| Tweet |

Time in the Market Beats Timing the Market

Time in the Market Beats Timing the Market

Trying to decide whether it makes more sense to buy a home now or wait? There’s a lot to consider, from what’s happening in the market to your changing needs. But generally speaking, aiming to time the market isn’t a good strategy – there are too many factors at play for that to even be possible.

That’s why experts usually say time in the market is better than timing the market.

In other words, if you want to buy a home and you’re able to make the numbers work, doing it sooner rather than later is usually worth it. Bankrate explains why:

“No matter which way the real estate market is leaning, though, buying now means you can start building equity immediately.”

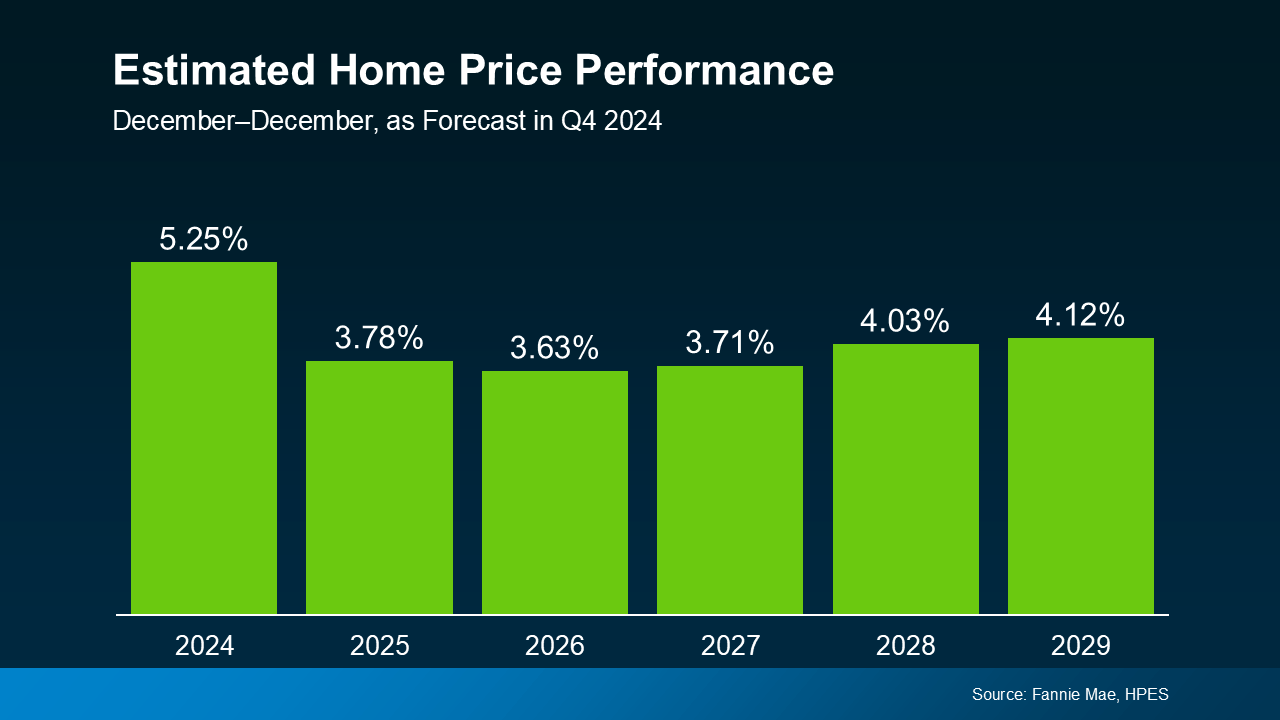

Here’s some data to break this down so you can really see the benefit of buying now versus later – if you’re able to. Each quarter, Fannie Mae releases the Home Price Expectations Survey. It asks over one hundred economists, real estate experts, and investment and market strategists what they forecast for home prices over the next five years. In the latest release, experts are projecting home prices will continue to rise through at least 2029 – just at a slower, more normal pace than they did over the past few years (see the graph below):

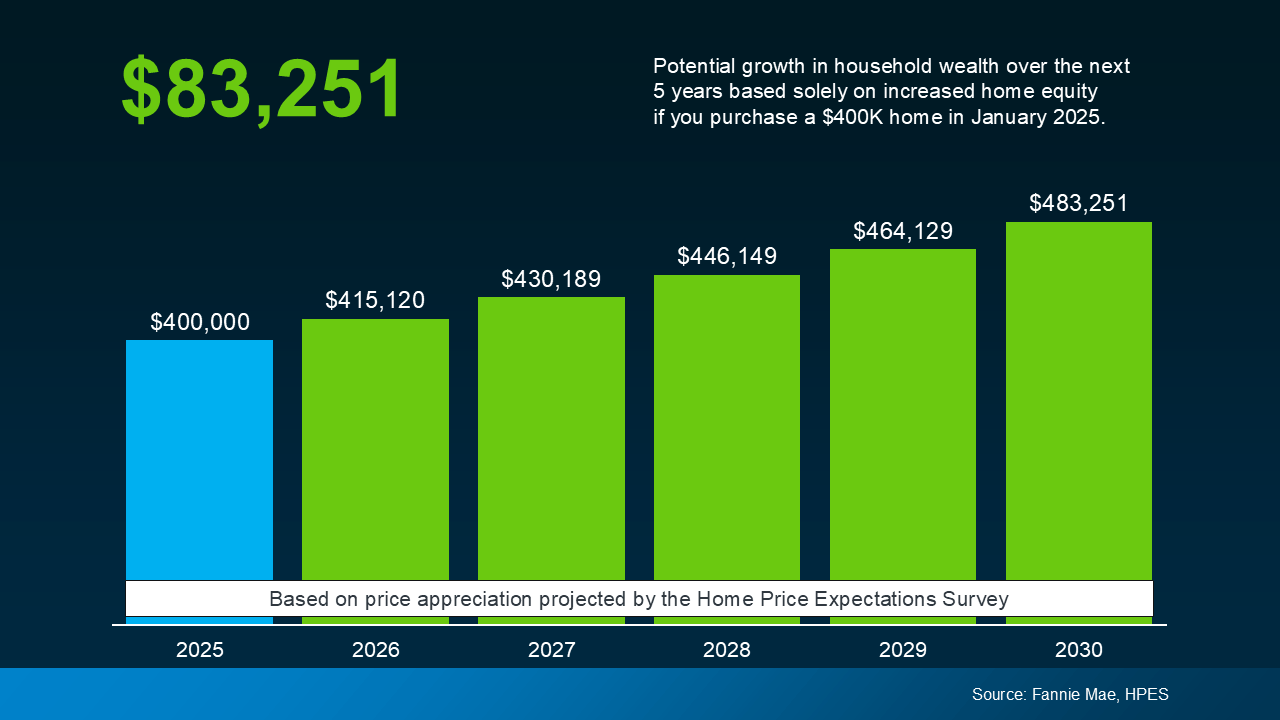

But what does that really mean for you? To give these numbers context, the graph below uses a typical home value to show how it could appreciate over the next few years using those HPES projections (see graph below). This is what you could start to earn in equity if you buy a home in early 2025.

But what does that really mean for you? To give these numbers context, the graph below uses a typical home value to show how it could appreciate over the next few years using those HPES projections (see graph below). This is what you could start to earn in equity if you buy a home in early 2025.

In this example, let’s say you go ahead and buy a $400,000 home this January. Based on the expert forecasts from the HPES, you could gain more than $83,000 in household wealth over the next five years. That’s not a small number. If you keep on renting, you’re losing out on this equity gain.

In this example, let’s say you go ahead and buy a $400,000 home this January. Based on the expert forecasts from the HPES, you could gain more than $83,000 in household wealth over the next five years. That’s not a small number. If you keep on renting, you’re losing out on this equity gain.

And while today’s market has its fair share of challenges, this is why buying is going to be worth it in the long run. If you want to buy a home, don’t give up. There are creative ways we can make your purchase possible. From looking at more affordable areas, to considering condos or townhomes, or even checking out down payment assistance programs, there are options to help you make it happen.

So sure, you could wait. But if you’re just waiting it out to perfectly time the market, this is what you’re missing out on. And that decision is up to you.

Bottom Line

If you’re torn between buying now or waiting, don’t forget that it’s time in the market, not timing the market that truly matters. Let’s connect if you want to talk about what you need to do to get the process started today.

New Year, New Home: How To Make It Happen in 2025

New Year, New Home: How To Make It Happen in 2025

This is the time when a lot of people take a moment to reflect and set their goals for this year. And as you picture what you want your 2025 to look like, one thing that may pop into your mind is the vision of you in a new home. But how do you get there? And where do you start?

Here’s some advice that can help you get the ball rolling.

Focus on Your Why

To lay the foundation, you need to focus on your why. While the dollars and cents are important, so is the driving force behind your desire to move. Maybe you need more space for a growing family, want to sell so you can downsize, or are finally ready to buy your first home. Whatever your reason, it’s important to keep it front and center.

Your why is what helps you stay focused. Share your motivation with your agent and they’ll use their expertise to help support that goal, no matter what the market looks like. With a great agent by your side, you’ll have someone to guide you, problem-solve, and keep you moving forward until you can check that goal off your to-do list.

Get Clear on What You Need

Then it’s time to figure out what your next home needs to have. How many bedrooms do you need? If you don’t have a designated home office, is that a deal-breaker? What about a big fenced-in backyard? Knowing your must-haves and nice-to-haves makes the search a lot smoother.

Since affordability is still tight, it’s important to have a clear idea of your essential items upfront. Maybe you can flex a bit on location, if it’s got everything else you’re looking for. Go over those essential items with your agent and they’ll help you focus on the homes that check the boxes that matter most while staying within your price range.

Know Your Numbers

Before you jump in, take a look at your finances. How much have you saved? What monthly payment feels comfortable? Getting clear on your budget early will help you know what’s possible.

The best way to do this is by partnering with trusted real estate professionals, like a local agent and a lender. They’ll help you:

- Plan for your down payment and look into down payment assistance programs

- Understand the equity you have in your current home and how you can use it to fuel your next move if you’re selling

- Get pre-approved for a mortgage so you know what you can borrow

Lean on a Pro To Guide You

It can be hard to know where to start, but you don’t have to do it alone. A real estate agent knows what you need to do to get ready to buy or sell, how to navigate the process, and can answer your questions every step of the way. As Bankrate puts it:

“. . . now more than ever, it’s smart to lean on the guidance of an experienced local real estate agent. If you want to enter the housing market in 2025, whether as a buyer or a seller, let a pro lead the way for you.”

Remember, buying or selling is a big milestone and a great goal for this year. With the right expert on your team, you’ll feel confident and ready to take on the market.

Bottom Line

If buying or selling a home is part of your goals for 2025, now’s the time to get started. Focus on your why, know what you need, and connect with trusted pros to make it happen. Let’s team up and make this the year you accomplish your real estate resolutions.

What’s Motivating More Buyers To Choose a Newly Built Home?

What’s Motivating More Buyers To Choose a Newly Built Home?

Planning to buy a home soon? Why not go for something brand-new? Because data shows a lot more buyers are seeing the appeal of new home construction these days – and you may find out it’s what you want too.

