| Tweet |

Don’t Fall for These Real Estate Agent Myths

Don’t Fall for These Real Estate Agent Myths

When it’s time to buy or sell a home, one of the most important decisions you’ll make is who you’ll work with as your agent. That choice will have an impact on your entire experience and how smoothly it goes.

As you figure out who you’ll partner with, it’s important to know what to expect and what to look for. Unfortunately, there may be some myths holding you back from making the best decision possible. So, let’s take some time to address those, and make sure you have the information you need to find the right agent for you.

Myth #1: All Real Estate Agents Are the Same

You might think all agents are the same – so it doesn’t matter who you work with. But, in reality, agents have varying levels of experience, specialties, and market knowledge, which can have a big impact on your results. For example: you’ll get much better service and advice from someone who is a true expert in their field. As Business Insider explains:

“If you were planning to get your hair done for a special event, you’d want to visit a stylist who specifically has experience doing that type of work — you wouldn’t make an appointment with someone who primarily does kids’ hair. The same concept applies to finding a real estate agent. If you have a smaller budget, you probably don’t want to work with an agent who exclusively sells multimillion-dollar properties.”

Take some time to talk with each agent you’re considering. Ask about their experience level and what they specialize in. This will help you find the one that’s the best fit for your search.

Myth #2: You Can Save Money by Not Using an Agent

As a seller, you may think you can save money by not working with a pro. However, the expertise, negotiation skills, and market knowledge an agent provides generally saves you money and helps you avoid making costly mistakes. Without that guidance, you could find yourself doing something like overpricing your house. And that’s a misstep that’ll cost you when it sits on the market for far too long. That’s why U.S. News Real Estate says:

“When it comes to buying or selling your home, hiring a professional to guide you through the process can save you money and headaches. It pays to have someone on your side who’s well-versed in the nuances of the market and can help ensure you get the best possible deal.”

Myth #3: Agents Will Push You To Spend More

You may also be worried an agent will push you to buy a more expensive house in order to increase their commission. But that’s not how that should go. A good agent will respect your budget and work hard to find a home that truly fits your financial situation and needs. With their market know-how, they’ll point you toward the best option for you, rather than try to pad their own pockets on your dime. As NerdWallet explains:

“Among other things, a good buyer’s agent will find homes for sale. A buyer’s agent will help you understand the type of home you can afford in the current market, find listed homes that match your needs and price range, and then help you narrow the options to the properties worth considering.”

Myth #4: Market Conditions Are the Same Everywhere, So Why Do I Need a Pro?

Maybe you believe housing market conditions are the same no matter where you are. But that couldn’t be further from the truth. Real estate markets are highly localized, and conditions can vary widely from one area to another. This is why you can’t pick just anyone you find online. You should choose an agent who’s an expert on your specific local market. As a recent article from Bankrate says:

“Real estate is very localized, and you want someone who’s extremely knowledgeable about the market in your specific area.”

You’ll know you’ve found the right person when they can explain the national trends and how your area stacks up too. That way you’re guaranteed to get the full picture when you ask: “how’s the market?”

Bottom Line

Don’t let myths keep you from the expert guidance you deserve. With market knowledge and top resources, a trusted local real estate agent isn’t just helpful, they’re invaluable.

In what could be one of the biggest financial decisions of your life, having the right pro by your side is a game changer. Let’s connect and make sure you get the best outcome possible.

Is Your House Priced Too High?

Is Your House Priced Too High?

Every seller wants to get their house sold quickly, for as much money as they can, with as few headaches as possible. And chances are, you’re no different.

But did you know one of the biggest things that could jeopardize your success is the asking price for your home? Pricing your house correctly is one of the most crucial steps in the selling process.

So, how do you know if you’re missing the mark? Here are four signs your high asking price might be turning potential buyers away—and why leaning on your real estate agent is the best way to course correct.

1. You’re Not Getting Many Showings or Offers

One of the most obvious signs your house may be overpriced is a lack of showings. If it’s been on the market for several weeks and only a few buyers have come to see it—or worse, you haven’t gotten any offers—it could be a clear indication the price isn’t matching up with what buyers expect. Because buyers who have been looking for a while can easily spot (and write off) a home that seems overpriced.

Your real estate agent will coach you through this, so lean on their experience for what you may want to try to bring more buyers in, including considering a price cut.

2. Buyers Have Consistent Negative Feedback after Showings

And if after the showings you do have, comments from the potential buyers aren’t great, you may need to course correct. Feedback from showings is an important part of understanding how buyers see your house. If they consistently say it’s overpriced compared to other homes they’ve seen, it’s time to reconsider your pricing strategy.

Your agent will gather and analyze this feedback for you, so you can look at how your house stacks up in the market. They can also suggest specific improvements or staging changes to better justify your asking price, or recommend one that aligns with today’s buyer expectations. As the National Association of Realtors (NAR) explains:

“Based on all the data gathered, agents may make adjustments to the initial price recommendation. This could involve adjusting for market conditions, property uniqueness, or other factors that may impact the property’s value.”

3. It’s Been on the Market for Too Long

And that lack of interest is ultimately going to lead to it sitting on the market without any serious bites. The longer it lingers, the more likely it is to raise red flags for buyers, who may wonder if something is wrong with it. Especially in today’s market with growing inventory, a long listing period means your house is stale – and that makes it even harder to sell.

Your real estate agent will be able to give you perspective on how quickly other homes in your area are selling and walk you through what’s working for other sellers. That way you can decide together if there’s something you want to do differently. As a Bankrate article says:

“Check with your agent about the average number of days homes spend on the market in your area. If your listing has been up significantly longer than average, that may be a sign to reduce the price.”

