builder’s commitment to industry standards.

2. Their Model Homes: Your agent will also be able to tell you if the builders have model homes you can tour. And when your agent walks through the model with you, they’ll draw your attention to the little details that matter most. Things like the quality of finishes, layout, and overall feel of the home.

3. Builder Warranties: Your agent will also be able to help you navigate any builder offers or incentives. Reputable builders often provide warranties to cover major structural elements of the home for a significant period of time. This is a testament to their confidence in the quality of their construction.

4. Getting Inspections: Even with new homes, inspections are crucial. Your agent will coordinate the inspections with licensed professionals to ensure the home meets safety and quality standards before you move in.

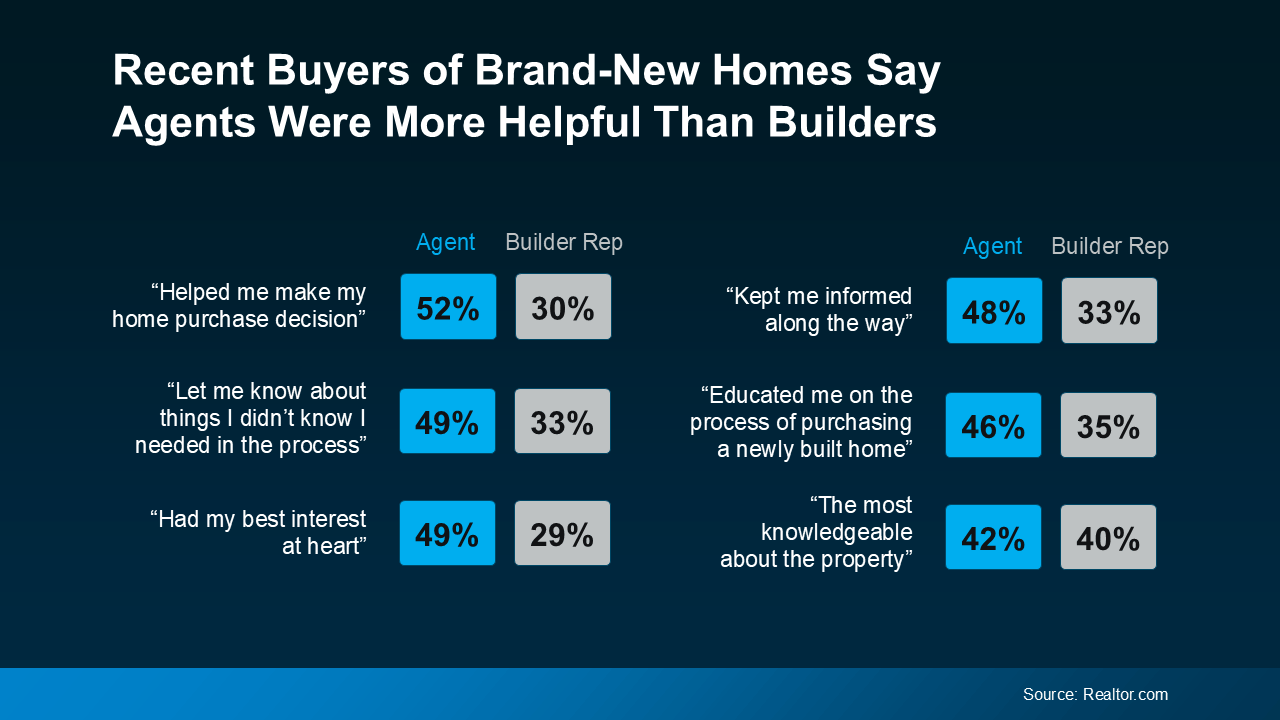

Agents Are the MVP When You’re Buying a Brand-New Home

Maybe that’s why data shows homebuyers unanimously scored their agents higher than their builders when looking back on their recent purchase:

So, you don’t need to worry that they just don’t make them like they used to. By working with a knowledgeable real estate agent to choose a reputable builder, you can feel confident when buying a newly built home today. As Realtor.com says:

So, you don’t need to worry that they just don’t make them like they used to. By working with a knowledgeable real estate agent to choose a reputable builder, you can feel confident when buying a newly built home today. As Realtor.com says:

“If you are interested in buying a new construction . . . You need your own real estate agent from the get-go. Even if it seems like plug and play to sign up with the builder’s on-site agent, you’re going to want someone representing your side of the deal.”

Bottom Line

If you’re considering buying a brand-new home, don’t let misconceptions hold you back. Let’s work together to find a home you’ll love and be proud to call your own.

Why a Condo Could Be Your Perfect First Home

Why a Condo Could Be Your Perfect First Home

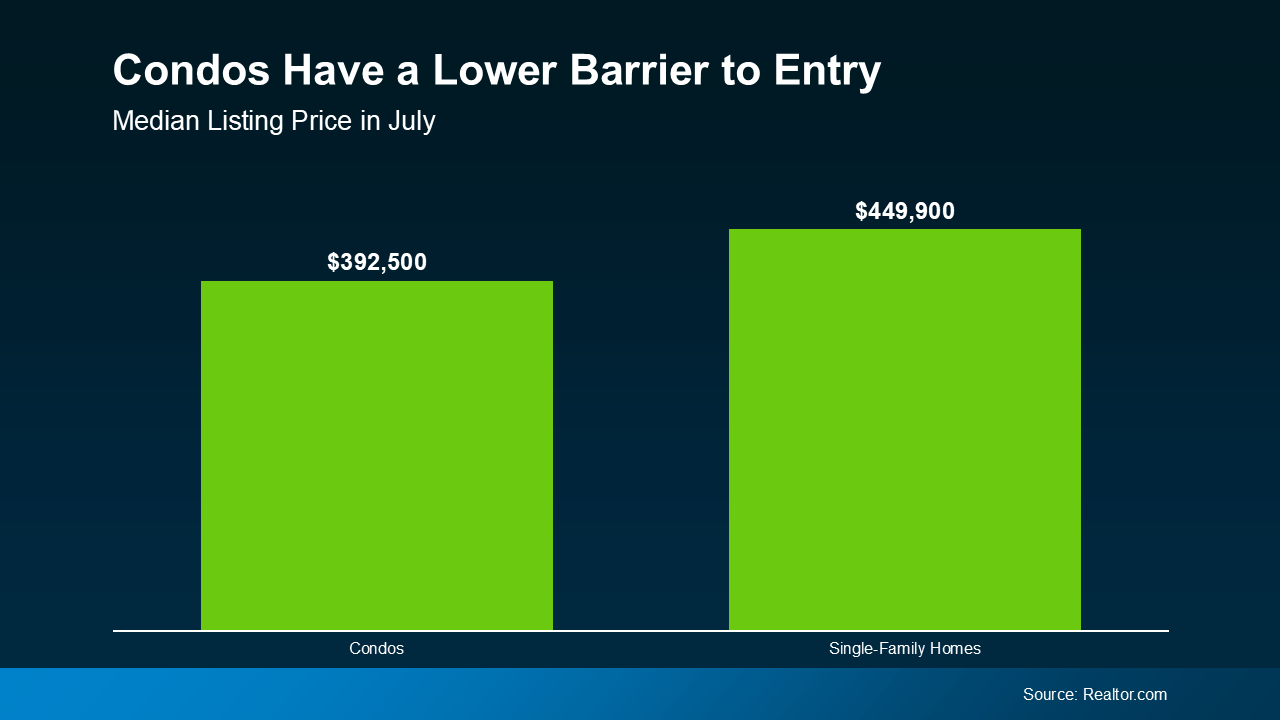

If you’re looking to break into homeownership but the price of single-family homes has you second-guessing, you might want to consider a condominium (condo) or townhome. These types of homes often come with a lower barrier to entry – and that can help you start to build equity and enjoy the benefits of owning a home sooner.

Since they’re usually smaller than single-family homes, they can be easier on your wallet. While it’s not always the case, smaller square footage usually comes with a smaller price tag too. As a result, according to the latest data from Realtor.com, condos typically have a lower asking price than single-family homes (see graph below):

And here’s some exciting news: builders are focusing more on homes like these. The National Association of Home Builders (NAHB) says:

And here’s some exciting news: builders are focusing more on homes like these. The National Association of Home Builders (NAHB) says:

“The share of townhomes being built is at an all-time high.”

That means there’s a good number of options to add to your home search if you broaden it to include condos and townhomes. And you may even find something that works better for your budget.

So, if you’re comfortable with a smaller space and want to buy your first home before the spring rush, adding these types of homes to your search might be your answer.

The Perks of a Condo Lifestyle

Living in a condo has a bunch of other perks, too. Let’s look closer at why condos are appealing for first-time buyers:

- They help you start building equity. When you buy a condo or townhome, you build equity and your net worth as you make your mortgage payments and as your condo’s value goes up over time.

- They can be low maintenance. Condos are great if you want to own your place but don’t want to mow the lawn, shovel snow, or fix the roof. Your real estate agent can help explain any associated fees and details for the condos you’re interested in.

- They usually come with a range of amenities. Your condo might come with access to a pool, dog park, or parking. And the best part? You don’t have to take care of any of them.

- They create a sense of community. Buying a condo means you’ll be living close to other people, which is nice if you want a more close-knit feel. Many communities like these hold fun events such as barbecues and parties to help create that sense of connection among residents.

Remember, your first home doesn’t have to be the one you stay in forever. The important thing is to get your foot in the door as a homeowner so you can start to gain home equity. Later on, that equity can help you buy another place if you want something different.

Ultimately, owning and living in a condo or townhome is a lifestyle choice. If you want to see if it makes sense for you, talk to a local real estate agent.

Bottom Line

Ready to find a home that suits your goals? A condo might be the perfect fit for your first home purchase. Let’s connect today to start your search.

Two Reasons Why the Housing Market Won’t Crash

Two Reasons Why the Housing Market Won’t Crash

You may have heard chatter recently about the economy and talk about a possible recession. It’s no surprise that kind of noise gets some people worried about a housing market crash. Maybe you’re one of them. But here’s the good news – there’s no need to panic. The housing market is not set up for a crash right now.

Real estate journalist Michele Lerner says:

“A housing market crash happens when home values plummet due to a lack of demand for homes or an oversupply.”

With that definition in mind, here are two reasons why this just isn’t on the horizon.

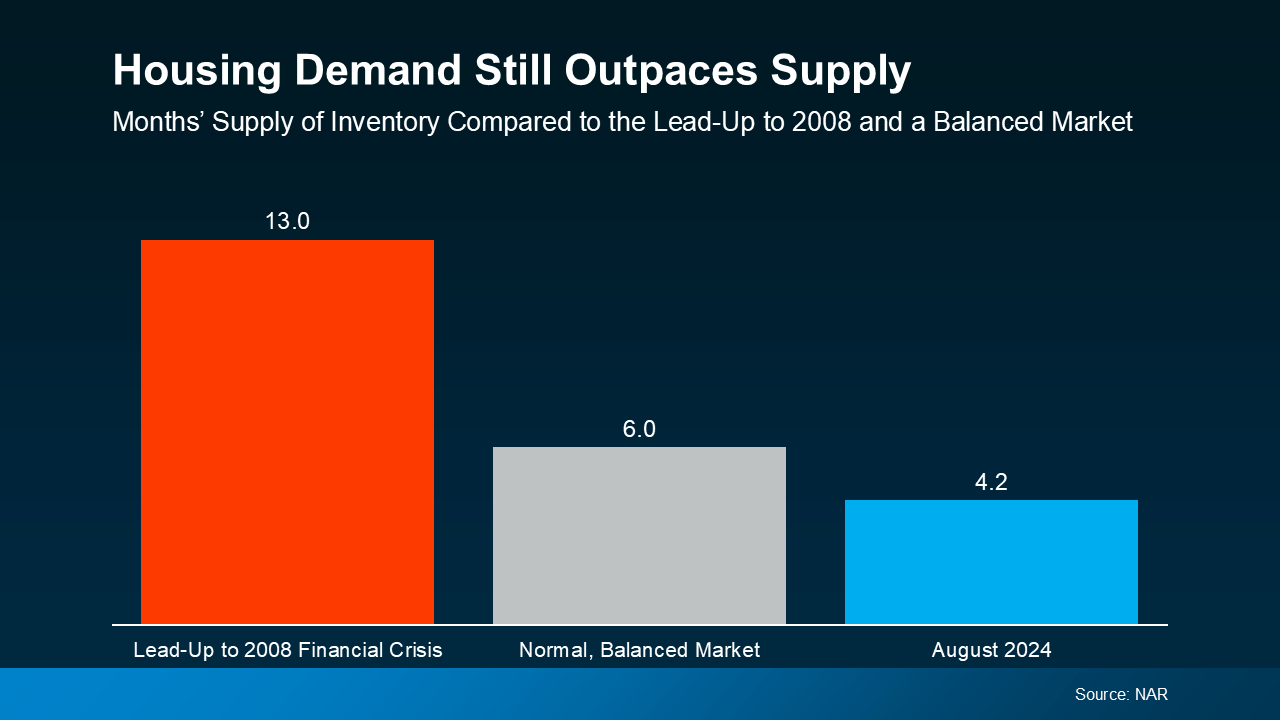

1. Demand for Homes Is Higher than Supply

One of the biggest reasons the housing market crashed back in 2008 was an oversupply of homes. Today, though, it’s a very different story.