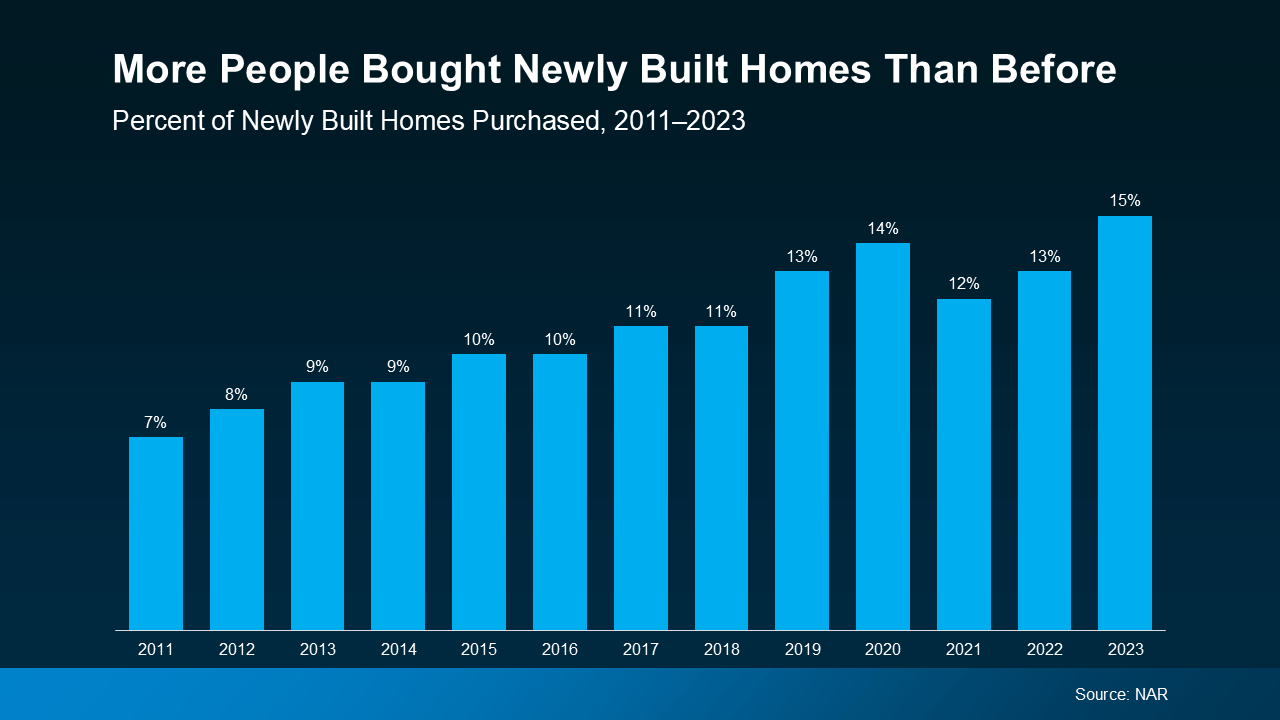

The National Association of Realtors (NAR), explains that newly built homes accounted for 15% of all homes sold last year. That’s a significant increase, and is actually the highest percentage in 17 years (see graph below):

To get a closer look at why so many people are opting for a brand-new home, NAR surveyed recent buyers. And here are the top reasons why new builds gained so much popularity (see graph below):

To get a closer look at why so many people are opting for a brand-new home, NAR surveyed recent buyers. And here are the top reasons why new builds gained so much popularity (see graph below):

Avoiding Renovations or Problems with Plumbing or Electricity (42%)

Avoiding Renovations or Problems with Plumbing or Electricity (42%)

According to buyers, the number one benefit is the peace of mind that comes with getting brand-new everything. Because let’s face it, buying a home right now is pricey. And with inflation also putting a pinch on your wallet, you want to do everything you can to cut down on any additional costs. Enter new builds.

A home that was just built is less likely to have unexpected repairs, and that means less maintenance you’ll need to budget for upfront. Plus, since many builders include warranties on their homes, that’s an added layer of protection for your wallet on some of the home’s major systems.

Ability To Choose and Customize Design Features (27%)

You may also get the chance to personalize parts of the build to your unique tastes. That can be as small as which knobs go on the cabinets and which light fixture goes in the dining room to as big as floor plans and siding color. So, if you’re not finding a home you like, it may be time to build one.

The Amenities of New Home Construction Communities (25%)

Many new developments also offer amenities like parks, pools, fitness centers, and community spaces. These features could help you feel more connected to your neighborhood and can be a great perk for your lifestyle.

Lack of Inventory of Previously Owned Homes (15%)

Since the supply of existing homes (homes that were previously lived in) is still lower than the norm, more people are asking their agents if they can see what builders have available – and builders aren’t disappointing. Right now, new builds make up a larger portion of the homes available for sale than the norm. So, checking out these homes can really open up your pool of options. And don’t worry – builders are not overbuilding. They’re just catching up after years of underbuilding.

Energy Efficiency (14%)

Not to mention, newly built homes usually have the latest energy-efficient materials and technologies. This not only feels good, but can also lead to lower utility bills and a reduced environmental footprint. In a U.S. News Real Estate interview with Kevin Morrow, Senior Program Manager at the National Association of Home Builders (NAHB), this topic came up:

“The more energy-efficient mechanics of the house also help reduce utility bills for new home buyers . . . Newly-constructed homes often include green systems and appliances—like high efficiency stoves, refrigerators, washing machines, water heaters, furnaces, or air conditioning units—that homes built years ago might not.”

Smart Home Features (11%)

And last on this list is the integration of smart technologies. Tech-savvy buyers often want the latest and greatest advancements – and new home construction usually delivers.

The Importance of Using Your Own Agent

Newly built homes are becoming a top pick for buyers these days, and it’s easy to see why. If you’re feeling motivated to see what’s out there, just remember you need to have your own real estate agent.

Builder contracts often have some complex terms and complicated fine print. If you bring your own agent, you’ll have someone to advocate for you, make sure you’re getting quality construction, and guide you through the process from start to finish.

Bottom Line

Imagine skipping the hassle of renovations and having the freedom to pick out the exact design features you want. If this sounds good to you, let’s connect to make sure you’ve got your own agent to help you negotiate with the builder so you can buy a new home with confidence.

The Personal Joys of Having a Home To Call Your Own

The Personal Joys of Having a Home To Call Your Own

There’s no doubt that owning a home comes with significant financial benefits. And this time of year is a great time to reflect on the other reasons why owning a home is so meaningful.

A house is more than four walls and a roof – it’s a place where memories are made, connections are built, and life happens.

From the sense of accomplishment that comes with owning your own home to the joy of creating a space that’s uniquely yours, the emotional connections we have to our homes can be just as important as the financial ones.

Here are some of the things that turn a house into a happy home.

1. It’s an Accomplishment You Can Be Proud Of

Buying a home is a significant milestone, whether it’s your first or your fifth. You’ve worked hard to make it happen and achieving this goal is a reason to celebrate. There’s nothing quite like stepping through the door of a home that’s yours and knowing you’ve accomplished something truly special.

2. It’s a Place You Can Call Your Own

Compared to renting, owning a home can give you a much greater sense of security and privacy. It’s your own place – not your landlord’s – and that just feels different. No one else has the keys but you and that gives you your own personal safe place to retreat to at the end of a long day.

3. It’s a Space That’s Yours To Customize

Owning a home means you have the freedom to personalize it however you like. While there can be HOA guidelines you may have to follow depending on where you buy, you can still make it a reflection of your style and create a space that feels just right for you. As Freddie Mac explains:

“As the homeowner, you have the freedom to adopt a pet, paint the walls any color you choose, renovate your kitchen, and more. You can customize your own space without approval from landlords.”

4. It’s a Foundation for Building a Sense of Community

Homeownership often means putting down roots in a neighborhood and becoming a part of the local community. According to groups like Habitat for Humanity, owning a home increases your interest in getting involved with your neighbors and local organizations. Whether it’s through joining a neighborhood group, volunteering, or simply getting to know the people next door, a home is a great foundation for building meaningful connections.

Bottom Line

Owning a home is about so much more than financial benefits – it’s about the pride, well-being, and sense of belonging it can bring. When you’re ready to take the next step toward buying a home, let’s connect.

The #1 Reason People Move: To Be Closer to Family and Friends

The #1 Reason People Move: To Be Closer to Family and Friends

Have you ever thought about packing up and moving to be closer to the people who mean the most to you? Maybe you’re tired of long drives to see your family or wish your kids could spend more time with their grandparents. Clearly, a lot of other people feel the same way.

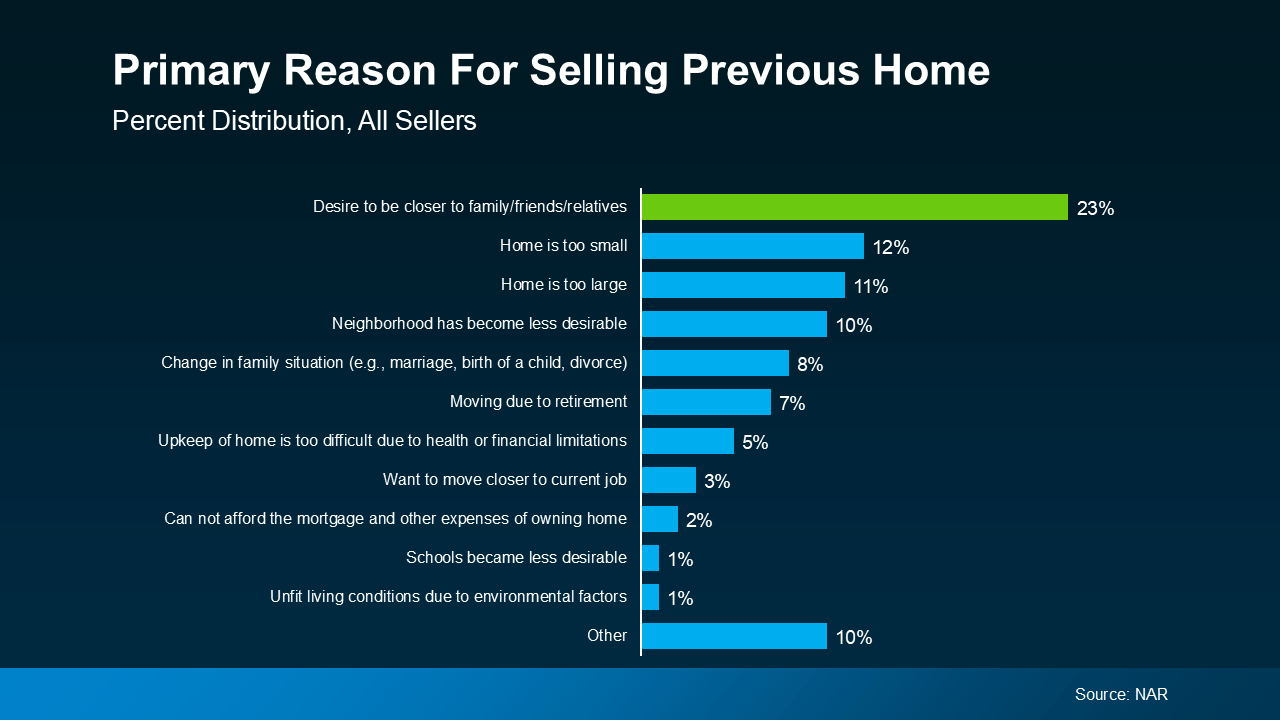

According to recent data from the National Association of Realtors (NAR), the desire to be near family and friends is the #1 reason people move (see graph below):

That’s because moving isn’t just about finding a new house – it’s about living a life where you’re surrounded by the people who matter most. Whether it’s catching up over weeknight dinners, watching your kids play with their cousins, or just knowing someone’s there when you need them, living near loved ones changes everything.

That’s because moving isn’t just about finding a new house – it’s about living a life where you’re surrounded by the people who matter most. Whether it’s catching up over weeknight dinners, watching your kids play with their cousins, or just knowing someone’s there when you need them, living near loved ones changes everything.

Let’s dive into why so many people are making this move and how it could be the best decision for you, too.

Why Family Comes First

Living near family and friends is a universal motivator that cuts across all types of buyers, whether you’re buying your first home or making a big lifestyle change.

But it’s especially important to repeat buyers. Unlike first-time homebuyers, who may be more focused on looking in more affordable areas, repeat buyers often have more flexibility on where they live. Many Baby Boomers, for example, have built significant equity in their homes, giving them the freedom to prioritize what matters most – like retiring near their grandkids. As Ali Wolf, Chief Economist at Zonda, says:

“25% of Baby Boomer households plan to retire near their children and grandchildren . . .”

Making a move to be closer to friends and family is all about creating a meaningful next chapter in your life where loved ones are just around the corner.

The Benefits of Living Near Loved Ones

But moving closer isn’t just a lifestyle choice – it’s a decision that offers real benefits:

- Spending More Time Together Whether it’s joining family dinners, going to weekend activities, or simply having someone nearby to talk to, these moments strengthen relationships and make life more fulfilling.

- Sharing Resources Living close to family can provide practical advantages, too – like sharing childcare, tools, or household items.

- Cutting Down on Travel Instead of spending hours on the road to spend time together, you can enjoy more spontaneous visits. This not only enhances your quality of life, but it also provides peace of mind in case of emergencies.

- Being There for Big Moments It also offers both emotional and practical support during life’s milestones. From graduations to tough times, being close to loved ones helps you feel connected and cared for.

Ready To Make Your Move?

At the end of the day, home isn’t just a place you live – it’s where your people are. Whether you’re looking to spend more quality time with family or enjoy the practical benefits of being closer to loved ones, the decision to move closer to those you care about is a deeply personal one.

Bottom Line

If you’re thinking about making a change, let’s connect. Together, we can explore neighborhoods that bring you closer to the people and places you love most.

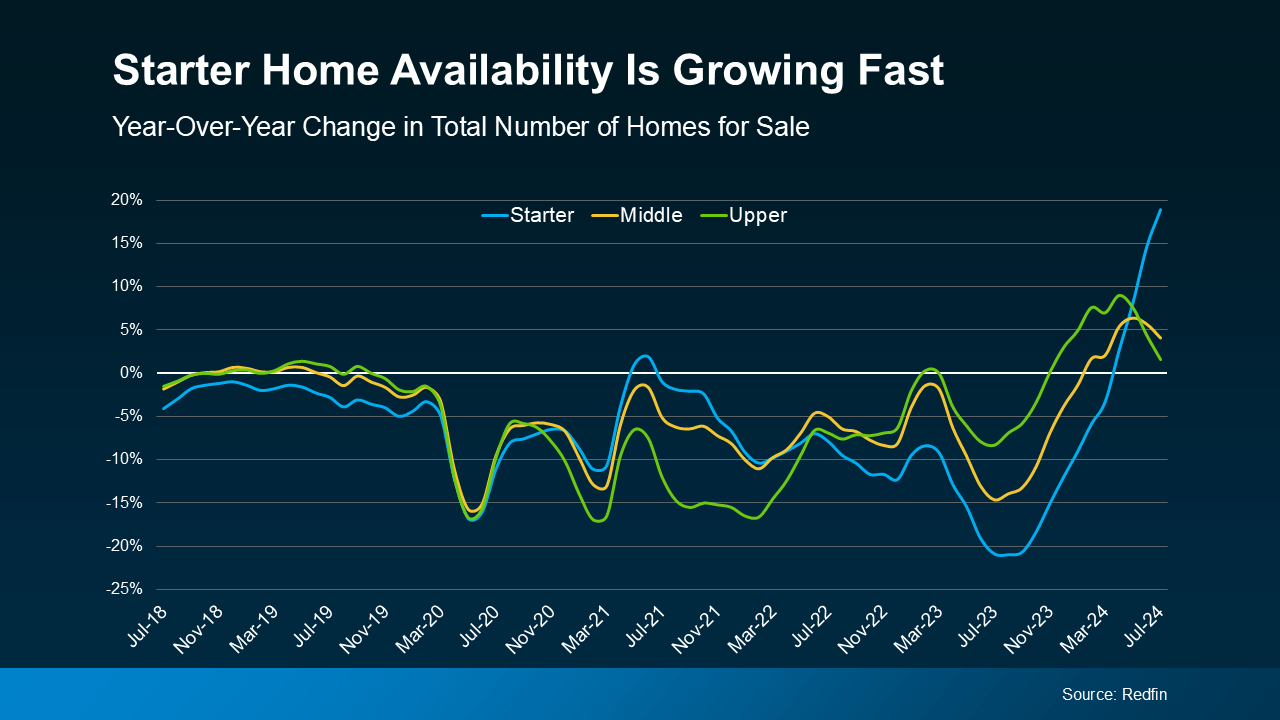

More Starter Homes Are Hitting the Market

More Starter Homes Are Hitting the Market

More entry-level homes – also known as starter homes – are popping up on the market. And after several years with very few homes available to buy and prices rising, there are finally some more options for first-time buyers.

Inventory Is Increasing – Especially at Lower Price Points

Over the past year, the total supply of homes for sale has improved. According to Realtor.com, in November there were 26.2% more homes for sale compared to this time last year, marking 13 months of inventory growth and the most homes available since December of 2019.

Interestingly, the growth isn’t spread evenly among all types of homes, though. According to Redfin, starter homes have seen the biggest increase (see graph below):

So, if you’re a first-time buyer who’s been sitting on the sidelines waiting because you thought you might never find a starter home in your market, this could be a game-changer. You finally have more options to choose from, and you just might be able to find one in your price range.

So, if you’re a first-time buyer who’s been sitting on the sidelines waiting because you thought you might never find a starter home in your market, this could be a game-changer. You finally have more options to choose from, and you just might be able to find one in your price range.

How an Experienced Agent Helps You Find a Starter Homes

Finding the right starter home at the right price point in your local market might feel like an unthinkable challenge, but a local real estate agent makes it easier. They stay up to date on the latest starter home listings in your area, so you don’t miss any opportunities.

Your agent will help you focus on homes that match your budget and your needs, making the search less stressful. They’ll also guide you through how to make the right offer and negotiate to get the best outcome possible.

On top of that, they handle the important details, like documentation and deadlines, so you can stay right on track. And if you have questions, your agent is there with answers and expert advice every step of the way.

Bottom Line

Starter homes are making a bit of a comeback, and this could be your chance to find one. Whether you’re ready to visit listings, need advice, or just want to see what’s out there, let’s connect.

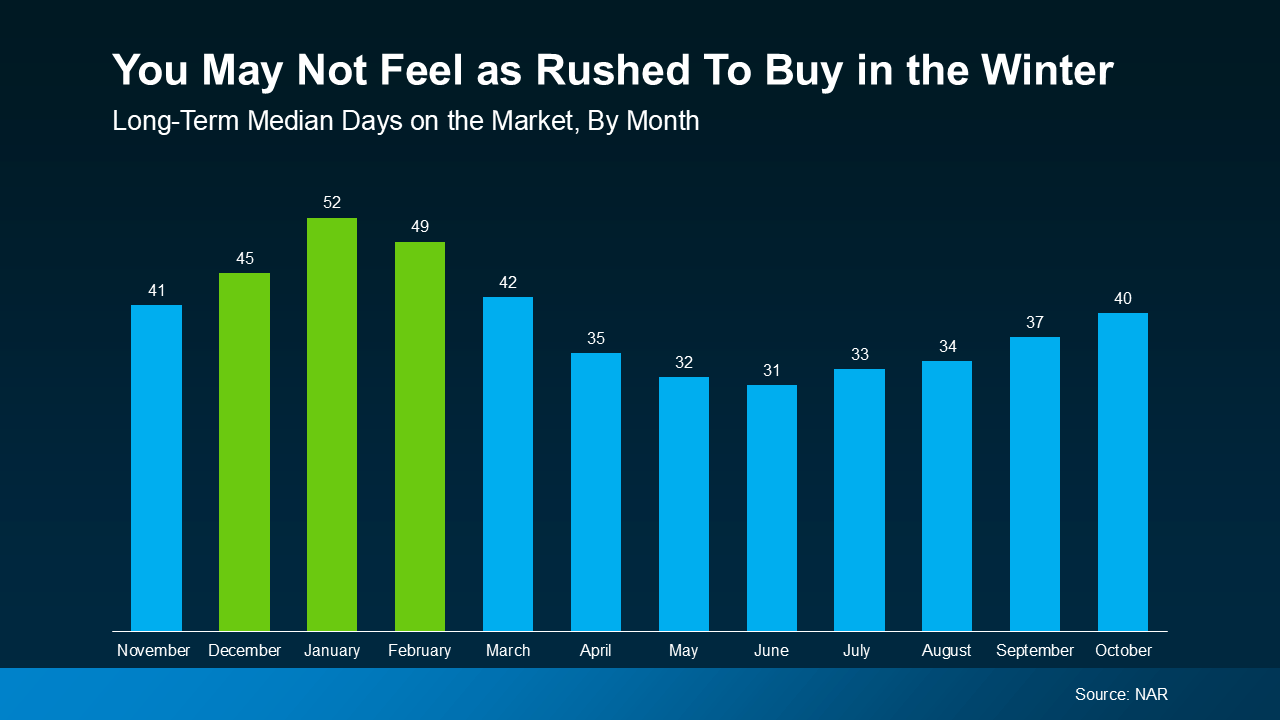

The Biggest Perks of Buying a Home This Winter

The Biggest Perks of Buying a Home This Winter

Waiting for perfect market conditions often means missing out. Because what you may not realize is, if you’re ready and able to buy, this time of year could actually give you an edge. Here’s why. As the weather cools down, the housing market can too – and that works in your favor.

You Likely Won’t Feel as Rushed

Homes tend to take a little longer to sell during this time of year. Data from the National Association of Realtors (NAR) shows the average time a house sits on the market jumps up during the winter months (see the green bars in the graph below):

This is partly because fewer buyers are active at this time of year – and that decrease in buyer competition means the houses that are on the market aren’t going to be snatched up as quickly. So, if you decide to buy a home in the next couple of months, you’ll likely have more time to consider your options and negotiate a deal without feeling as pressured.