It’s a general rule of thumb that a market where supply and demand are balanced has a six-month supply of homes. A higher number means supply outpaces demand, and a lower number means demand outpaces supply. The graph below uses data from NAR to put today’s situation into context:

The graph compares housing supply during three different periods of time. The red bar shows there were 13 months of supply before the 2008 crisis, which was far too much. The gray bar shows a balanced market with six months of supply, for context. And the blue bar shows there are only 4.2 months of supply today.

The graph compares housing supply during three different periods of time. The red bar shows there were 13 months of supply before the 2008 crisis, which was far too much. The gray bar shows a balanced market with six months of supply, for context. And the blue bar shows there are only 4.2 months of supply today.

Put simply, there are more people who want to buy homes than there are homes available to buy right now. So, demand is greater than supply. When that happens, home prices stay steady or rise – the opposite of a housing market crash.

It’s important to note that inventory levels differ from market to market. Some areas may be more balanced, while a few could have a slight oversupply, which can impact prices locally. However, most markets continue to experience a shortage of homes.

Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), says:

“We simply don’t have enough inventory. Will some markets see a price decline? Yes. [But] with the supply not being there, the repeat of a 30 percent price decline is highly, highly unlikely.”

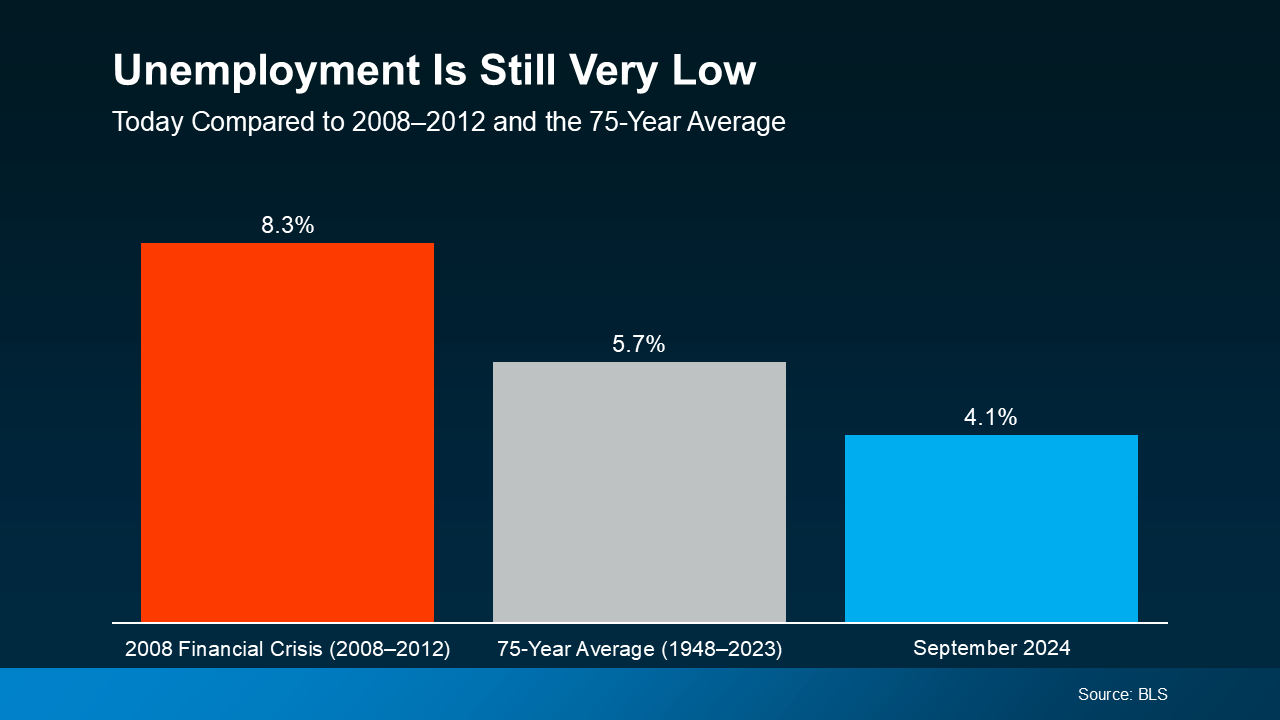

2. Unemployment Is Still Low

When people are unemployed, they’re more likely to have trouble making their mortgage payments and may be forced to sell or face foreclosure. That was a big problem during the 2008 financial crisis. Today, the employment situation is much more stable (see graph below):

Again, this graph shows three different periods of time, but this one is the unemployment rate. The red bar represents the 2008 financial crisis when unemployment was very high at 8.3%. The gray bar shows the 75-year average of 5.7%. And the blue bar shows the unemployment rate today, and it’s much lower at just 4.1%.

Again, this graph shows three different periods of time, but this one is the unemployment rate. The red bar represents the 2008 financial crisis when unemployment was very high at 8.3%. The gray bar shows the 75-year average of 5.7%. And the blue bar shows the unemployment rate today, and it’s much lower at just 4.1%.

Right now, people are working, earning an income, and making their mortgage payments. That’s one reason why the wave of foreclosures that happened in 2008 isn’t going to happen again this time. Plus, since so many people are employed right now, many are actually in a position to buy a home, and this demand keeps upward pressure on prices.

Today’s Housing Market Is Stronger than in 2008

While it’s understandable to be concerned when you hear talk of a recession and economic uncertainty, but know this: the housing market is in a much better place than it was in 2008. According to Rick Sharga, Founder and CEO at CJ Patrick Company:

“Literally everything is different about today’s housing market dynamics than the conditions that led to the housing crisis.”

Demand for homes still outpaces supply, and unemployment remains low. And these are two key factors that will help prevent the housing market from crashing any time soon.

Bottom Line

The housing market is doing a lot better than it was in 2008, but it’s important to remember that real estate is very local.

So, it’s always a good idea to stay informed about our specific market. If you have any questions or want to discuss how these factors are playing out in our area, feel free to reach out.

This Is the Sweet Spot Homebuyers Have Been Waiting For

This Is the Sweet Spot Homebuyers Have Been Waiting For

After months of sitting on the sidelines, many homebuyers who were priced out by high mortgage rates and affordability challenges finally have an opportunity to make their move. With rates trending down, today’s market is a sweet spot for buyers—and it’s one that may not last long.

So, if you’ve put your own move on the back burner, here’s why maybe you shouldn’t delay your plans any longer.

As you weigh your options and decide if you should buy now or wait, ask yourself this: What do you think everyone else is going to do?

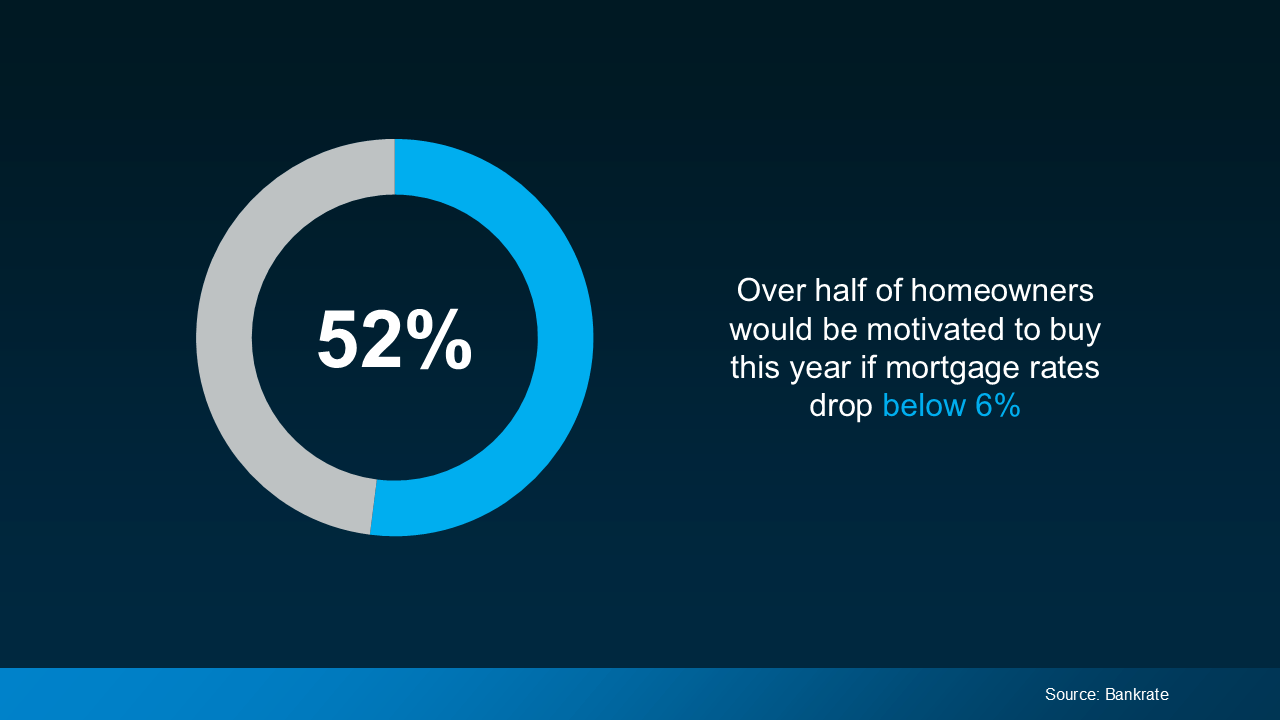

The truth is, if mortgage rates continue to ease, as experts project, more buyers will jump back into the market. A survey from Bankrate shows over half of homeowners would be motivated to buy this year if rates drop below 6% (see graph below):

With rates already in the low 6% range, we’re not terribly far off from hitting that threshold. The bottom line is, that when they drop into the 5s, the number of buyers in the market is going to go up – and that means more competition for you.

With rates already in the low 6% range, we’re not terribly far off from hitting that threshold. The bottom line is, that when they drop into the 5s, the number of buyers in the market is going to go up – and that means more competition for you.

That increased demand will likely push home prices up, which could potentially take away from some of the benefits you’d gain from a slightly lower interest rate. As Nadia Evangelou, Senior Economist and Director of Real Estate Research at the National Association of Realtors (NAR), explains:

“The downside of increased demand is that it puts upward pressure on home prices as multiple buyers compete for a limited number of homes. In markets with ongoing housing shortages, this price increase can offset some of the affordability gains from lower mortgage rates.”

So, while waiting to buy may seem like a smart move, it could backfire if rising prices outpace your savings from slightly lower rates.

What This Means for You

Right now, you’ve got the chance to get ahead of all of that. Today’s market is a buyer sweet spot. Why? Because a lot of other buyers are waiting – which means not as many people are actively looking for homes. That means less competition for you.

At the same time, affordability has already improved quite a bit. Recent easing in mortgage rates has made homeownership more accessible. As Mike Simonsen, Founder of Altos Research, says:

“Mortgage payments on the typical-price home are 7% lower than last year and are 13% lower than the peak in May 2024.”

And while the supply of homes for sale is still low, it’s also higher than it’s been in years. According to Ralph McLaughlin, Senior Economist at Realtor.com:

“The number of homes actively for sale continues to be elevated compared with last year, growing by 35.8%, a 10th straight month of growth, and now sits at the highest since May 2020.”

This means you now have more options to choose from than you’ve had in quite a while.

With fewer buyers in the market, improving affordability, and more homes to choose from, you have the chance to find the right one before the competition heats up.

Why Waiting Could Cost You

If you’re waiting for the perfect time to buy, it’s important to understand that timing the market is nearly impossible. The longer you wait, the higher the risk that market conditions will shift—and not necessarily in your favor. As Greg McBride, Chief Financial Analyst at Bankrate, says:

“It’s one of those things where you should be careful what you wish for. A further drop in mortgage rates could bring a surge of demand that makes it tougher to actually buy a house.”

Bottom Line

Don’t wait until you have to deal with more competition and higher prices – you already have the chance to buy a home while we’re in the sweet spot today. Let’s connect to make sure you’re taking advantage of it.

Why Buying Now May Be Worth It in the Long Run

Why Buying Now May Be Worth It in the Long Run

Should you buy a home now or should you wait? That’s a question a lot of people have these days. And while what’s right for you is going to depend on a lot of different factors, here’s something you’ll want to consider as you make your decision.