This is partly because fewer buyers are active at this time of year – and that decrease in buyer competition means the houses that are on the market aren’t going to be snatched up as quickly. So, if you decide to buy a home in the next couple of months, you’ll likely have more time to consider your options and negotiate a deal without feeling as pressured.

Sellers May Be More Willing To Negotiate

And since homes generally take longer to sell during the winter, sellers are often more motivated to close a deal. That can work in your favor, too. According to NAR:

“Less competition can lead to better deals. While homes are not selling as fast as during the summer, sellers may be more willing to negotiate.”

Whether it’s compromising on price, covering closing costs or repairs, or including extras like appliances, you have more room to ask for what you need.

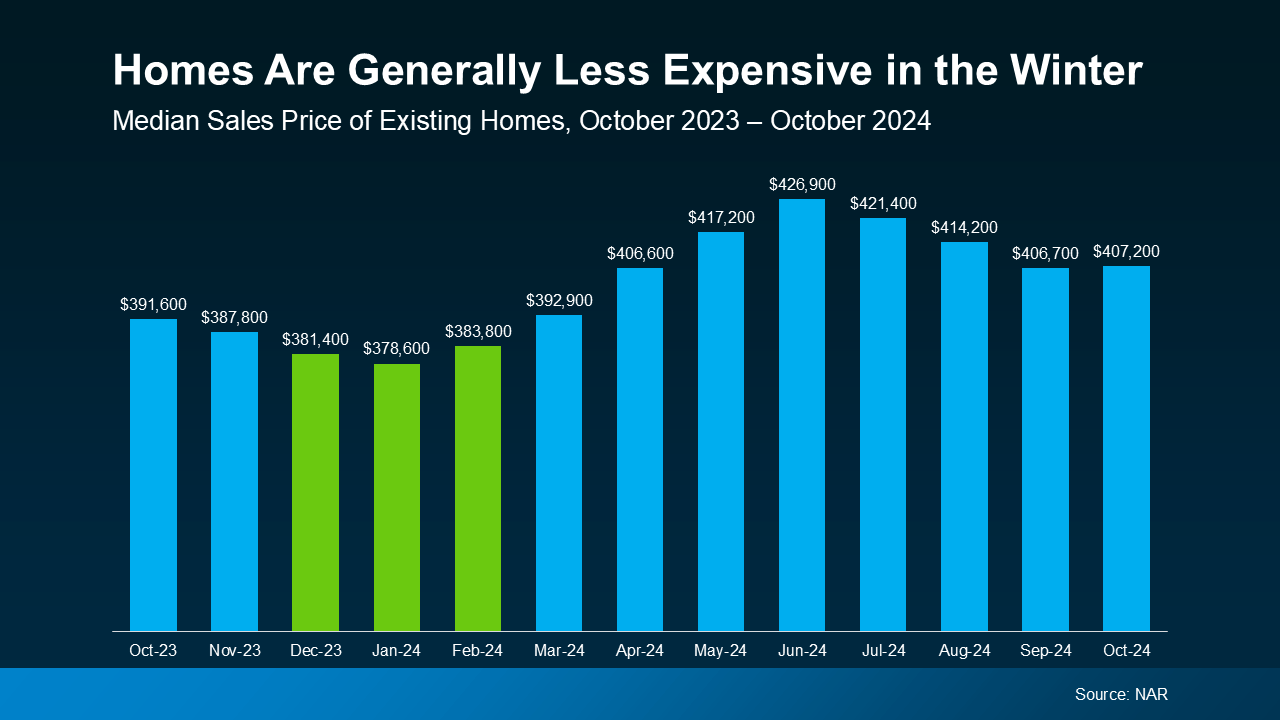

Homes Are Less Expensive in the Winter

With less competition from other buyers and sellers who are more willing to negotiate, you may see slightly lower prices too. In fact, according to NAR, homes are typically about 5% less expensive now compared to when prices normally peak in the summer.

That might not seem like a huge difference, but on a $400,000 home, it could mean savings of $20,000 on the purchase price.

You can see this expected seasonal shift in home prices taking place this year. Take a look at the graph below showing the median sales price of existing homes (homes that were previously owned) over the past 12 months. You’ll notice in the green bars that prices were lower in the winter months last year, and it seems like that’s going to happen again this year. That gives you the chance to make your budget go further:

Bottom Line

Buying a home during the winter means less competition, motivated sellers, and potentially lower prices, too. Let’s work together to find the right one at the right price for you.

The Top 2 Reasons To Look at Newly Built Homes

The Top 2 Reasons To Look at Newly Built Homes

When planning a move, a newly built home might not be the first thing that comes to mind. But with more brand-new homes on the market and builders focusing on smaller, more affordable options, this type of home may just be the key to crossing the homebuying finish line.

Here’s why a new build is worth considering – and how an agent can help you find one that meets your needs and your budget.

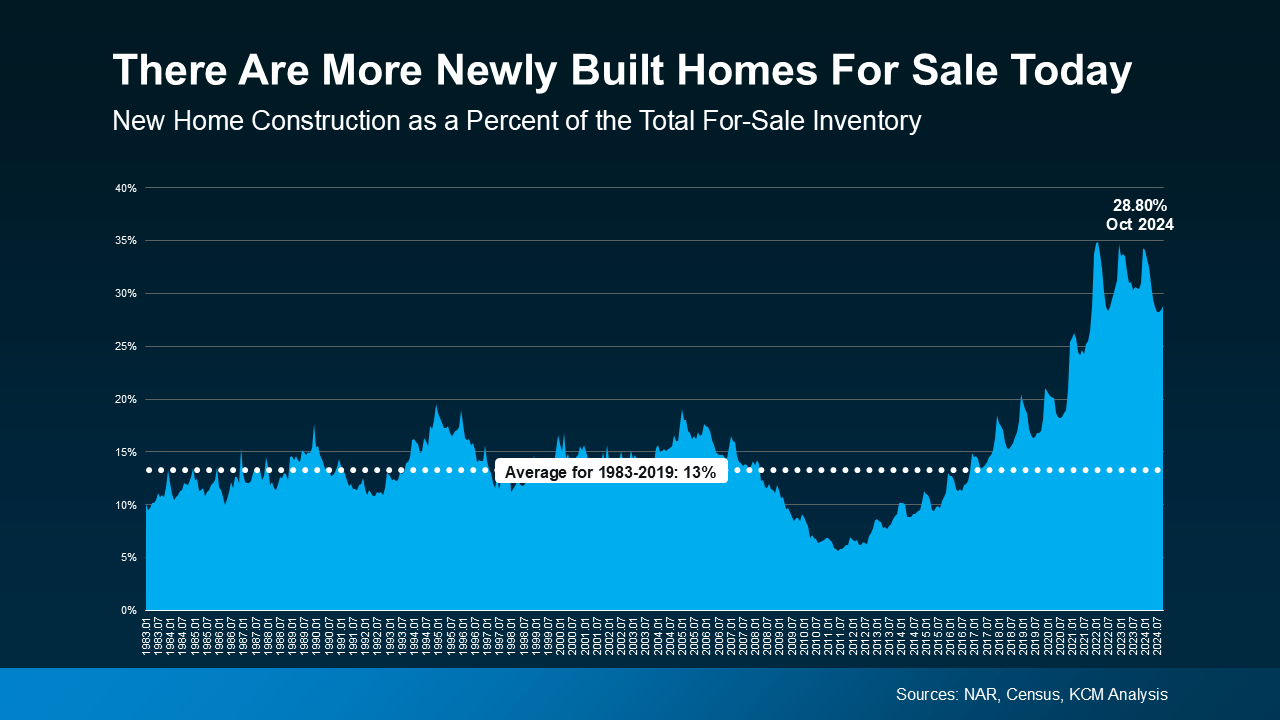

1. More Newly Built Homes Are Available Right Now

First, let’s break down the types of homes on the market. A newly built home is a house that was just built or is under construction. On the other hand, an existing home is one a homeowner has already lived in.

Right now, the number of existing homes for sale is still low. And, if you’re struggling to find something you like because there aren’t that many existing homes for sale, opening up your search to include brand-new homes could really expand your options. That’s because there are more newly built homes available right now than in a typical year (see graph below):

From 1983 to 2019, newly built homes made up only 13% of the total inventory of homes for sale. Today, that number has climbed to 28.8%, according to the most recent data.

From 1983 to 2019, newly built homes made up only 13% of the total inventory of homes for sale. Today, that number has climbed to 28.8%, according to the most recent data.

And as Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), notes:

“Even though existing home sales have been stuck at low levels, newly constructed home sales look to mark one of its best annual performance in 15 years . . . The new home inventory has been consistently rising with homebuilders getting active and making up around 1/3 of total inventory.”

While the uptick in new home construction is encouraging, rest assured that builders aren’t overdoing it, they’re just making up for over a decade of underbuilding. There are still way more buyers than there are homes on the market. But the good news for you is this increase in newly built homes means more options for your search.

2. Newly Built Homes Are Becoming Less Expensive

Still skeptical if a new build is right for you or if they’re even in your budget? The average cost of newly built homes has actually come down from a year ago.

Why is that? Builders know affordability is top of mind for homebuyers right now. So they’re focusing their efforts on building smaller homes they can offer at lower price points and are more likely to sell. As Realtor.com says:

“Builders are increasingly bringing smaller, more affordable homes to the market, so buyers may find more newly-built homes that fit their budget.”

Something to keep in mind: buying a newly built home isn’t the same as buying an existing one. Builder contracts have different fine print. So be sure to partner with a local agent who knows the market, builder reputations, and what to look for in those contracts.

Bottom Line

Depending on your needs and budget, a new build might be the opportunity you’ve been waiting for to bring your homebuying vision to life. If you’re interested in a brand-new home, let’s connect so you can check out what builders in your area are up to.

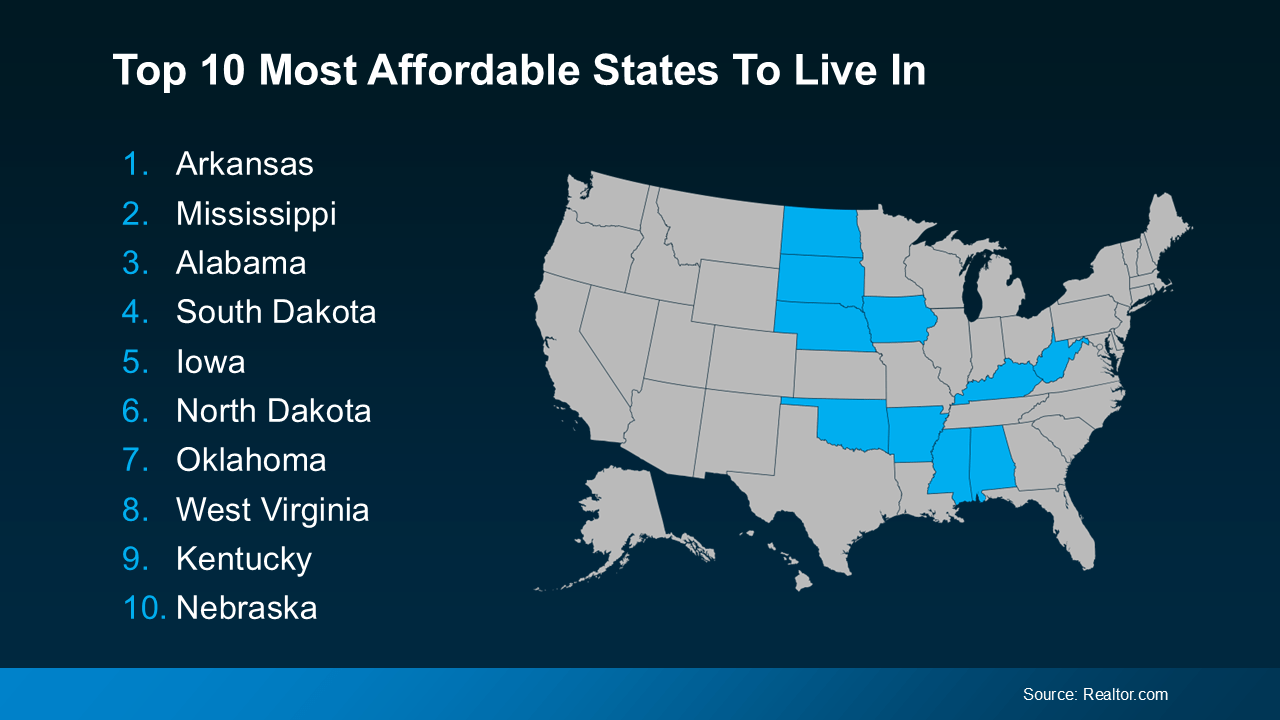

Why Moving to a More Affordable Area Makes Sense

Why Moving to a More Affordable Area Makes Sense

Moving to a more affordable area could be the fresh start you need to get ahead financially. While some markets are certainly more affordable than others, know that working with a trusted real estate agent to find what fits your budget and your desired location – no matter where you want to be – is always the best plan. And with the rising cost of living, many people are rethinking where they live and looking for ways to cut expenses. If that sounds like you, here’s a great place to start (see visual below):

These states are well known for lower housing costs, reduced insurance premiums, and more budget-friendly daily living expenses – but they’re not the only places to find a hidden gem. If you’re open to relocating, you might discover the savings you’re looking for.

These states are well known for lower housing costs, reduced insurance premiums, and more budget-friendly daily living expenses – but they’re not the only places to find a hidden gem. If you’re open to relocating, you might discover the savings you’re looking for.

Why Move to a Lower-Cost Area?

Life is getting more expensive by the day. From rising home prices to higher grocery bills, it feels like everything costs more than it used to. Housing, the largest expense for most people, has become especially costly.

In fact, according to data from Case-Shiller, home prices increased 3.9% from September 2023 to September 2024. And data from GOBankingRates shows insurance costs are up too, with home insurance premiums averaging $2,151 annually – a significant jump compared to recent years.

These rising costs can feel like a lot to handle. That’s why more people are considering lower-cost areas. An article from the National Association of Realtors (NAR) says:

“With the past decade of rising home prices, buyers are looking for more affordable areas . . . As housing affordability continues to shape migration patterns, these areas may provide an opportunity . . . for those looking for more cost-effective alternatives to the nation’s larger, pricier metropolitan areas.”

Lower-cost areas typically offer more affordable housing, less expensive home insurance, and reduced costs for daily living like groceries and gas. Transportation expenses and car insurance premiums also tend to be lower. For anyone feeling stretched thin, moving to a less expensive area can provide meaningful financial relief.

Planning Your Big Move

Whether it’s finding a home that fits your budget or cutting down on other expenses, making the right move in any market can bring significant financial relief. Of course, moving isn’t a decision to take lightly.

Whether you’re moving just a few towns over or to a completely different state, there’s a lot to consider. From job opportunities, to schools, to local amenities – it all has an impact on finding the right home for you.

This is where a knowledgeable local real estate agent can be your best resource. Not only can they help you navigate the housing market in your new or desired area, but they’ll also guide you to neighborhoods that balance affordability with your needs.

And don’t worry if none of the states on the affordability list seem like the right fit for you. An agent can still help you identify budget-friendly options wherever you need to be.

Bottom Line

If the rising cost of living has you feeling stuck, know that you have options. Moving to a more affordable area could be the fresh start you need to get ahead financially and improve your quality of life.

But don’t try to tackle the process alone. With the help of a real estate agent who knows the area, you’ll be well-prepared to make a move. When you’re ready to take the first step, let’s connect.

What Will It Take for Prices To Come Down?

What Will It Take for Prices To Come Down?

You may be wondering if home prices are going to crash. And believe it or not, some people might even be hoping this happens so they can finally purchase a more affordable home. But experts agree that’s not what’s in the cards – and here’s why.

There are more people who want to buy a home than there are homes available to purchase. That’s what drives prices up.

Let’s break that down and explore why, nationally, home prices aren’t going to be coming down anytime soon.

Prices Depend on Supply and Demand

The housing market works like any other market – when demand is high and supply is low, prices rise.

According to the latest estimates, the U.S. is facing a housing shortfall of several million homes. That means there are far more people looking to buy (demand) than there are homes for sale (supply). That mismatch is the key reason why prices won’t fall at the national level. As David Childers, President of Keeping Current Matters (KCM), puts it:

“The main driving force on pricing is the limited amount of inventory in most markets across the country. That issue is not going to be solved overnight or in the next twelve months.”

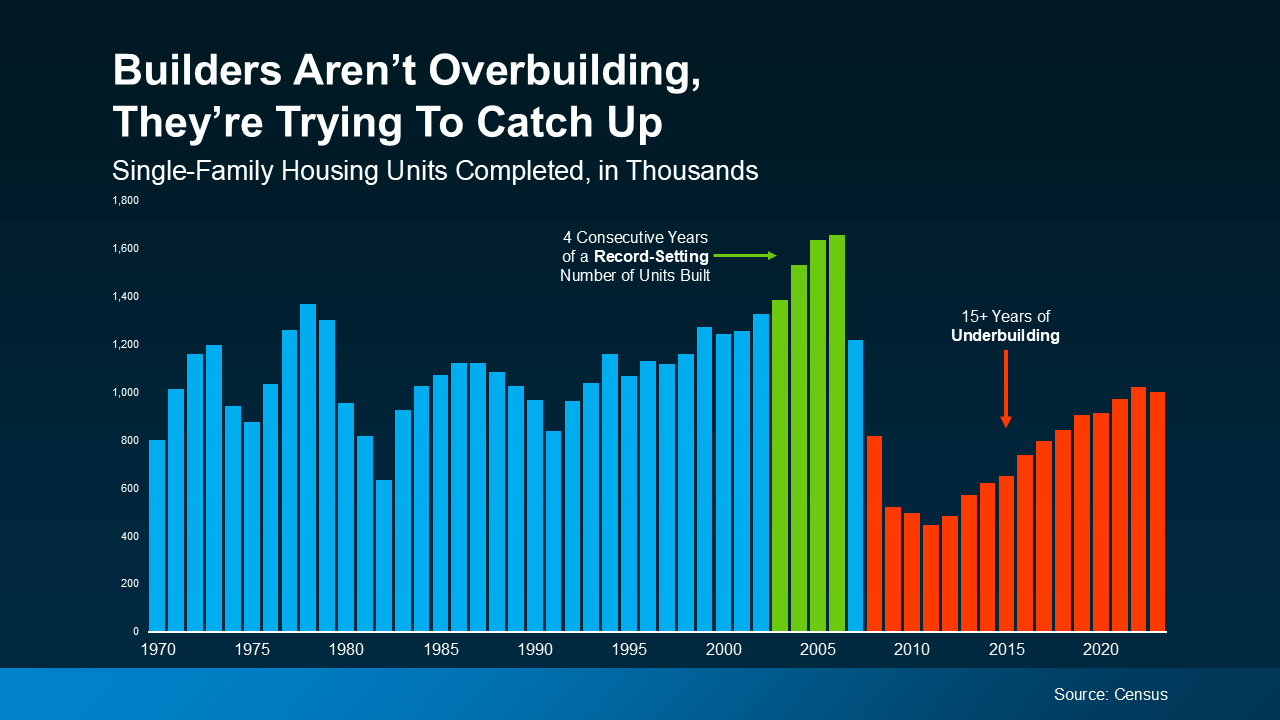

How Did We Get Here?

For over 15 years, homebuilders haven’t been building enough homes to keep up with buyer demand. After the 2008 housing crisis, homebuilding slowed significantly, and it’s only recently started to recover (see graph below):

Even with new construction on the rise over the past few years, builders are playing catch-up. And according to AmericanProgress.org, they’re still not even keeping up with today’s demand, let alone making up for years of underbuilding.

Even with new construction on the rise over the past few years, builders are playing catch-up. And according to AmericanProgress.org, they’re still not even keeping up with today’s demand, let alone making up for years of underbuilding.

And as long as there’s a housing shortage, home prices will remain steady or increase in most areas.

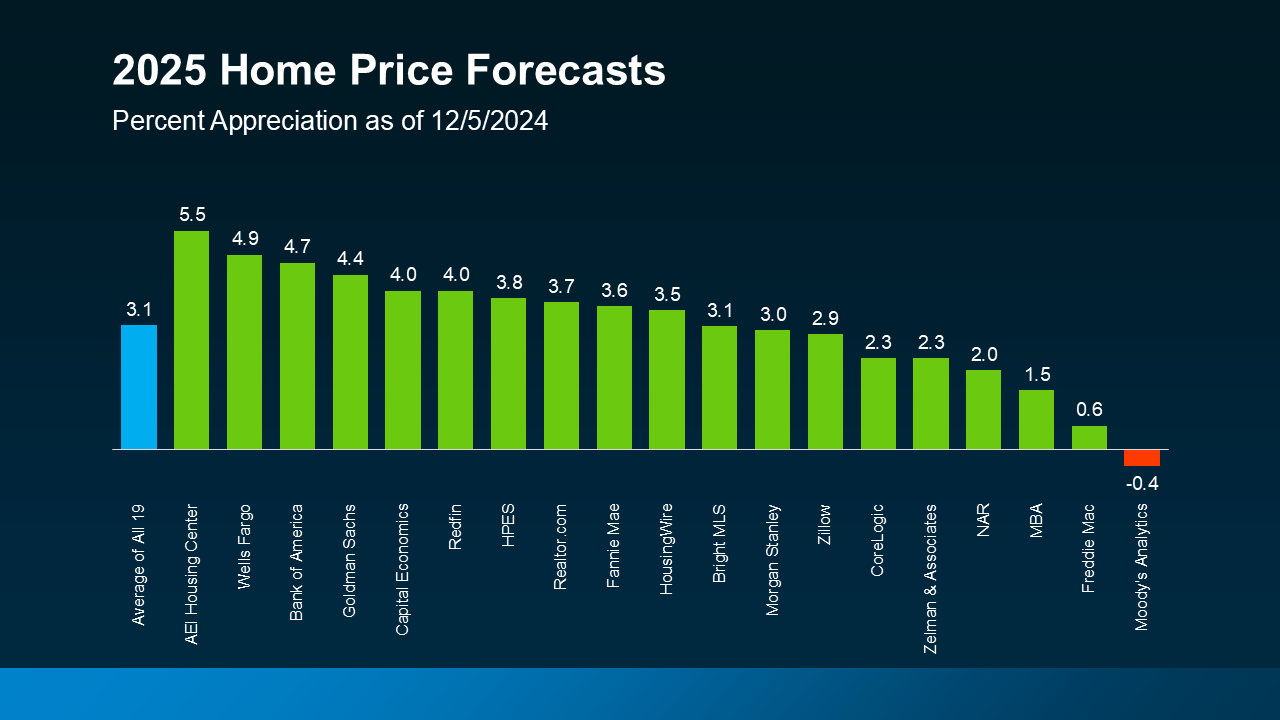

What About Next Year?