As soon as you buy, you’ll start gaining equity. And you’d be surprised how quickly that can add up – even with more moderate home price appreciation.

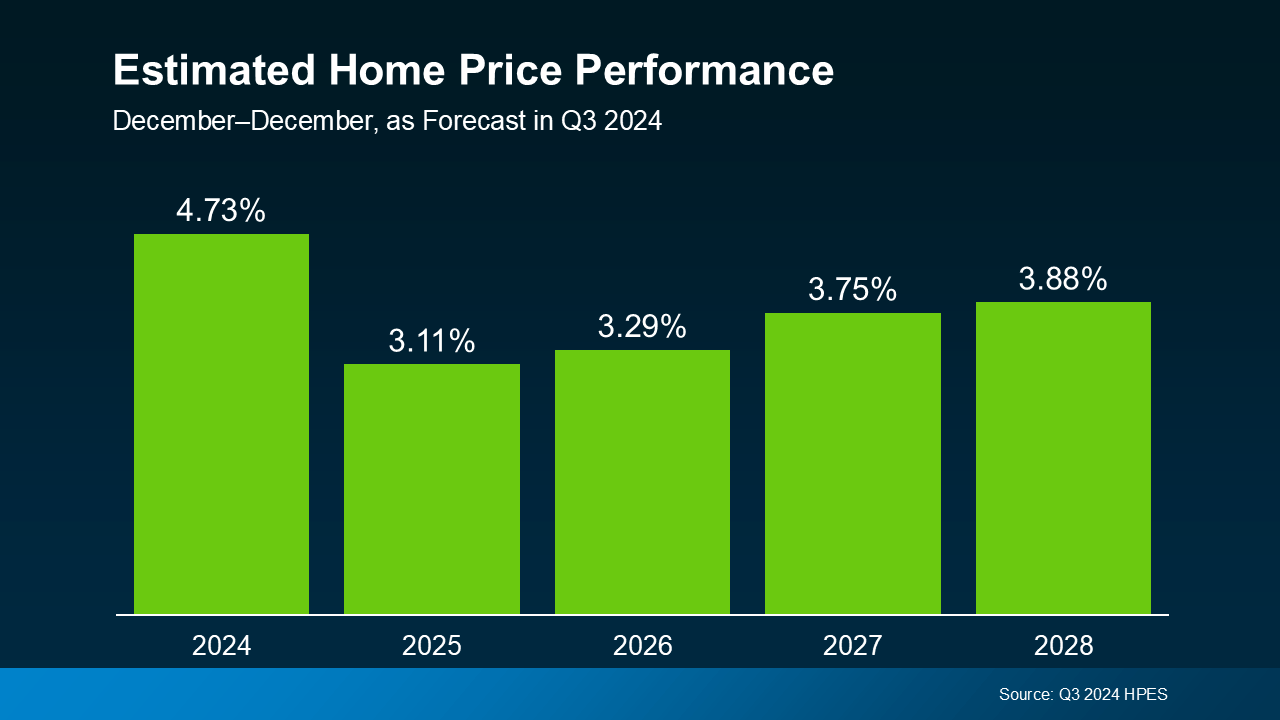

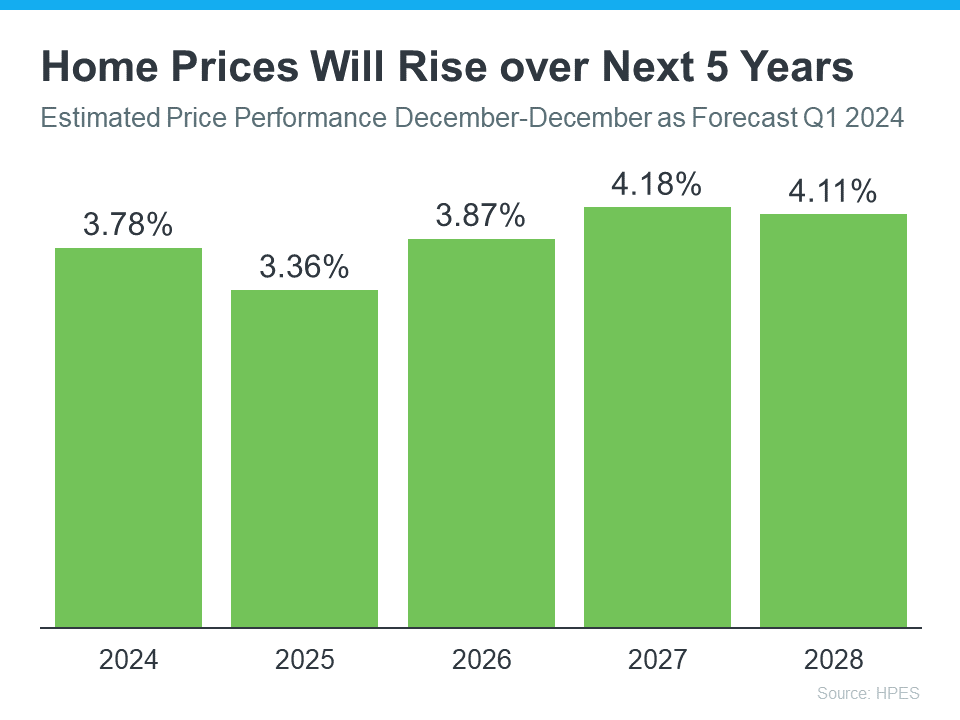

Each quarter, Fannie Mae releases the Home Price Expectations Survey. It asks over one hundred economists, real estate experts, and investment and market strategists what they forecast for home prices over the next five years. In the latest release, experts project prices will continue to rise nationally through at least 2028 (see the graph below):

While home prices are going to vary from one local area to the next, this shows they’re expected to keep going up nationally. The size of the increase varies from year-to-year, but the important takeaway is that prices are forecast to rise every single year – just at a moderate pace.

While home prices are going to vary from one local area to the next, this shows they’re expected to keep going up nationally. The size of the increase varies from year-to-year, but the important takeaway is that prices are forecast to rise every single year – just at a moderate pace.

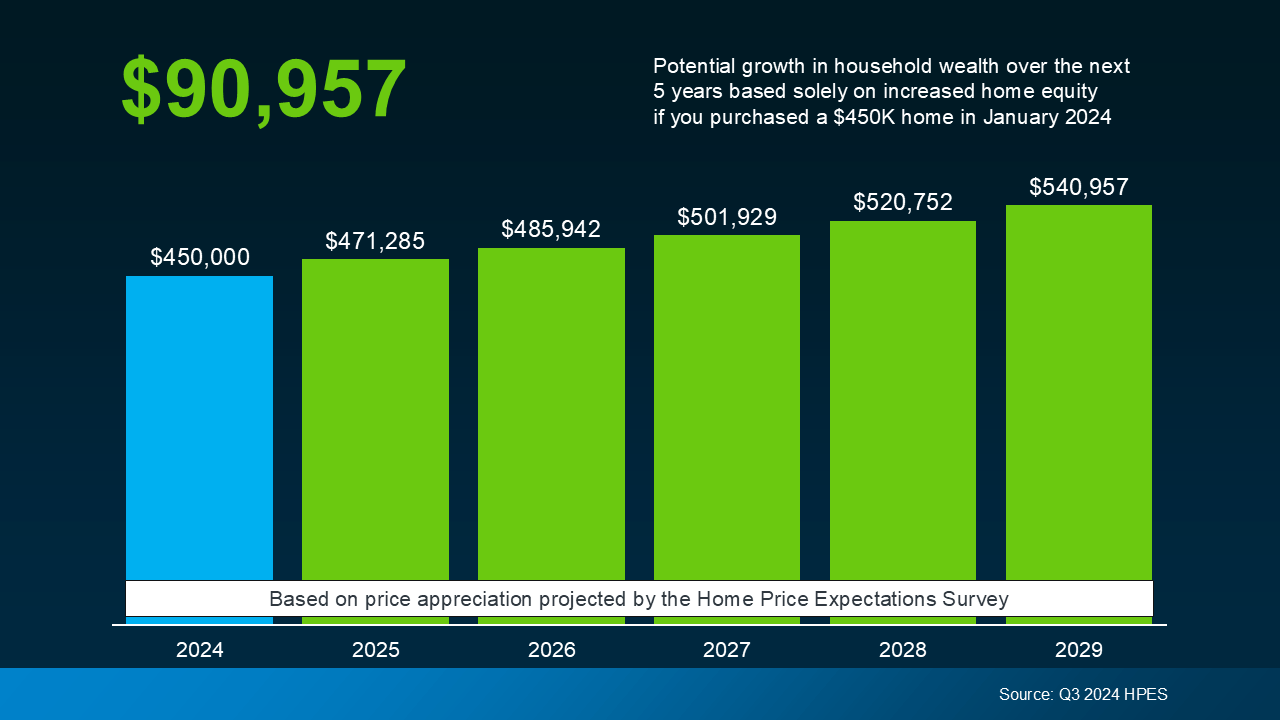

And while rising home prices may not sound great right now, once you own a home, that growth will be a big bonus for you. Here’s a look at what you stand to gain equity-wise once you buy. The graph below uses a typical home’s value and those HPES projections to show how much equity is at stake:

If you bought a $450,000 home at the beginning of this year, based on that starting value and the expert forecasts from the HPES, you could gain more than $90,000 in household wealth over the next five years. That’s significant.

If you bought a $450,000 home at the beginning of this year, based on that starting value and the expert forecasts from the HPES, you could gain more than $90,000 in household wealth over the next five years. That’s significant.

So, if you’re ready and able to buy, and growing your wealth is important to you, you’ve got an opportunity in front of you. And now that mortgage rates have fallen, it may be time to consider making a move.

To talk more about your options and what makes sense, lean on a pro. They’ll be able to tell you what home prices are doing in your area and what that means for your move (and your future equity). The Mortgage Reports says:

“Given the intricacies of the current market, it’s more important than ever to stay informed and up to date about housing market conditions. Whether you’re looking to buy or sell in the remaining months of 2024, having a professional guide you through the process can make all the difference.”

Bottom Line

The decision to buy now or wait is a very personal one, but it’s valuable to have an expert’s perspective. They won’t push you, but they will explain things you may not have considered, like the equity that’s at stake.

If you want help weighing your options and thinking through how the current market factors in, let’s connect.

The Down Payment Assistance You Didn’t Know About

The Down Payment Assistance You Didn’t Know About

Believe it or not, almost 80% of first-time homebuyers qualify for down payment assistance, but only 13% actually use it. And if you’re hoping to buy a home, this is a mission-critical gap to close – fast (see graph below):

Here’s what you need to know to make the most of your down payment in today’s housing market.

Here’s what you need to know to make the most of your down payment in today’s housing market.

Amplify Your Down Payment Potential

For first-time buyers, the name of the game with down payments is making sure you’re taking advantage of all the resources out there designed to help you. And a bunch of them can get you to your goal faster than you may have thought possible.

For example, there are loan options that require as little as 3% down, or even 0% for certain qualified borrowers, like Veterans. And let’s not forget down payment assistance, like grants and other opportunities, that help you cover the upfront cost of your down payment.

If you’re interested in exploring those options and what you may be able to use to your advantage, connect with a trusted lender. Because if you don’t at least see what’s available, you could be leaving money on the table and missing your chance at buying a home. These resources can boost your down payment. And a higher down payment could help lower your eventual monthly mortgage payment, and even avoid or reduce your fees like private mortgage insurance.

Don’t Let News Headlines About Down Payments Scare You

There’s one more thing to address. News coverage has been talking about how the typical down payment is rising. A report from Redfin states:

“The typical down payment for U.S. homebuyers hit a record high of $67,500 in June, up 14.8% from $58,788 a year earlier . . . This was the 12th consecutive month the median down payment rose year over year.”

But don’t let those high dollars scare you. Just because the average down payment is rising doesn’t mean down payment requirements are going up. That’s a key piece of the puzzle to understand. It’s really just because people are choosing to put more down to try to offset higher mortgage rates, and current homeowners who are putting their equity to work are using that to increase their down payment on their next home. As HousingWire explains:

“. . . buyers are putting down a higher percentage of the purchase price to lower their monthly mortgage payment. And buyers also had more equity from their home sales, which gives them more cushion.”

Let’s break those two reasons down a bit:

1. A bigger down payment helps lower your monthly mortgage payment. Affordability has been a challenge for many buyers recently, which is why those who have the ability to make a bigger down payment are going to do so in an effort to lower their future housing costs.

2. Buyers who already own a home have a record amount of equity to leverage. Someone who bought a home a few years ago has gained a significant amount of value in their house, thanks to home price appreciation. These people can put down much more than the average first-time buyer who hasn’t owned a home yet.

Bottom Line

What’s the best thing to do? Talk with a trusted lender about your options. They’ll help you figure out where you stand today and how to access the resources you may qualify for. Because help is out there, you just need to work with a pro to take advantage of it.

Falling Mortgage Rates Are Bringing Buyers Back

Falling Mortgage Rates Are Bringing Buyers Back

If you’ve been hesitant to list your house because you’re worried no one’s buying, here’s your sign it may be time to talk with an agent.

After months of high rates keeping buyers on the sidelines, things are starting to shift. Rates are already coming down due to a number of economic factors. And yesterday the Federal Reserve cut the Federal Funds Rate for the first time since they began raising that rate in March 2022. And while they don’t control mortgage rates, this sets the stage for mortgage rates to fall even further than they already have – especially since more cuts from the Fed are expected into next year. And lower mortgage rates are bringing more buyers back into the market. Lisa Sturtevant, Chief Economist at Bright MLS, says:

“A drop in the cost of borrowing will help fuel more homebuyer demand . . . Falling rates will also bring more sellers into the market.”

The best part? You can take advantage of that renewed buyer interest.

As Rates Fall, Buyer Activity Goes Up

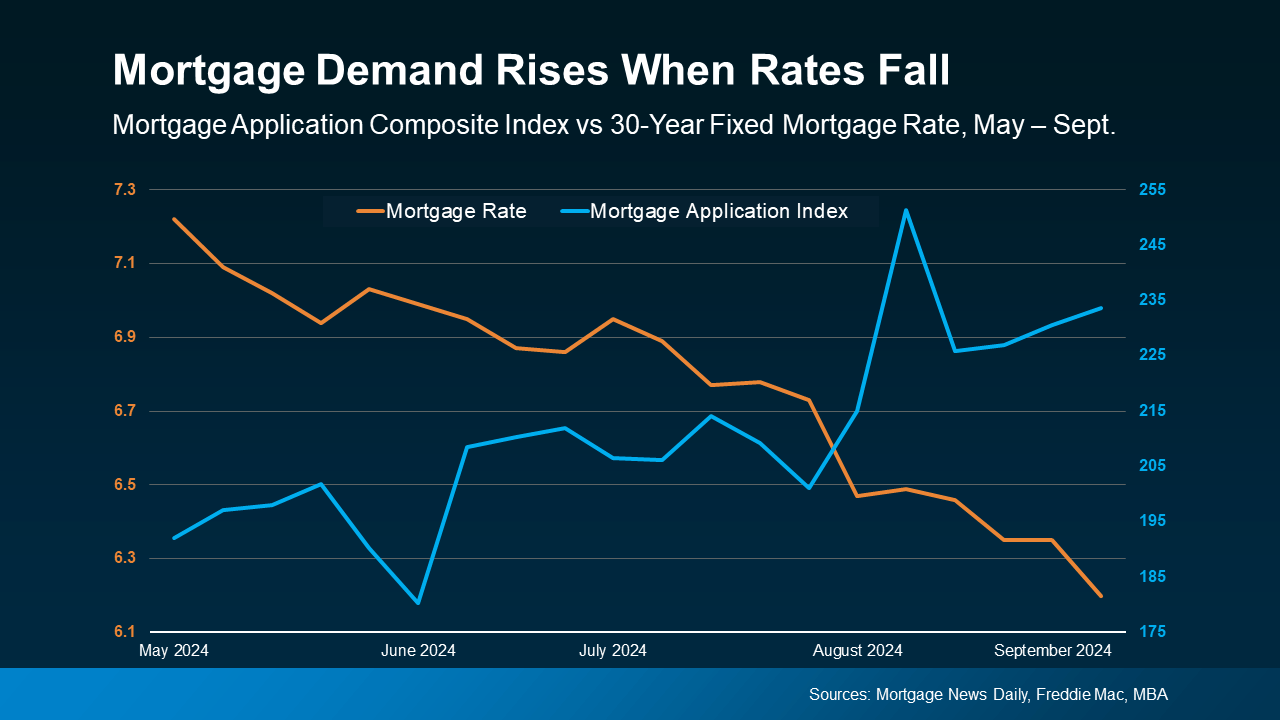

The graph below illustrates the relationship between falling mortgage rates and rising buyer activity. The orange line represents the average 30-year fixed mortgage rate, while the blue line shows the Mortgage Bankers Association (MBA) Mortgage Application Index, which tracks the number of mortgage applications.

As you can see, as mortgage rates (orange) come down, the Mortgage Application Index (blue) rises, showing more people start to re-engage in the process (see graph below):

What This Means for You

What This Means for You

What This Means for You

What This Means for YouAccording to the National Association of Realtors (NAR), home sales increased in July, which was a welcome shift after four straight months of declines. If you’re a homeowner thinking about selling, this uptick in buyer activity works in your favor.

More buyers means more competition, which can lead to higher offers and shorter time on the market for your house. And, according to Edward Seiler, AVP of Housing Economics at the Mortgage Bankers Association (MBA), this trend is expected to continue:

“MBA is expecting that slower home-price appreciation, coupled with lower rates, will ease affordability constraints and lead to increased activity in the housing market.”

All in all, the market is becoming more accessible to a wider range of buyers, which could result in even more people looking to purchase a house like yours.

With more buyers entering the market, now’s the time to start getting your house ready to sell.

Bottom Line

The recent decline in mortgage rates is already driving more buyers into the market, and experts project this trend will continue. Let’s work together to take advantage of this increased buyer demand and get your house ready to sell.

The Latest Builder Trend: Smaller, Less Expensive Homes

The Latest Builder Trend: Smaller, Less Expensive Homes

Even though affordability is improving, buying a home can still feel tough right now. But here’s some good news: builders are focusing their efforts on building smaller homes, and they’re offering key incentives to buyers. And both of these things can be a big help if you’re worried about finding a home that’s right for your budget.

Builders Are Building Smaller Homes

During the pandemic, homebuyers were looking for larger homes—and many could afford them. Builders responded to that demand and created bigger spaces to help people with things like working from home, setting up home gyms, and having extra rooms for virtual school.

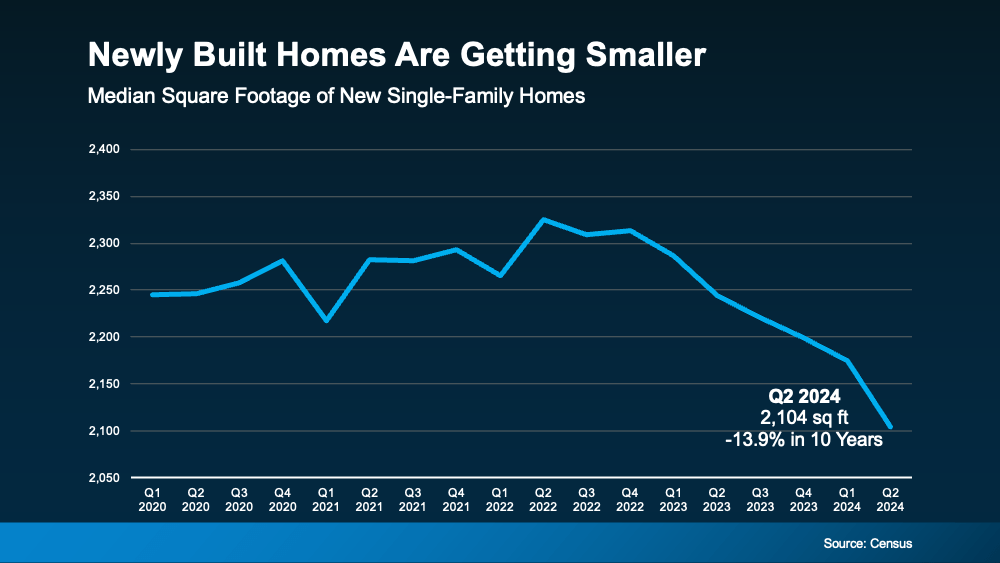

Now, with affordability as tight as it is, builders are turning their focus to smaller single-family homes. Data from the Census shows how significant this trend toward smaller new homes has been over the last couple of years (see graph below):

But why would builders want to build smaller homes right now? At the end of the day, builders are going to focus on building homes that meet current market demand – because they want to build what they know will sell. And the number one thing homebuyers are looking for right now is better affordability. Since smaller homes typically come with smaller price tags, both buyers and builders have shifted their focus to homes with less square footage. The National Association of Home Builders (NAHB) reports:

But why would builders want to build smaller homes right now? At the end of the day, builders are going to focus on building homes that meet current market demand – because they want to build what they know will sell. And the number one thing homebuyers are looking for right now is better affordability. Since smaller homes typically come with smaller price tags, both buyers and builders have shifted their focus to homes with less square footage. The National Association of Home Builders (NAHB) reports:

“. . . home buyers are looking for homes around 2,070 square feet, compared to 2,260 20 years ago.”

And according to Orphe Divounguy, Senior Economist at Zillow:

“Not only are cash-strapped buyers continually seeking out lower-cost options, but developers are changing what type and size of home they’re producing to try and meet that need.”

How a Newly Built Home Can Help You Achieve Your Homebuying Goals

So, if you’re having a hard time finding something in your budget, it may be time to look at brand-new homes that have a smaller footprint. When you do, you may get a few other fringe benefits that can help on the affordability front – like price reductions or mortgage rate buy-downs.

According to the most recent data from Zonda, more than half of builders are offering incentives, some of which are mortgage rate buydowns. And those perks could help lower your future monthly housing payment too. John Burns, CEO of John Burns Research & Consulting, shares:

“The monthly payment matters more than anything else and builders have responded with smaller, more efficient homes.”

Not to mention, with new home construction, you’ll also get brand new everything, have fewer maintenance needs, and get some of the latest features available. That’s worth looking into, right?

Bottom Line

With builders focusing on smaller homes, you may have more budget-friendly options when it matters most. If you’re thinking about buying a home soon, let’s connect and see what’s available where you want to live.

Mortgage Rates Drop to Lowest Level in over a Year and a Half

Mortgage Rates Drop to Lowest Level in over a Year and a Half

Mortgage rates have hit their lowest point in over a year and a half. And that’s big news if you’ve been sitting on the homebuying sidelines waiting for this moment.

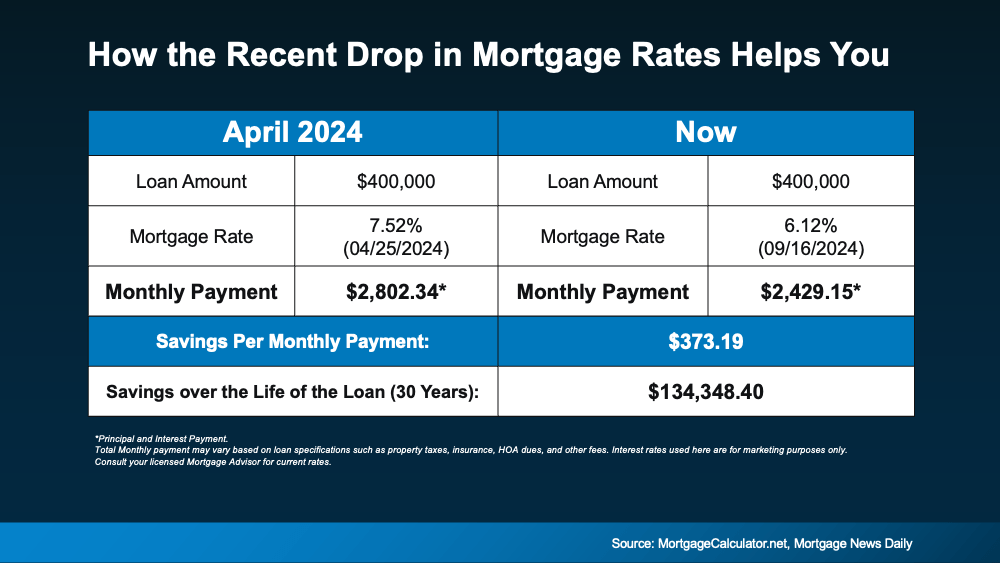

Even a small decline in rates could help you get a better monthly payment than you would expect on your next home. And the drop that’s happened recently isn’t small. As Sam Khater, Chief Economist at Freddie Mac, says:

“Mortgage rates have fallen more than half a percent . . . and are at their lowest level since February 2023.”

But if you want to see it to really believe it, here’s how the math shakes out. Take a closer look at the impact on your monthly payment.

The chart below shows what a monthly payment (principal and interest) would look like on a $400K home loan if you purchased a house back in April (this year’s mortgage rate high), versus what it could look like if you buy a home now (see below):

Going from 7.5% just a few months ago to the low 6s has a big impact on your bottom line. In just a few months’ time, the anticipated monthly payment on a $400K loan has come down by over $370. That’s hundreds of dollars less per month.