The majority of experts agree prices will keep rising next year, but at a much slower, healthier pace (see graph below):

But it’s important to note home prices vary by market. What happens nationally might not reflect exactly what’s happening in your area. If your local market has more inventory available, prices could grow more slowly or even decline slightly. But in areas where inventory remains tight, prices will keep climbing – and that’s what’s happening throughout most of the country. That’s why it’s crucial to work with a local real estate expert who understands your market and can explain what’s going on where you live.

But it’s important to note home prices vary by market. What happens nationally might not reflect exactly what’s happening in your area. If your local market has more inventory available, prices could grow more slowly or even decline slightly. But in areas where inventory remains tight, prices will keep climbing – and that’s what’s happening throughout most of the country. That’s why it’s crucial to work with a local real estate expert who understands your market and can explain what’s going on where you live.

Bottom Line

If you’re wondering what it’ll take for prices to come down, it all goes back to supply and demand. With inventory still limited in most markets, prices are likely to remain steady or rise.

To see what’s happening with home prices where we live, let’s connect. That way you’ll have help understanding our market and making a plan that works for you.

Why Owning a Home Is Worth It in the Long Run

Why Owning a Home Is Worth It in the Long Run

Today’s mortgage rates and home prices may have you second-guessing whether it’s still a good idea to buy a home right now. While market factors are definitely important, there’s also a bigger picture to consider: the long-term benefits of homeownership.

Think of it this way. If you know people who bought a home 5, 10, or even 30 years ago, you’re probably going to have a hard time finding someone who regrets their decision. That’s because over time, home values usually grow – and that means a homeowner’s net worth does too. Here’s a look at how that can really add up over the years.

Home Price Growth over Time

The map below uses data from the Federal Housing Finance Agency (FHFA) to show how much prices have grown over the last five years. Since home prices vary by area, the map is broken out regionally to really showcase larger market trends:

You can see that nationally, home prices increased by over 57% in just five years.

Some regions are slightly above or below that average, but overall, home prices saw a big uptick in a short time. And if you zoom out even more, the benefit of homeownership — and the drastic gains homeowners made over the years — become even more clear (see map below):

The second map shows that, over a roughly 30-year span, home prices appreciated by an average of more than 320% nationally.

The second map shows that, over a roughly 30-year span, home prices appreciated by an average of more than 320% nationally.

So the typical homeowner who bought a house about 30 years ago saw their home triple in value during that time. And that’s a major reason so many homeowners who bought their homes years ago are still happy with their decision today.

Bottom Line

There’s no denying today’s market is complex. But if you’re ready and able to buy right now, let’s connect to talk about how we can still make your move happen. That way you can take advantage of the long-term advantages that come with homeownership, like your ability to build wealth as your home value rises.

Today’s mortgage rates and home prices may have you second-guessing whether it’s still a good idea to buy a home right now. While market factors are definitely important, there’s also a bigger picture to consider: the long-term benefits of homeownership.

Think of it this way. If you know people who bought a home 5, 10, or even 30 years ago, you’re probably going to have a hard time finding someone who regrets their decision. That’s because over time, home values usually grow – and that means a homeowner’s net worth does too. Here’s a look at how that can really add up over the years.

Home Price Growth over Time

The map below uses data from the Federal Housing Finance Agency (FHFA) to show how much prices have grown over the last five years. Since home prices vary by area, the map is broken out regionally to really showcase larger market trends:

You can see that nationally, home prices increased by over 57% in just five years.

Some regions are slightly above or below that average, but overall, home prices saw a big uptick in a short time. And if you zoom out even more, the benefit of homeownership — and the drastic gains homeowners made over the years — become even more clear (see map below):

The second map shows that, over a roughly 30-year span, home prices appreciated by an average of more than 320% nationally.

So the typical homeowner who bought a house about 30 years ago saw their home triple in value during that time. And that’s a major reason so many homeowners who bought their homes years ago are still happy with their decision today.

Bottom Line

There’s no denying today’s market is complex. But if you’re ready and able to buy right now, let’s connect to talk about how we can still make your move happen. That way you can take advantage of the long-term advantages that come with homeownership, like your ability to build wealth as your home value rises.

When Will Mortgage Rates Come Down?

When Will Mortgage Rates Come Down?

One of the biggest questions on everyone’s minds right now is: when will mortgage rates come down? After several years of rising rates and a lot of bouncing around in 2024, we’re all eager for some relief.

While no one can project where rates will go with complete accuracy or the exact timing, experts offer some insight into what we might see going into next year. Here’s what the latest forecasts show.

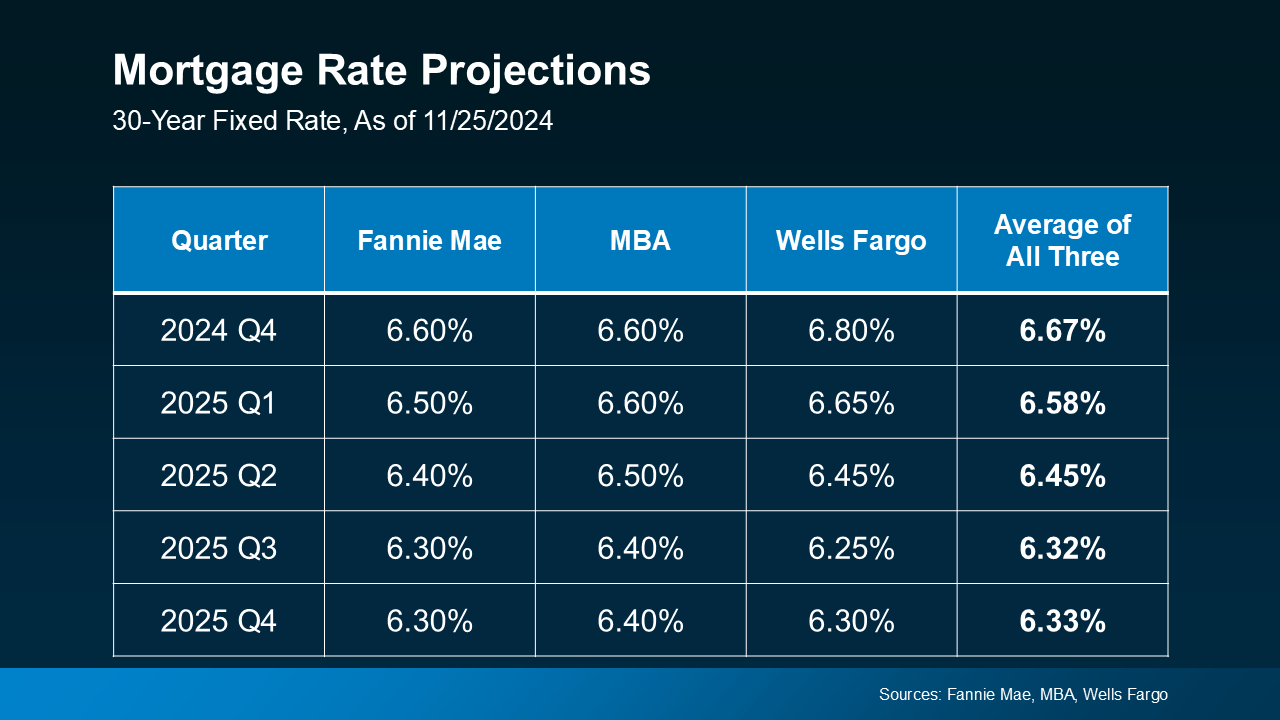

Mortgage Rates Are Expected To Ease and Stabilize in 2025

After a lot of volatility and uncertainty, the most updated forecasts suggest rates will start to stabilize over the next year, and should ease a bit compared to where they are right now (see graph below):

As Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), says:

“While mortgage rates remain elevated, they are expected to stabilize.”

Key Factors That’ll Impact the Future of Mortgage Rates

It’s important to note that the timing and the pace of what happens with mortgage rates is one of the most challenging forecasts to make in the housing market. That’s because these forecasts hinge on a few key factors all lining up. So don’t be fooled, because while rates are expected to come down slightly, they’re going to be a moving target. And the ups and downs of ongoing economic drivers will likely stick around. Here’s a look at just a few of the things that’ll influence where they go from here:

- Inflation: If inflation cools, rates could dip a bit more. On the flip side, if inflation rises or remains stubbornly high, rates may stay elevated longer.

- Unemployment Rate: The unemployment rate also plays a significant role in upcoming decisions by the Federal Reserve (the Fed). And while the Fed doesn’t set mortgage rates, their actions do reflect what’s happening in the greater economy, which can have an impact.

- Government Policies: With the next administration set to take office in January, fiscal and monetary policies could also affect how financial markets respond and where rates go from here.

Remember, these forecasts are based on the best information available right now. As new economic data comes out, experts will revise their projections accordingly. So, don’t try to time the market based on these forecasts alone.

Instead, the best thing you can do is focus on what you can control right now. Work on improving your credit score, put away any extra cash for your down payment, and automate your savings. All of these things will help you reach your homeownership goals even faster.

And be sure to connect with a trusted agent and a lender, so you always have the latest updates – and an expert opinion on what that means for your move.

Bottom Line

If you’re planning to move and want to stay informed about where mortgage rates are heading, let’s connect.

How Co-Buying a Home Helps with Affordability Today

How Co-Buying a Home Helps with Affordability Today

Buying a home in today’s market can feel like an uphill battle – especially with home prices and mortgage rates putting pressure on your budget. If you’re feeling stuck, co-buying could be one way to help you get your foot in the door. Freddie Mac says:

“If you are an aspiring homeowner, buying a home with your family or friends could be an option.”

But there are some things you’ll want to consider first. Let’s explore why co-buying is gaining popularity right now among some buyers and see if it may make sense for you too.

What Is Co-Buying?

Co-buying means buying a home with someone like a friend, sibling, or even a group of people. And, with today’s high home prices and mortgage rates, it’s an option more people are turning to.