Going from 7.5% just a few months ago to the low 6s has a big impact on your bottom line. In just a few months’ time, the anticipated monthly payment on a $400K loan has come down by over $370. That’s hundreds of dollars less per month.

Bottom Line

With the recent drop in mortgage rates, the purchasing power you have right now is better than it’s been in almost two years. Let’s talk about your options and how you can make the most of this moment you’ve been waiting for.

The Best Time To Buy a Home This Year

The Best Time To Buy a Home This Year

A shift is underway in the housing market this season. And if you’ve been sitting on the sidelines waiting for the right moment to jump back into your homebuying search, this is a great time to do it. That’s because the best week to buy a home this year is just around the corner. Your sweet spot is here.

The experts at Realtor.com study seasonal trends to figure out the ideal week for homebuyers:

“Nationally, the best time to buy in 2024 is the week of Sept. 29–Oct. 5. This week historically has shown the best balance of market conditions that favor buyers. Inventory tends to be high, prices are below peak levels, demand is waning, and the pace of the market slows to a more manageable speed.”

In addition to the historical trends and typical seasonality that Realtor.com looks at, there are also clear indicators in today’s market data that you’ll see better conditions right now than you would have over the last few years.

Mortgage rates just hit their lowest point in 19 months, and that goes a long way to help with your purchasing power and affordability. Andy Walden with Intercontinental Exchange Inc. (ICE) points out:

“Recent easing in mortgage rates brought some much-sought relief to prospective homebuyers. Along with a general cooling in home price growth, rates falling below 6.5 percent made August the most affordable month for housing since February.”

And Ralph McLaughlin, Senior Economist at Realtor.com, explains that it’s not just rates that have improved – inventory has too:

“The number of homes actively for sale continues to be elevated compared with last year, growing by 35.8%, a 10th straight month of growth, and now sits at the highest since May 2020.”

That should give you more options. At the same time, sellers now have to compete with each other for your attention. That means they’ll be more likely to negotiate because they know their house will sit on the market longer if they don’t. As Zillow says:

“Buyers waiting on the sidelines could find that early fall presents a ‘sweet spot,’ where there’s less competition from other buyers, more motivated sellers and lower interest rates to finance their purchases.”

Bottom Line

If you want to make sure you’re ready to take advantage of this sweet spot, let’s connect and start the prep work now. Maybe it’s time to get off the sidelines and into the action.

Why Pre-Approval Should Be at the Top of Your Homebuying To-Do List

Why Pre-Approval Should Be at the Top of Your Homebuying To-Do List

Since the supply of homes for sale is growing and mortgage rates are coming down, you may be thinking it’s finally your moment to jump into the market. To make sure you’re ready, you need to get pre-approved for a mortgage.

That’s when a lender looks at your finances, including things like your W-2, tax returns, credit score, and bank statements, to figure out what they’re willing to loan you. After that process, you’ll get a pre-approval letter to show what you can borrow. Here are two reasons why this is essential in today’s market.

Pre-Approval Helps You Know Your Numbers

While home affordability is finally starting to show signs of improving, it’s still tight. So, it’s a good idea to talk to a lender about your loan options and how today’s changing mortgage rates will impact your monthly payment. The pre-approval process is the perfect time for that. In addition to determining the maximum amount you can borrow, pre-approval also helps you understand this piece of the puzzle. As Investopedia says:

“Consulting with a lender and obtaining a pre-approval letter allows you to discuss loan options and budgeting with the lender; this step can clarify your total house-hunting budget and the monthly mortgage payment you can afford.”

You should use this information to tailor your home search to what you’re actually comfortable with budget-wise. Since mortgage rates have inched down some lately, you may find you’re able to afford a bit more than you’d expect for your monthly payment, but you still want to avoid overextending. As CNET explains:

“In many cases, a lender may preapprove you for more than you need to spend on a home. And while it can be tempting to look at houses outside your budget, it won’t help you in the long run. Before you start touring homes, figure out how much you can realistically afford and stick to your budget.”

Pre-Approval Makes Your Offer More Appealing

And once you do find a home you want in your budget, pre-approval has another big perk. It not only makes your offer stronger, it also shows sellers you’ve already undergone a credit and financial check. When a seller sees you as a serious buyer, they may be more attracted to your offer because it seems more likely to go through. As Greg McBride, Chief Financial Analyst at Bankrate, says:

“Preapproval carries more weight because it means lenders have actually done more than a cursory review of your credit and your finances, but have instead reviewed your pay stubs, tax returns and bank statements. A preapproval means you’ve cleared the hurdles necessary to be approved for a mortgage up to a certain dollar amount.”

As mortgage rates trend down, more buyers are going to be ready to jump back into the market. And while demand is still limited right now, there’s the potential for competition to pick back up, especially in hot markets. So, why not stack the deck in your favor and make sure you’re putting yourself in the best position possible when you find a home you love?

Bottom Line

If you’re planning on buying a home, don’t forget to get pre-approved early in the process. It can help you get a more in-depth understanding of what you can borrow and shows sellers you mean business.

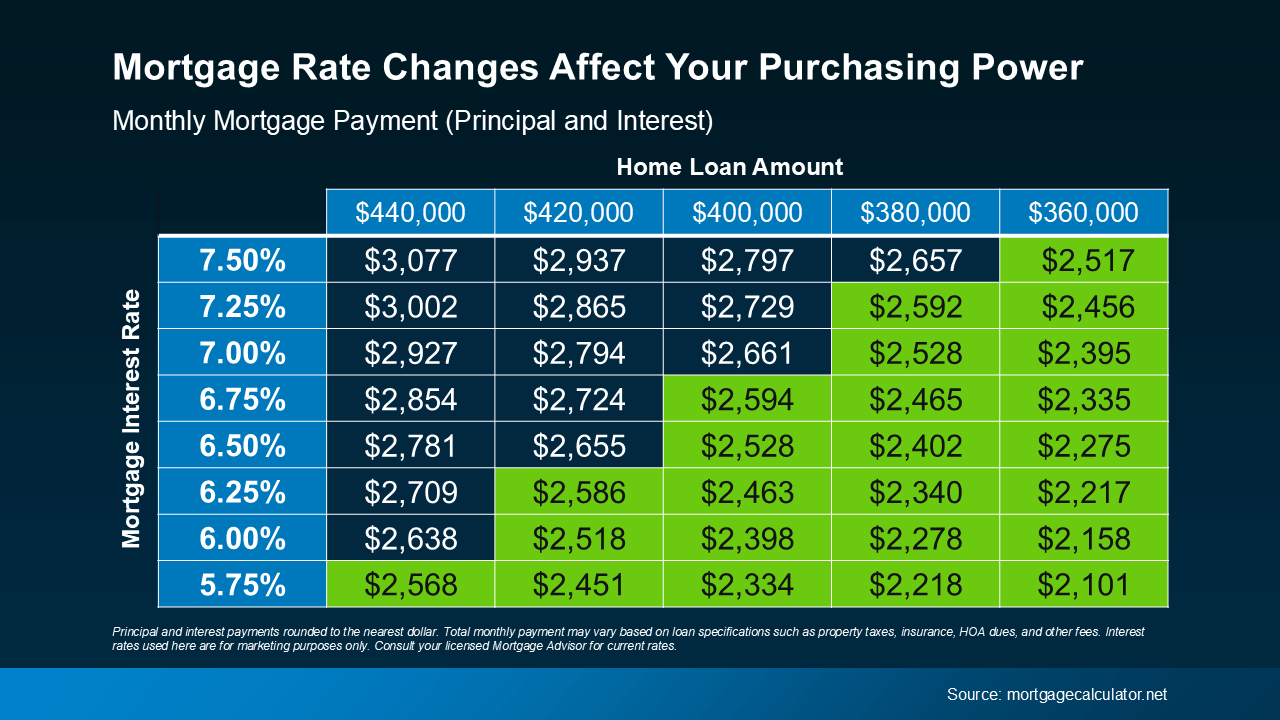

How Mortgage Rate Changes Impact Your Homebuying Power

How Mortgage Rate Changes Impact Your Homebuying Power

If you’re thinking about buying or selling a home, you’ve probably got mortgage rates on your mind. That’s because you’ve likely heard that mortgage rates impact how much you can afford in your monthly mortgage payment, and you want to factor that into your planning. Here’s what you need to know.

What’s Happening with Mortgage Rates?

Mortgage rates have been trending down recently. While that’s good news for your homebuying plans, it’s important to know that rates can be unpredictable because they’re affected by many factors.

Things like the economy, job market, inflation, and decisions made by the Federal Reserve all play a part. So, even as rates go down, they can still bounce around a bit based on new economic data. As Odeta Kushi, Deputy Chief Economist at First American, says:

“The ongoing deceleration in inflation, coupled with the Federal Reserve’s recent indication of potential rate cuts [in 2024], suggests an environment supportive of modest declines in mortgage rates. Barring any unforeseen circumstances and resurgence in inflation, lower mortgage rates could be on the horizon, but the journey towards them might be slow and bumpy.”

How Do These Changes Affect You?

When mortgage rates change, it affects how much you pay each month for your home loan. Even a small rate change can make a big difference to your monthly bill.

Take a look at the chart below to see how different mortgage rates impact your house payment each month for various loan amounts. Imagine you can afford a monthly payment of $2,600 for your home loan. The green part in the chart shows payments in that range or lower based on varying mortgage rates (see chart below):

Understanding how mortgage rates impact your payment helps you make better decisions.

Understanding how mortgage rates impact your payment helps you make better decisions.

How Can You Keep Track of the Latest on Rates?

Real estate agents have the expertise to help you understand what’s happening and what it means for you. They can provide tools and visuals, like the chart above, to show how rate changes impact your buying power.

You don’t need to be a mortgage expert; you just need a professional by your side. Someone who can help you make sense of the market and guide you through your homebuying or selling journey.

Bottom Line

If you have questions about the housing market, let’s connect. That way you’ll understand what’s going on and how to navigate it.

What Credit Score Do You Really Need To Buy a House?

What Credit Score Do You Really Need To Buy a House?

When you’re thinking about buying a home, your credit score is one of the biggest pieces of the puzzle. Think of it like your financial report card that lenders look at when trying to figure out if you qualify, and which home loan will work best for you. As the Mortgage Report says:

“Good credit scores communicate to lenders that you have a track record for properly managing your debts. For this reason, the higher your score, the better your chances of qualifying for a mortgage.”

The trouble is most buyers overestimate the minimum credit score they need to buy a home. According to a report from Fannie Mae, only 32% of consumers have a good idea of what lenders require. That means nearly 2 out of every 3 people don’t.

So, here’s a general ballpark to give you a rough idea. Experian says:

“The minimum credit score needed to buy a house can range from 500 to 700, but will ultimately depend on the type of mortgage loan you’re applying for and your lender. Most lenders require a minimum credit score of 620 to buy a house with a conventional mortgage.”

Basically, it varies. So, even if your credit isn’t perfect, there are still options out there. FICO explains:

“While many lenders use credit scores like FICO Scores to help them make lending decisions, each lender has its own strategy, including the level of risk it finds acceptable. There is no single “cutoff score” used by all lenders, and there are many additional factors that lenders may use . . .”

And if your credit score needs a little TLC, don’t worry—Experian says there are some easy steps you can take to give it a boost, including:

1. Pay Your Bills on Time

Lenders want to see that you can reliably pay your bills on time. This includes everything from credit cards to utilities and cell phone bills. Consistent, on-time payments show you’re a responsible borrower.

2. Pay Off Outstanding Debt

Paying down what you owe can help lower your overall debt and make you less of a risk to lenders. Plus, it improves your credit utilization ratio (how much credit you’re using compared to your total limit). A lower ratio means you’re more reliable to lenders.

3. Don’t Apply for Too Much Credit

While it might be tempting to open more credit cards to build your score, it’s best to hold off. Too many new credit applications can lead to hard inquiries on your report, which can temporarily lower your score.

Bottom Line

Your credit score is crucial when buying a home. Even if your score isn’t perfect, there are still pathways to homeownership.

Working with a trusted lender is the best way to get more information on how your credit score could factor into your home loan.

Is Affordability Starting To Improve?

Is Affordability Starting To Improve?

Over the past couple of years, a lot of people have had a hard time buying a home. And while affordability is still tight, there are signs it’s getting a little better and might keep improving throughout the rest of the year. Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), says:

“Housing affordability is improving ever so modestly, but it is moving in the right direction.”

Here’s a look at the latest data on the three biggest factors affecting home affordability: mortgage rates, home prices, and wages.

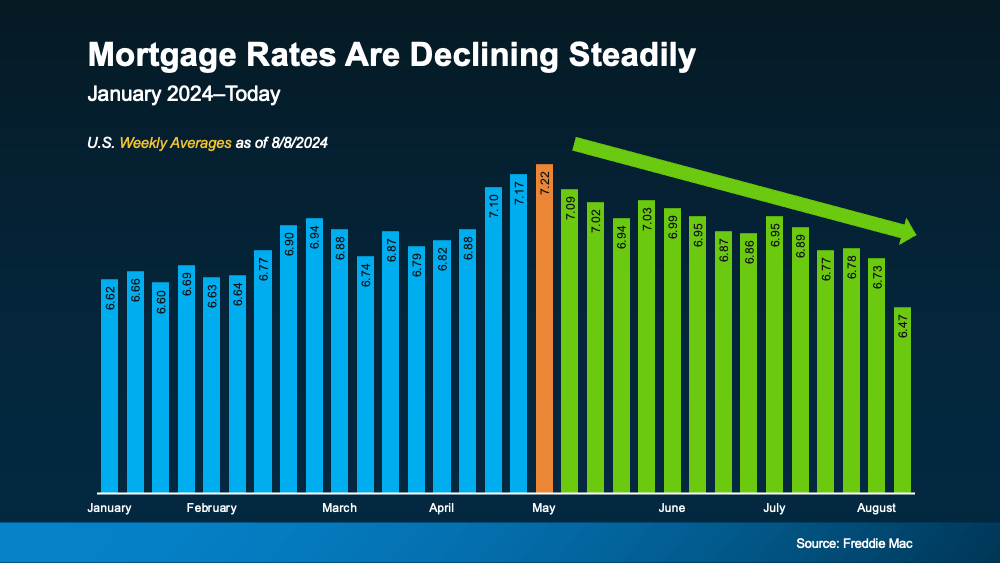

1. Mortgage Rates

Mortgage rates have been volatile this year, bouncing around from the mid-6% to low 7% range. But there’s some good news. Data from Freddie Mac shows rates have been trending down overall since May (see graph below):

Mortgage rates have improved lately in part because of recent economic, employment, and inflation data. Moving forward, some rate volatility is to be expected. But if future economic data continues to show signs of cooling, experts say mortgage rates could keep going down.

Mortgage rates have improved lately in part because of recent economic, employment, and inflation data. Moving forward, some rate volatility is to be expected. But if future economic data continues to show signs of cooling, experts say mortgage rates could keep going down.

Even a small drop can help you out. When rates decline, it’s easier to afford the home you want because your monthly payment will be lower. Just don’t expect them to go back down to 3%.

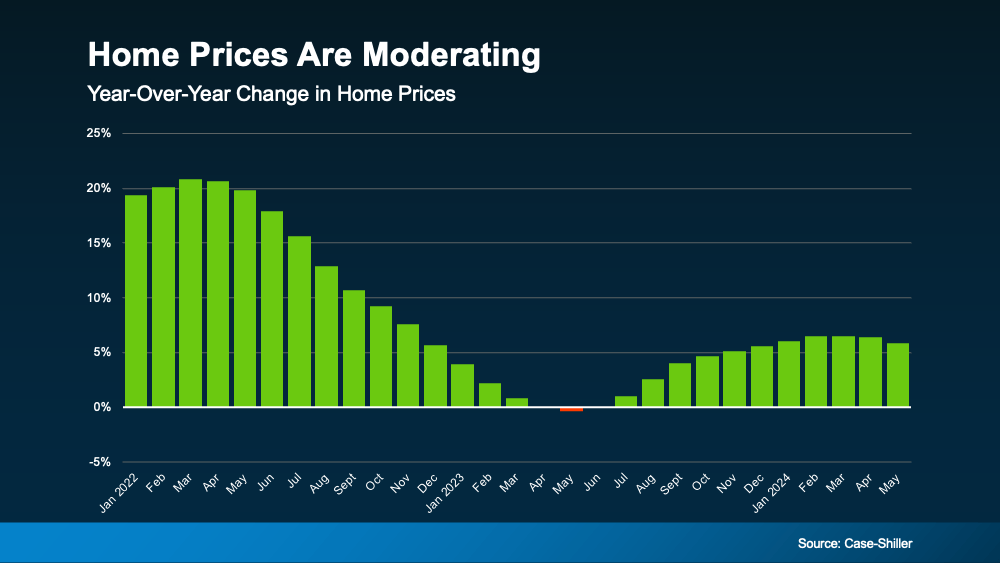

2. Home Prices

The second big thing to think about is home prices. Nationally, they’re still going up this year, but not as fast as they did a couple of years ago. The graph below uses home price data from Case-Shiller to illustrate that point:

If you’re thinking about buying a home, slower price growth is good news. Home prices went up a lot during the pandemic, making it hard for many people to buy. Now, with prices rising more slowly, buying a home may feel less out of reach. As Odeta Kushi, Deputy Chief Economist at First American, says:

If you’re thinking about buying a home, slower price growth is good news. Home prices went up a lot during the pandemic, making it hard for many people to buy. Now, with prices rising more slowly, buying a home may feel less out of reach. As Odeta Kushi, Deputy Chief Economist at First American, says:

“While housing affordability is low for potential first-time home buyers, slowing price appreciation and lower mortgage rates could help – so the dream of homeownership isn’t boarded up just yet.”

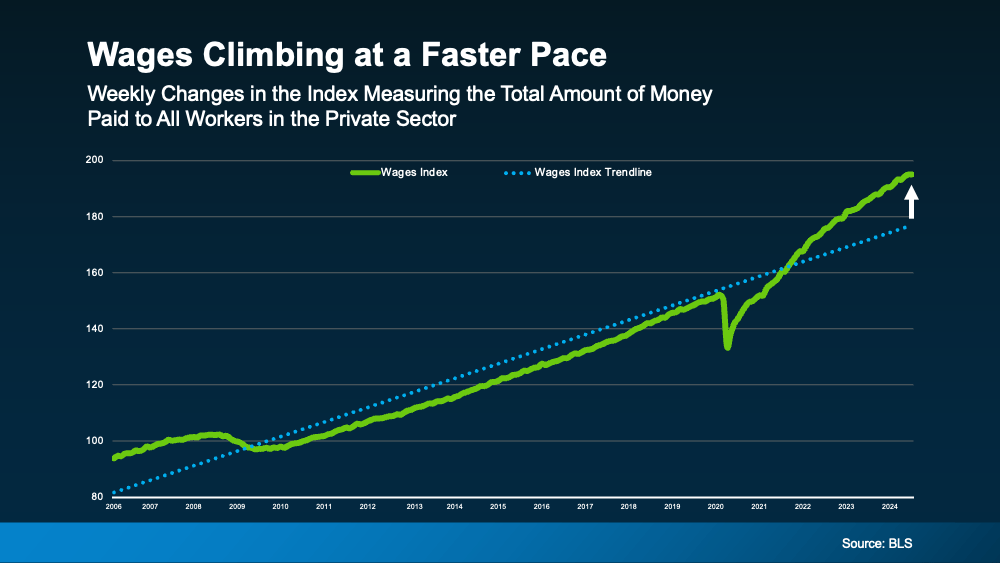

3. Wages

Another factor helping with affordability is rising wages. The graph below uses data from the Bureau of Labor Statistics (BLS) to show how wages have increased over time:

Look at the blue dotted line. It shows how wages usually go up in a typical year. On the right side of the graph, you’ll see wages are rising even faster than normal right now – that’s the green line.

Look at the blue dotted line. It shows how wages usually go up in a typical year. On the right side of the graph, you’ll see wages are rising even faster than normal right now – that’s the green line.

This helps you because if your income increases, it’s easier to afford a home. That’s because you won’t have to spend as much of your paycheck on your monthly mortgage payment.

Bottom Line

When you put all these factors together, you see mortgage rates are trending down, home prices are rising more slowly, and wages are going up faster than usual. Though affordability is still a challenge, these trends are early signs things might be starting to improve.

A Newly Built Home May Actually Be More Budget-Friendly

A Newly Built Home May Actually Be More Budget-Friendly

If you’re in the market to buy a home, there’s some exciting news for you. Many people assume that newly built homes are more expensive than existing ones (houses that have already been lived in), but that’s not always the case. In fact, exploring newly built homes can sometimes lead to more cost-effective options, especially today. Hard to believe, right? But the data doesn’t lie.

Here are two key reasons working with your agent to look into new home construction could help you find a more budget-friendly option.

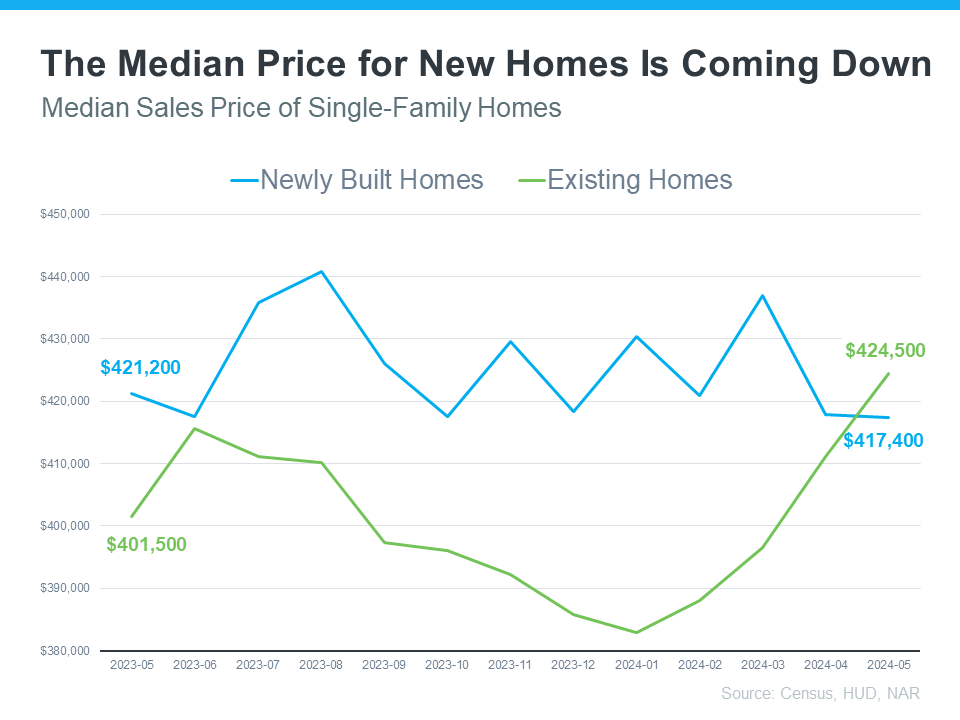

Reason 1: Lower Median Prices for Newly Built Homes

The median sales price for newly built homes is lower than the median sales price for existing homes today. This might seem surprising, but it’s true according to the latest data from the Census and the National Association of Realtors (NAR):

Why is that? Builders are focused on building what they can sell. And right now, there’s a very real need for smaller and more affordable homes – so that’s what they’ve been bringing to the market. At the same time, there are also more newly built homes already on the market than there have been over the past few years, so builders are motivated to make sure they’re selling what they’ve got available before adding more.

Reason 2: Attractive Incentives from Home Builders

Another big reason to consider a newly built home is the range of incentives that many home builders are offering. Again, since builders are aiming to sell their current inventory, some are providing special deals to sweeten the pot for homebuyers. HousingWire explains today’s trend:

“Overall, the usage of sales incentives was up to 61% in June, compared to 59% in May.”

One of the most appealing incentives right now is how builders are able to offer competitive mortgage rates. They may also provide other incentives, such as covering closing costs, or offering free upgrades.

Why This Matters to You

Considering a newly built home could open up opportunities you hadn’t thought of before. With competitive pricing and attractive incentives, you might just find that a brand-new home is the most appealing option for you.

Bottom Line

Buying a home is a big decision, and it’s essential to consider all your options. By looking into newly built homes, you might find a perfect fit for your needs and your budget.

Let’s explore the possibilities together. If you have any questions or want to see what’s available, feel free to reach out.

Why a Foreclosure Wave Isn’t on the Horizon

Why a Foreclosure Wave Isn’t on the Horizon

Even though data shows inflation is cooling, a lot of people are still feeling the pinch on their wallets. And those high costs on everything from gas to groceries are fueling unnecessary concerns that more people are going to have trouble making their mortgage payments. But, does that mean there’s a big wave of foreclosures coming?

Here’s a look at why the data and the experts say that’s not going to happen.