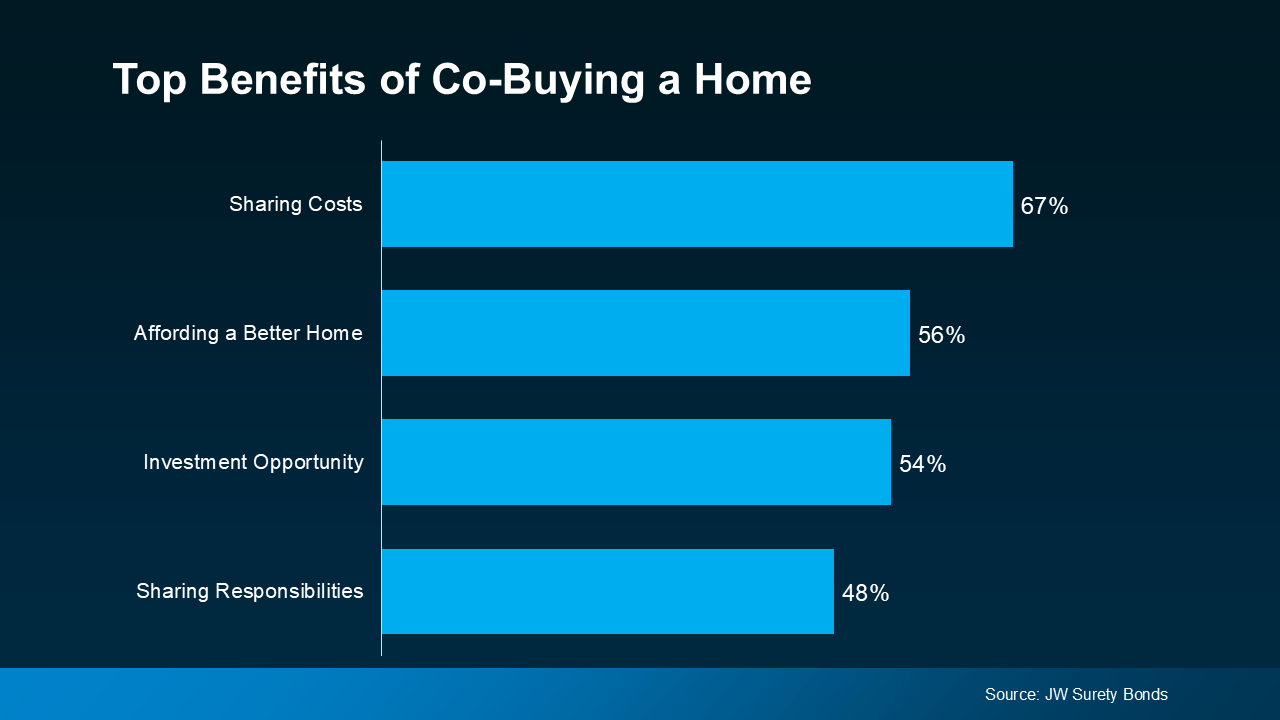

According to a survey done by JW Surety Bonds, nearly 15% of Americans have already co-purchased a home with someone, and another 48% would consider doing it.

Why Consider Co-Buying?

The same survey also asked people about the perks of co-buying a home. Here are some of the top responses (see graph below):

Sharing Costs (67%): From saving for a down payment to managing monthly payments, buying a home is a big financial step. When you co-buy, you split these costs, making it easier to afford a home.

Sharing Costs (67%): From saving for a down payment to managing monthly payments, buying a home is a big financial step. When you co-buy, you split these costs, making it easier to afford a home.

Affording a Better Home (56%): By pooling your financial resources, you may also be able to afford a larger or higher-quality home than you could have on your own. This may mean getting that extra bedroom, a bigger backyard, or living in a more desirable neighborhood.

Investment Opportunity (54%): Co-buying a home can also be an investment. You could buy a house with someone so you can rent out, which could help generate passive income.

Sharing Responsibilities (48%): Owning a home comes with a lot of responsibilities, including maintenance and upkeep and more. When you co-buy, you share these commitments, which can lighten the load for everyone involved.

Other Co-Buying Considerations

While co-buying has its benefits, there’s something else you need to consider before deciding if this approach is right for you. As Rocket Mortgage says:

“Buying a house with a friend or multiple friends might be a great way for you to achieve homeownership, but it’s not a decision you should make lightly. Before diving in, make sure you understand the financial and logistical hurdles you’ll face, as well as the human and emotional elements that might affect the purchase or, more importantly, your relationship.”

Basically, make sure you and your co-buyer are on the same page about things like how costs will be split, who will handle what responsibilities, and what will happen if one of you wants to sell your share of the home in the future. Leaning on an expert can help you weigh the pros and cons to make that conversation easier.

Bottom Line

If you’re looking to get your foot in the door but are having a tough time with today’s affordability challenges, co-buying could be an option to make your move happen. But, it’s important to plan carefully and make sure all parties are clear on the details. To figure out if co-buying makes sense for you, let’s connect.

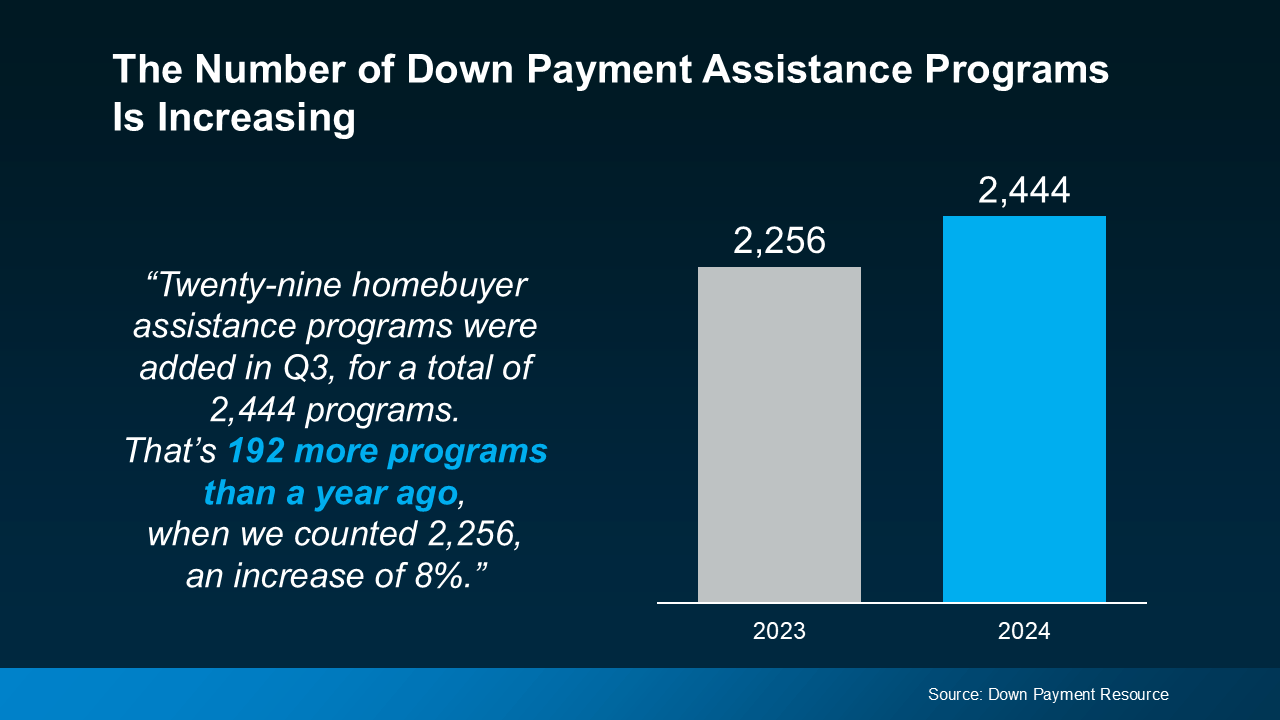

Don’t Miss Out on the Growing Number of Down Payment Assistance Programs

Don’t Miss Out on the Growing Number of Down Payment Assistance Programs

With rising home prices and volatile mortgage rates, it’s important you know about every resource that could help make buying a home possible. And one thing you’ll want to be aware of is just how much the number of down payment assistance (DPA) programs has grown lately.

Take a look at the graph below to see how many new programs have been added in the last year, according to data from Down Payment Resource:

More Programs, More Opportunities for You

More Programs, More Opportunities for You

More Programs, More Opportunities for YouSo, what does this increase mean for you? With more programs available, there’s a higher likelihood that one of them could help you reach your homeownership goals.

And these programs aren’t small-scale help either – the benefits can go a long way toward covering a chunk of your costs. As Rob Chrane, Founder and CEO of Down Payment Resource, shares:

“We are pleased to see a growing number of these programs, and think they are becoming a targeted way to help first-time and first-generation homebuyers struggling to save for a down payment get into a home they can afford. Our data shows the average DPA benefit is roughly $17,000. That can be a nice jump-start for saving for a down payment and other costs of homeownership.”

Imagine being able to qualify for $17,000 toward your down payment—that’s a big boost, especially if you’re looking to buy your first home. With that level of help, buying a home may be more within reach than you think.

But it’s worth calling out that the growth in DPA options isn’t just focused on first-time and first-generation buyers. Many of the new programs are also aimed at supporting affordable housing initiatives, which include manufactured and multi-family homes. This means that more people, and a wider variety of home types, can qualify for down payment assistance, making it easier for you to find an option that fits your needs.

Talk to a Real Estate Expert About What’s Available for You

With so many DPA programs out there, you need to make sure you’re finding the right one for you. That’s why it’s key to lean on your real estate and lending professionals for guidance. The Mortgage Reports says:

“The best way to find down payment assistance programs for which you qualify is to speak with your loan officer or broker. They should know about local grants and loan programs that can help you out.”

Your loan officer or real estate agent will know what’s available in your area and can point you toward programs that align with your goals.

Bottom Line

With more down payment assistance programs than ever before, now’s a great time to explore how these options can help on your homebuying journey. Let’s work together to make sure you’ve got a team of expert advisors in place to see which DPA programs could be a fit for you.

What’s Behind Today’s Mortgage Rate Volatility?

What’s Behind Today’s Mortgage Rate Volatility?

If you’ve been keeping an eye on mortgage rates lately, you might feel like you’re on a roller coaster ride. One day rates are up; the next they dip down a bit. So, what’s driving this constant change? Let’s dive into just a few of the major reasons why we’re seeing so much volatility, and what it means for you.

The Market’s Reaction to the Election

A significant factor causing fluctuations in mortgage rates is the general reaction to the political landscape. Election seasons often bring uncertainty to financial markets, and this one is no different. Markets tend to respond not only to who won, but also to the economic policies they are expected to implement. And when it comes to what’s been happening with mortgage rates over the past couple of weeks, as the National Association of Home Builders (NAHB) says:

“. . . the primary reason interest rates have been on the rise pertains to the uncertainty surrounding the presidential election. Although the election is now complete, there continue to be growing concerns over budget deficits.”

In the short term, this anticipation has caused a slight uptick in mortgage rates as the markets adjust and react. Additionally, factors like international tensions, supply chain disruptions, and trade policies can drive investor sentiment, causing them to seek safer assets like bonds, which can indirectly impact mortgage rates. Essentially, the more global or domestic uncertainty, the greater the chance that mortgage rates may shift.

The Economy and the Federal Reserve

Inflation and unemployment are two other big drivers of mortgage rates. The Federal Reserve (the Fed) has been working to bring inflation under control, and has been closely monitoring the economy as they do. And as long as inflation continues to moderate and the job market shows signs of maximum employment, the Fed will continue its plans to cut the Federal Funds Rate.

Although the Fed doesn’t set mortgage rates, their decisions do have an impact, and typically a cut leads to a mortgage rates response. And in their November 6-7th meeting, the Fed had the data they needed to make another cut to the Federal Funds Rate. And while that decision was expected and much of the mortgage rate movement happened prior to that meeting, there was a slight dip in rates.