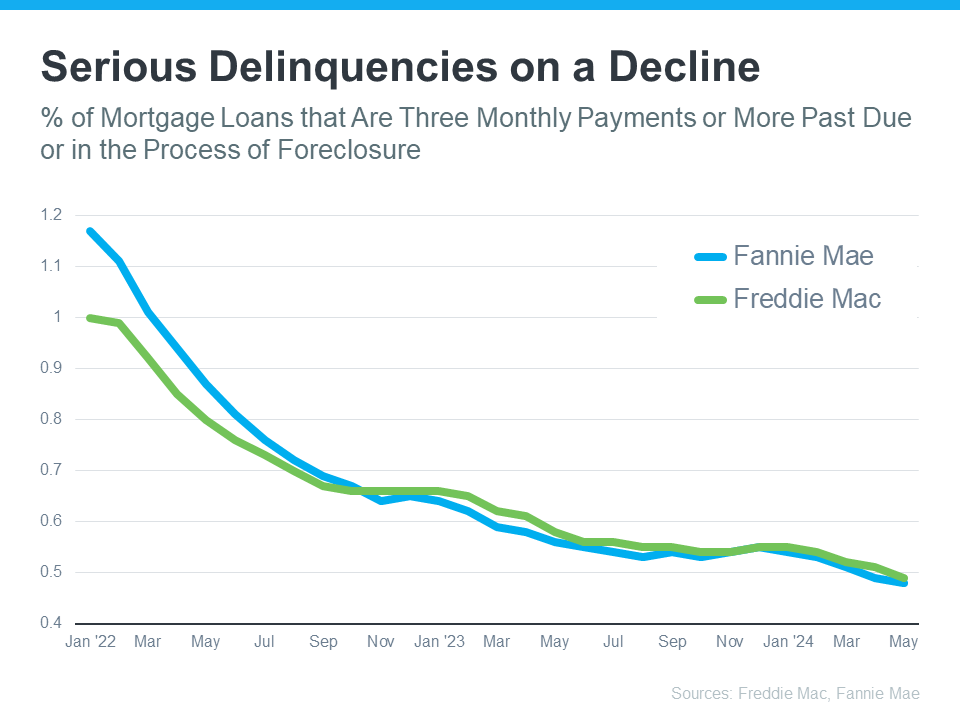

There Aren’t Many Homeowners Who Are Seriously Behind on Their Mortgages

One of the main reasons there were so many foreclosures during the last housing crash was because relaxed lending standards made it easy for people to take out mortgages, even when they couldn’t show they’d be able to pay them back. At that time, lenders weren’t being as strict when looking at applicant credit scores, income levels, employment status, and debt-to-income ratio.

But since then, lending standards have gotten a whole lot tighter. Lenders became much more diligent when assessing applicants for home loans. And that means we’re seeing more qualified buyers who have less of a risk of defaulting on their loans.

That’s why data from Freddie Mac and Fannie Mae shows the number of homeowners who are seriously behind on their mortgage payments (known in the industry as delinquencies) has been declining for quite some time. Take a look at the graph below:

What this means is that, not only are borrowers more qualified, but they’re also finding ways to navigate through their challenges, exploring their repayment options, or maybe even using the record amount of equity they have to sell and avoid foreclosure entirely.

The Answer Is: There’s No Sign of a Wave Coming

Before there can be a significant rise in foreclosures, the number of people who can’t make their mortgage payments would need to rise significantly. But, since so many buyers are making their payments today and homeowners have so much equity built up, a wave of foreclosures isn’t likely.

Take it from Bill McBride of Calculated Risk – an expert on the housing market who, after closely following the data and market leading up to the crash, was able to see the foreclosure crisis coming in 2008. McBride says:

“We will NOT see a surge in foreclosures that would significantly impact house prices (as happened following the housing bubble) for two key reasons: 1) mortgage lending has been solid, and 2) most homeowners have substantial equity in their homes.”

Bottom Line

If you’re worried about a potential foreclosure crisis, know there’s nothing in the data to suggest that’ll happen. Buyers are more qualified now, and that’s one reason why they’re not falling seriously behind on their mortgage payments.

How Affordability and Remote Work Are Changing Where People Live

How Affordability and Remote Work Are Changing Where People Live

There’s an interesting trend happening in the housing market. People are increasingly moving to more affordable areas, and remote or hybrid work is helping them do it.

Consider Moving to a More Affordable Area

Today’s high mortgage rates combined with continually rising home prices mean it’s tough for a lot of people to afford a home right now. That’s why many interested buyers are moving to places where homes are less expensive, and the cost of living is lower. As Orphe Divounguy, Senior Economist at Zillow, explains:

“Housing affordability has always mattered . . . and you’re seeing it across the country. Housing affordability is reshaping migration trends.”

If you’re hoping to buy a home soon, it might make sense to broaden your search area to include places where homes that fit your needs are more affordable. That’s what a lot of other people are doing right now to find a home within their budget. Extra Space Storage explains:

“55% of American adults are looking to relocate to a different state or city for more affordable homes and lower costs of living. . . Specifically, states with a strong economy, lower costs of living, and remote work options continue to be the ideal places to live in the U.S.”

Remote Work Opens Up More Home Options

If you work remotely or drive into the office only a few times each week, you have many more possibilities when looking for your next home. That’s because you can cast a broader net and include more suburban or rural areas nearby. As Market Place Homes says:

“People start to reconsider where they want to live when commute times are slashed in half or eliminated altogether. If they have a longer commute but don’t have to do it daily, they may feel like they can tolerate living farther away from their job. Or, if someone works entirely remotely, they can move to a cheaper area and get a lot of house for their dollar.”

How a Real Estate Agent Can Help

A real estate agent can help you find the perfect home for your budget. They’re especially valuable if you’re moving to a new, unfamiliar area. Bankrate says:

“If you’re moving far away, you may not have a good idea about which neighborhoods or towns will be the best fit. An experienced local agent can help you find the lifestyle you’re looking for in a home you can afford.”

So, if you’re thinking about relocating to somewhere with more affordable homes, what are you waiting for? With the added flexibility of remote work, you might have more options than before.

Bottom Line

Dreaming of a place where your money goes further? Let’s connect so you have someone to help you find your next home. Together, we’ll make your dream of homeownership a reality.

Unlocking Homebuyer Opportunities in 2024

Unlocking Homebuyer Opportunities in 2024

There’s no arguing this past year has been difficult for homebuyers. And if you’re someone who has started the process of searching for a home, maybe you put your search on hold because the challenges in today’s market felt like too much to tackle. You’re not alone in that. A Bright MLS study found some of the top reasons buyers paused their search in late 2023 and early 2024 were:

- They couldn’t find anything in their price range

- They didn’t have any successful offers or had difficulty competing

- They couldn’t find the right home

If any of these sound like why you stopped looking, here’s what you need to know. The housing market is in a transition in the second half of 2024. Here are four reasons why this may be your chance to jump back in.

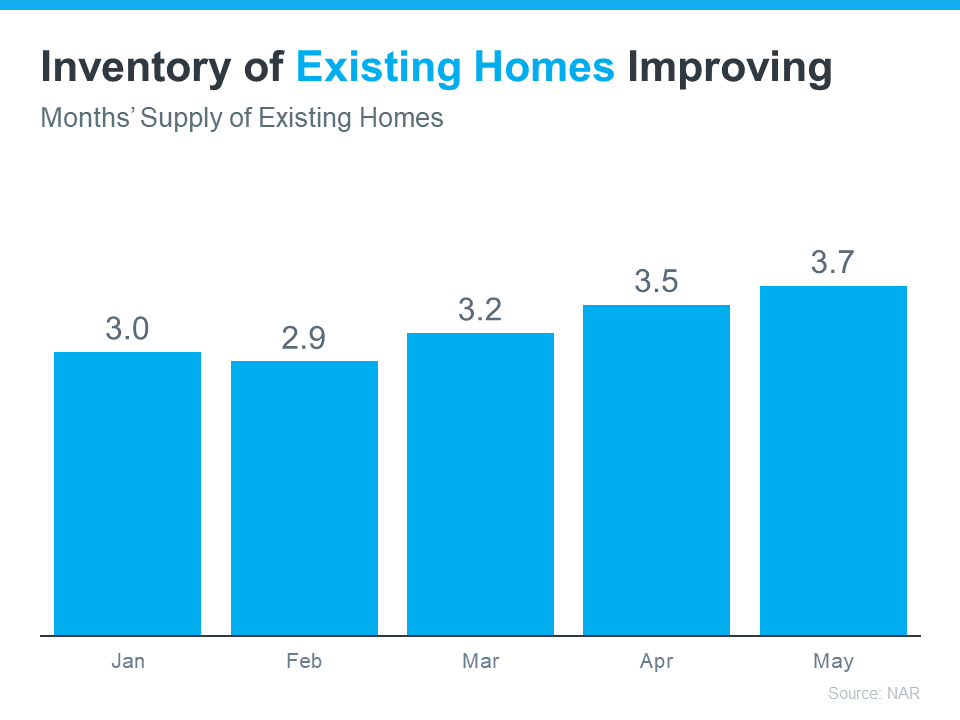

1. The Supply of Homes for Sale Is Growing

One of the most significant shifts in the market this year is how the months’ supply of homes for sale has increased. If you look at data from the National Association of Realtors (NAR), you’ll see how inventory has grown throughout 2024 (see graph below):

This graph shows the months’ supply of existing homes – homes that were previously lived in by another homeowner. The upward trend this year is clear.

This increase means you have a better chance of finding a home that suits your needs and preferences. And if the biggest reason you put off your home search was difficulty finding the right home, this is a big relief.

2. There’s More New Home Construction

And if you still don’t see an existing home you like, another big opportunity lies in the rise of new home construction. Builders have worked to increase the supply of newly built homes this year. And they’ve turned their attention to crafting smaller, more affordable homes based on what’s most needed in today’s market. This helps address the long-standing issue of housing undersupply throughout the country, and those smaller homes also offset some of the affordability challenges you’re feeling today.

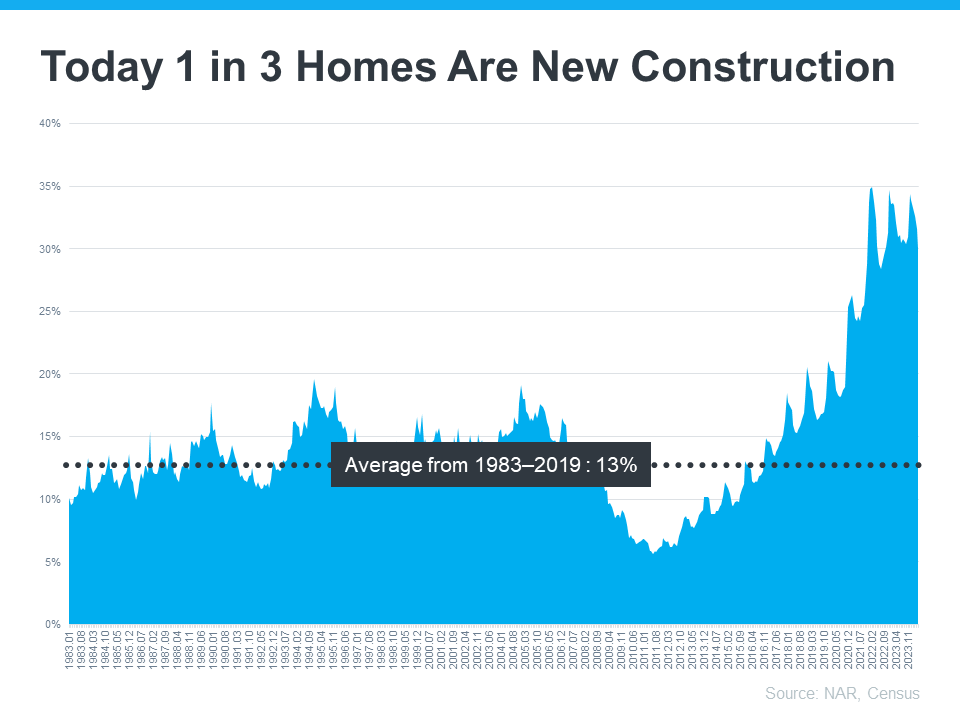

According to data from the Census and NAR, one in three homes on the market is a newly built home (see graph below):

This means, that if you didn’t previously look at newly built homes as part of your search, you may have been cutting your pool of options by a third. Not to mention, some builders are also offering incentives like buying down mortgage rates to make it easier for buyers to get a home that fits their budget.

So, consider talking to your agent about what builders have to offer in your area. Your agent’s expertise on builder reputations, contracts, and more will help you weigh your options.

3. Less Buyer Competition

Mortgage rates are still hovering around 7%, so buyer demand isn’t as fierce as it once was. And when you combine that with more housing supply, you have a better chance of avoiding an intense bidding war. Danielle Hale, Chief Economist at Realtor.com, highlights the positive trend for the latter half of 2024, saying:

“Home shoppers who persist could see better conditions in the second half of the year, which tends to be somewhat less competitive seasonally, and might be even more so since inventory is likely to reach five-year highs.”

This creates a unique opportunity for you to find a home you want to buy with less stress and at a potentially better price.

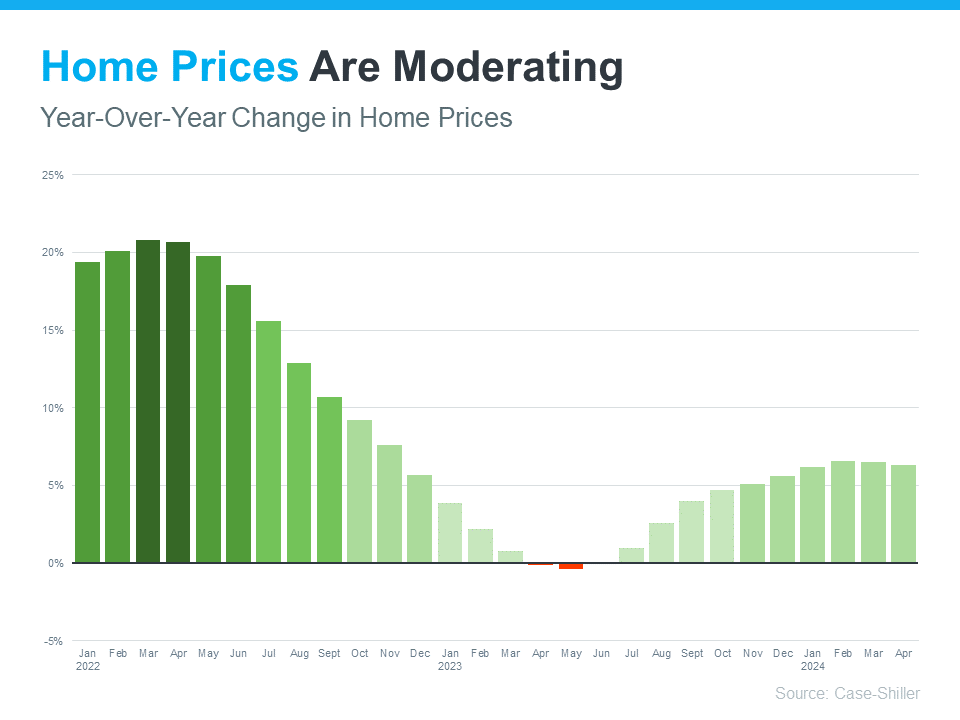

4. Home Prices Are Moderating

Speaking of prices, home prices are also showing signs of moderation – and that’s a welcome shift after the rapid appreciation seen in recent years (see graph below):

This moderation is mostly due to supply and demand. Supply is growing and demand is easing, so prices aren’t rising as fast. But make no mistake, that doesn’t mean prices are falling – they’re just rising at a more normal pace. You can see this in the graph. The bars are still showing prices increasing, just not as dramatic as it was before.

The average forecast for home price appreciation in 2024 is for positive growth around 3% to 5%, which is more in line with historical norms. That moderation means that you are less likely to face the steep price increases we saw a few years ago.

The Opportunity in Front of You

If you’re ready and able to buy, you may find that the second half of 2024 is a bit easier to navigate. There are still challenges, but some of the biggest hurdles you’ve faced are getting better as time wears on.

On the other hand, you could choose to wait. But if you do, here’s the risk you run. As more buyers recognize the shift in the market, competition will grow again. On a similar note, if mortgage rates do come down (as forecasts say), more buyers will flood back into the market. So, making a move now helps you take advantage of the current market conditions and get ahead of those other buyers.

Bottom Line

If you’ve put your dream of homeownership on hold, the second half of 2024 may be your chance to jump back in. Let’s connect to talk more about the opportunities you have in today’s market.

How To Determine if You’re Ready To Buy a Home

How To Determine if You’re Ready To Buy a Home

If you’re trying to decide if you’re ready to buy a home, there’s probably a lot on your mind. You’re thinking about your finances, today’s mortgage rates and home prices, the limited supply of homes for sale, and more. And, you’re juggling how all of those things will impact the choice you’ll make.

While housing market conditions are definitely a factor in your decision, your own personal situation and your finances matter too. As an article from NerdWallet says:

“Housing market trends give important context. But whether this is a good time to buy a house also depends on your financial situation, life goals and readiness to become a homeowner.”

Instead of trying to time the market, focus on what you can control. Here are a few questions that can give you clarity on whether you’re ready to make your move.

1. Do You Have a Stable Job?

One thing to consider is how stable you feel your employment is. Buying a home is a big purchase, and you’re going to sign a home loan stating you’ll pay that loan back. That’s a big commitment. Knowing you have a reliable job and a steady stream of income coming in can help put your mind at ease when making such a large purchase.

2. Have You Figured Out What You Can Afford?

If you have reliable paychecks coming in, the next thing to figure out is what you can afford. That’ll depend on your spending habits, debt, and more. To be sure you have a good idea of what to expect from a number’s perspective, start by talking to a trusted lender.

They’ll be able to tell you about the pre-approval process and what you’re qualified to borrow, current mortgage rates and your approximate monthly payment, closing costs to anticipate, and other expenses you’ll want to budget for. That way you can make an informed decision about whether you’re ready to buy.

3. Do You Have an Emergency Fund?

Another key factor is whether you’ll have enough cash left over in case of an emergency. While that’s not fun to think about, it’s an important thing to consider. You don’t want to overextend on the house, and then not be able to weather a storm if one comes along. As CNET says:

“You’ll want to have a financial cushion that can cover several months of living expenses, including mortgage payments, in case of unforeseen circumstances, such as job loss or medical emergencies.”

4. How Long Do You Plan To Live There?

It was mentioned above, but buying a home involves some upfront expenses. And while you’ll get that money back (and more) as you gain equity, that process takes time. If you plan to move too soon, you may not recoup your investment. For example, if you’re looking to sell and move again in a year, it might not make sense to buy right now. As Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), explains:

“Five years is a good, comfortable mark. If the price of your home appreciates considerably, then even three years would be fine.”

So, think about your future. If you plan to transfer to a new city with the upcoming promotion you’re working toward or you anticipate your loved ones will need you to move closer to take care of them, that’s something to factor in.

5. Above all else, the most important question to answer is: do you have a team of real estate professionals in place?

If not, finding a trusted local agent and a lender is a good first step. The pros can talk you through your options and help you decide if you’re ready to take the plunge or if you have a few more things to get in order first.

Bottom Line

If you want to have a conversation about all the things you need to consider to determine if you’re ready to buy, let’s connect.

Why Working with a Real Estate Professional Is Crucial Right Now

Why Working with a Real Estate Professional Is Crucial Right Now

Navigating the housing market can be tricky, especially these days. That’s why having an experienced guide when buying or selling a home is so important. The market isn’t exactly straightforward right now, and working with a real estate expert can offer insights and advice that make all the difference.

While today’s market conditions might seem confusing or overwhelming, you don’t have to handle them alone. With a trusted expert leading you through every step, you can navigate the process with the clarity and confidence you deserve.

Here are just a few of the ways a real estate expert is invaluable:

Contracts – Agents help with the disclosures and contracts necessary in today’s heavily regulated environment.

Experience – In today’s market, experience is crucial. Real estate professionals know the entire sales process, including how it’s changing right now.

Negotiations – Your real estate advisor acts as a buffer in negotiations with all parties, and advocates for your best interests throughout the entire transaction.

Industry Expertise– Knowledge is power in today’s market, and your advisor will simply and effectively explain processes, market conditions, and key terms, translating what they mean for you along the way along the way.

Pricing – A real estate professional understands current real estate values when setting the price of your home or helping you make an offer to purchase one. Pricing matters more than ever right now, so having expert advice will help ensure you’re set up for success.

A real estate agent is a crucial guide through this challenging market, but not all agents are created equal. A true expert can carefully walk you through the whole real estate process, look out for your unique needs, and advise you on the best ways to achieve success.

Finding an expert real estate advisor – not just any agent – should be your top priority if you want to buy or sell a home. As Bankrate says:

“Real estate is very localized, and you want someone who’s extremely knowledgeable about the market in your specific area. You should also look for someone with a successful track record of negotiating and closing deals, preferably for homes similar to the kind you want to buy.”

What’s the Key To Choosing the Right Expert?

Like any relationship, it starts with trust. You’ll want to know you can depend on that person to always put you and your best interests first. That means hiring a true professional. As Business Insider explains:

“As long as you’ve properly vetted the agents you’re considering and ensured they have the necessary expertise, it’s ok to go with your gut when making your final decision on which real estate agent you want to work with. You’re going to be working closely with this person, so it’s important to choose an agent you’re comfortable with.”

Bottom Line

It’s critical to have an expert on your side who’s well-versed in navigating today’s housing market dynamics. If you’re planning to buy or sell a home this year, let’s connect so you have a real estate professional to give you the best advice and guide you along the way.

The Price of Perfection: Don’t Wait for the Perfect Home

The Price of Perfection: Don’t Wait for the Perfect Home

In life, patience is a virtue – but in the world of homebuying, waiting too long in hopes of finding the perfect home actually isn’t wise. That’s because the pursuit of perfection comes at a cost. And in this case, that cost may be delaying your dream of homeownership. As Bankrate explains:

“One of the most common first-time homebuyer mistakes is looking for a home that checks each of your boxes. Looking for perfection can narrow your choices and lead you to pass over good, suitable options for starter homes in the hopes that something better will come along.”

The Cost of Holding Out for Perfection

Nothing in life is ever perfect – and that’s true when you search for a home too. Unless you’re building a brand-new home from the ground up, chances are there are going to be some features or finishes you wouldn’t have picked yourself. It may be as simple as paint colors, a light fixture, or the tile in the bathrooms or kitchen. Or even that the backyard isn’t fenced in. It could also be that the home itself is great, but it’s not the ideal location you were hoping for.

But here’s the trade-off you’d be making without even realizing it. In all that time you’d spend searching for the perfect place, you’d overlook a lot of homes that would’ve worked for you. U.S. News explains:

“. . . you may miss opportunities if you enter the process with blinders on and aren’t open-minded . . . Countless potential buyers never buy because of this, and thus miss great investments or never move on to the next chapter of their lives.”

It’s Time To Redefine Perfection

Especially with affordability and inventory where they are today, buying a home that needs some updates, is a few neighborhoods away from your ideal location, or doesn’t have all your desired features can be a smart move. Here’s why.

For starters, these homes are usually more affordable, which is important at a time when some buyers are struggling to find options in their budget.

And they give you a chance to make the space your own or discover a whole new area of town. You may find out you actually love that neighborhood. Or, swapping out a feature here or there after move-in isn’t such a big deal. So, look past the green shag carpet and see the bones of the house. With a little vision and creativity, you can turn a good house into a fantastic home.

How an Agent Helps You Explore Your Options

If you’re open to a home that needs a little elbow grease or is a bit further out, let your agent know. They’ll be happy to show you how this can really open up your pool of homes to pick from. They’ll also help coach you through this process by:

1. Prioritizing Your Must-Haves: Your agent will want to revisit your wish list and separate your non-negotiables from your nice-to-haves. From there, they’ll focus on what’s really most important to you as they come up with a bigger list of options for you to choose from.

2. Coaching You To See the Potential: As you tour these added options, your agent will help you look beyond cosmetic flaws and imagine what the home could be with a little work. Simple updates like a fresh coat of paint or new flooring can make a big difference.

3. Connecting You with Local Pros: And an agent’s support goes one step further. If they know what you’re hoping to change after you move in, they can connect you with local pros who can get the job done. That way it’s less work for you, and you don’t have to worry about tracking down contractors.

Bottom Line

Remember, there is no perfect home. But with expert help and an open mind, we can find you the right home – even in today’s market. Let’s connect to see what’s out there.

What You Need To Know About Today’s Down Payment Programs

What You Need To Know About Today’s Down Payment Programs

There’s no denying it’s gotten more challenging to buy a home, especially with today’s mortgage rates and home price appreciation. And that may be one of the big reasons you’re eager to look into grants and assistance programs to see if there’s anything you qualify for that can help. But unfortunately, many homebuyers feel like they don’t know where to start.

A recent Bank of America Institute study asked prospective buyers where they lack confidence in the process and need more information. And this is what topped the list:

53% said they need help understanding homebuying grant programs.

So, here’s some information that can help you close that gap.

What Is Down Payment Assistance?

As the Mortgage Reports explains:

“Down payment assistance (DPA) programs offer loans and grants that can cover part or all of a home buyer’s down payment and closing costs. More than 2,000 of these programs are available nationwide. . . DPA programs vary by location, but many home buyers could be in line for thousands of dollars in down payment assistance if they qualify.”

And here’s some more good news. On top of all of these programs, you probably don’t need to save as much for your down payment as you think. Contrary to what you may have heard, typically you don’t have to put 20% down unless it’s specified by your loan type or lender. So, you likely don’t need to save as much upfront, and there are programs designed to make your down payment more achievable. Sounds like a win-win.

First-Time and Repeat Buyers Are Often Eligible