What To Expect in the Coming Months

As we look ahead, mortgage rates will respond to changes in the Fed’s policies and other economic indicators. The markets will likely remain in a wait-and-see mode, reacting to each new development. And, with the transition of a new administration comes an element of unpredictability. A recent article from The Mortgage Reports explains:

“Today’s economic indicators come with mixed pressures on mortgage rates and we’re likely to be in for a good amount of volatility as markets adjust and respond to the election . . .”

The best way to navigate this landscape is to have a team of real estate experts by your side. Professionals will help you understand what’s happening and can provide you with the guidance you need to make informed housing market decisions along the way.

Bottom Line

The takeaway? Today’s mortgage rate volatility is going to continue to be driven by economic factors and political changes.

Now is the time to lean on experienced professionals. A trusted real estate agent and mortgage lender can help you navigate through it. And with the right guidance, you can make informed decisions.

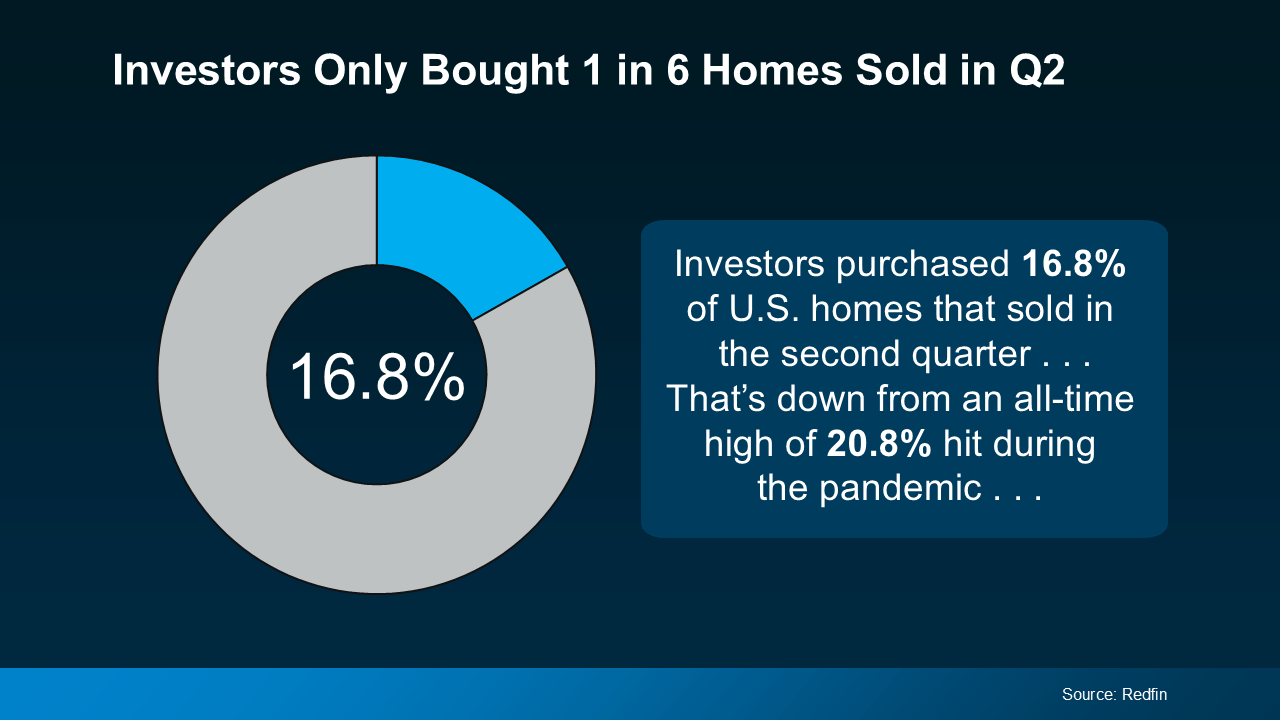

Is Wall Street Really Buying All the Homes?

Is Wall Street Really Buying All the Homes?

Let’s be real – buying a home right now is tough. You’re scrolling through listings, rushing to open houses, and maybe even losing out to more competitive offers. Somewhere along the way, you might’ve heard the reason it’s so hard to find a home is because big Wall Street investors are swooping in and snatching up everything in sight.

But here’s the thing: that’s mostly a myth. While investors are part of the market, according to Redfin, they’re a relatively small part:

Here’s what that means. Five out of every six homes are being purchased by everyday homebuyers like you – not big investors.

Here’s what that means. Five out of every six homes are being purchased by everyday homebuyers like you – not big investors.

So, before you get discouraged, let’s take a look at what’s really going on. You might be surprised to learn that Wall Street isn’t the competition you may think it is.

Most Investors Are Small Mom-and-Pops

Most investors aren’t the mega corporations you’ve probably heard about. In fact, many are your neighbors. A recent report from CoreLogic shows most investors are small, mom-and-pop types who own fewer than 10 properties. They aren’t massive companies with endless resources. Picture your neighbor who has another home they’re renting out or a vacation getaway.

Only about 1% of the market is owned by large, mega investors with thousands of properties. The majority are still owned by individuals and smaller investors – not the Wall Street giants.

Investor Purchases Are Declining

Not only are most investors small, but overall investor purchases have been on the decline. As the same report from CoreLogic says:

“Investors made 80,000 purchases in June 2024, compared with 112,000 in June 2023, and a nearly 50% percent drop from the high of 149,000 purchases in June 2021 . . .”

And what does this mean going forward? CoreLogic goes on to point out this downward trend is expected to continue into 2025.

So, if it seems like competition with investors is pushing you out of the market, it might help to know that investor activity is actually slowing down.

Bottom Line

The idea that Wall Street is buying up all the homes is largely a myth. Most investors are small ones, and the share of homes purchased by investors is declining – so you can take this one off your worry list.

If you have questions about the housing market, let’s talk.

Don’t Let These Two Concerns Hold You Back from Selling Your House

Don’t Let These Two Concerns Hold You Back from Selling Your House

If you’re debating whether or not you want to sell right now, it might be because you’ve got some unanswered questions, like if moving really makes sense in today’s market. Maybe you’re wondering if it’s even a good idea to move right now. Or you’re stressed because you think you won’t find a house you like.

To put your mind at ease, here’s how to tackle these two concerns head-on.

Is It Even a Good Idea To Move Right Now?

If you own a home already, you may have been holding off because you don’t want to sell and take on a higher mortgage rate on your next house. But your move may be a lot more feasible than you think, and that’s because of your equity.

Equity is the current market value of your home minus what you still owe on your loan. And thanks to the rapid appreciation we saw over the past few years, your equity has gotten a big boost. Just how much are we talking about? See for yourself. As Dr. Selma Hepp, Chief Economist at CoreLogic, explains:

“Persistent home price growth has continued to fuel home equity gains for existing homeowners who now average about $315,000 in equity and almost $129,000 more than at the onset of the pandemic.”

Here’s why this can be such a game-changer when you sell. You can use that equity to put down a larger amount on your next home, which means financing less at today’s mortgage rate. And in some cases, you may even be able to buy your next home in cash, avoiding mortgage rates altogether.

The bottom line? Your equity could be the key to making your next move possible.

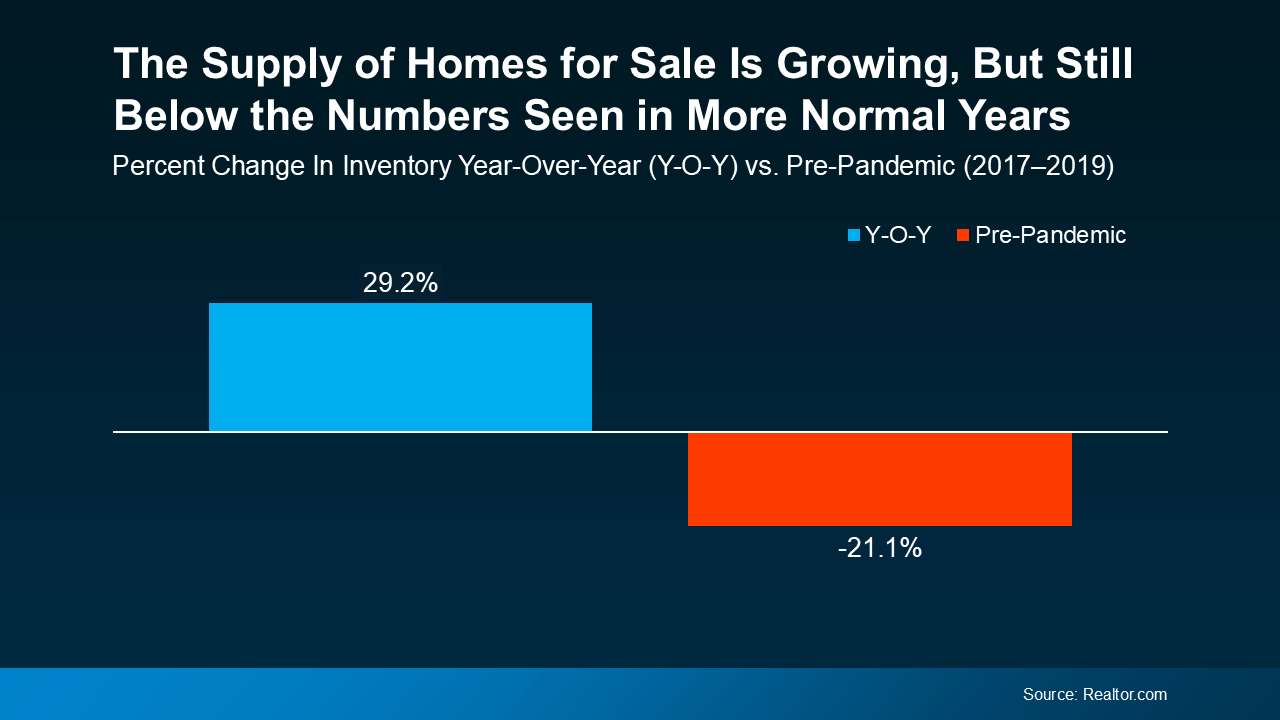

Will I Be Able To Find a Home I Like?

If this is on your mind, it’s probably because you remember just how low the supply of homes for sale got over the past few years. It felt nearly impossible to find a home to buy because there were so few available.

But finding a home in today’s market isn’t as challenging. That’s because the number of homes for sale is growing, giving you more options to choose from. Data from Realtor.com shows just how much inventory has increased – it’s up almost 30% year-over-year (see graph below):

And even though inventory is still below pre-pandemic levels, this is the highest it’s been in quite a while. That means you have more options for your move, but your house should still stand out to buyers at the same time. That’s a sweet spot for you.

And even though inventory is still below pre-pandemic levels, this is the highest it’s been in quite a while. That means you have more options for your move, but your house should still stand out to buyers at the same time. That’s a sweet spot for you.

It’s important to note, though, that this balance varies by local market. Some places may have more homes for sale than others, so working with a local real estate agent is the best way to see what inventory trends look like in your area.

Bottom Line

If you’re thinking about selling, hopefully these concerns haven’t kept you up at night. With this information, you should realize you don’t have to let the what-if’s delay your move anymore.

Let’s connect so you have the data and the local perspective you need to move forward.