4. Your Neighbor’s House Sold Without an Issue

And here’s the last one to watch out for. If similar homes in your area are selling faster than yours, it’s a clear sign that something is off. This could be due to things like a lack of upgrades, outdated features, or a less desirable location. Or, it may be priced too high.

Your agent will keep you up to date on your competition and what changes, if any, you need to make your home more competitive. They’ll offer advice on small updates that could increase your home’s appeal or how to adjust your strategy to reflect the reality of the market today.

Bottom Line

Pricing a home correctly is both an art and a science. It requires a deep understanding of the market and buyer psychology. And when the price isn’t drawing in buyers, there’s no better resource than your agent on what you may want to do next.

The Real Story Behind What’s Happening with Home Prices

The Real Story Behind What’s Happening with Home Prices

If you’re wondering what’s going on with home prices lately, you’re definitely not the only one. With so much information out there, it can be hard to figure out your next move.

As a buyer, you might be worried about paying more than you should. And if you’re thinking of selling, you might be concerned about not getting the price you’re aiming for.

So, here’s a quick breakdown to help clear things up and show you what’s really happening with prices—whether you’re thinking about buying or selling.

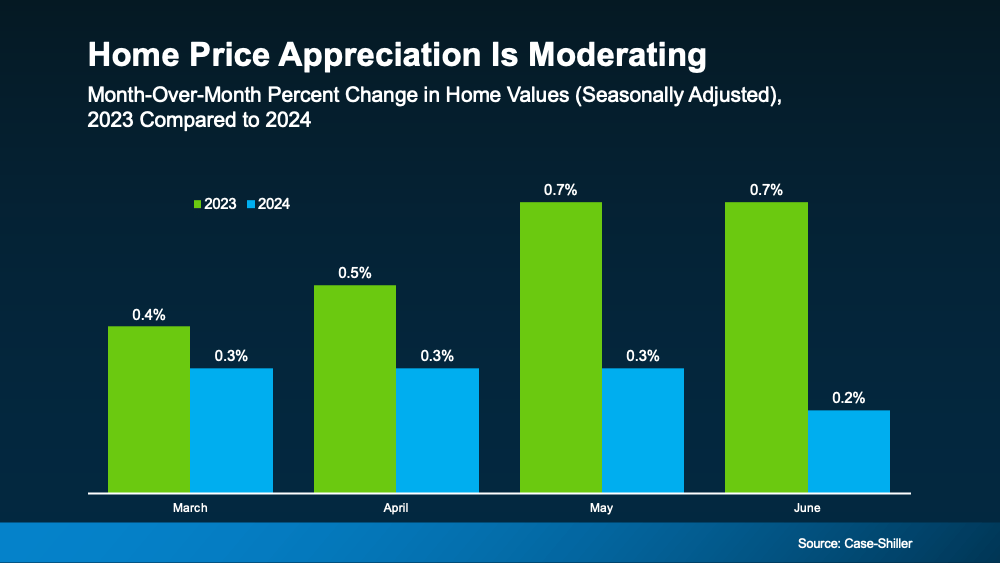

Home Price Growth Is Slowing, but Prices Aren’t Falling Nationally

Throughout the country, home price appreciation is moderating. What that means is, prices are still going up, but they’re not rising as quickly as they were in recent years. The graph below uses data from Case-Shiller to make the shift from 2023 to 2024 clear:

But rest assured, this doesn’t mean home prices are falling. In fact, all the bars in this graph show price growth. So, while you might hear talk of prices cooling, what that really means is they’re not climbing as fast as they were when they skyrocketed just a few years ago.

But rest assured, this doesn’t mean home prices are falling. In fact, all the bars in this graph show price growth. So, while you might hear talk of prices cooling, what that really means is they’re not climbing as fast as they were when they skyrocketed just a few years ago.

What’s Next for Home Prices? It’s All About Supply and Demand

You might be curious where prices will go from here. The answer depends on supply and demand, and it’s going to vary by local market.

Nationally, the number of homes for sale is going up, but there still aren’t enough of them to meet today’s buyer demand. That’s keeping upward pressure on prices – even though recent inventory growth has caused that home price appreciation to slow. Danielle Hale, Chief Economist at Realtor.com, said:

“. . . today’s low but quickly improving for-sale inventory has ushered in more market balance than would otherwise be expected . . . This should help home prices maintain a slower pace of growth.”

And here’s one other thing you may not have considered that could play a role in where prices go from here. Since experts say mortgage rates should continue to decline, it’s likely more buyers will re-enter the market in the months ahead. If demand picks back up, that could make prices climb a bit further.

Why You Should Work with a Local Real Estate Agent

While national trends give a big-picture view, real estate is always local – especially when it comes to prices. What’s happening in your neighborhood might be different from the national average based on what supply and demand look like in your market. That’s why it’s crucial to get local insights from a knowledgeable real estate agent.

As your go-to source for everything related to home prices, a local agent can provide the most current data and trends specific to your area.

So, if you’re planning to sell, they can help you price your house accurately. And when you’re ready to buy, they can find the right home that fits your budget and your needs.

Bottom Line

Home prices are still rising, just not as quickly as before. Whether you’re thinking about buying, selling, or just curious about what your house is worth, let’s connect so you have the personalized guidance you need.

The Surprising Amount of Home Equity You’ve Gained over the Years

The Surprising Amount of Home Equity You’ve Gained over the Years

There are a number of reasons you may be thinking about selling your house. And as you weigh your options, you may find you’re unsure how you’re going to deal with one thing about today’s housing market – and that’s affordability. If that’s your biggest concern, understanding how much equity you have in your house could help make your decision that much easier. Here are two key factors that have a big impact on your equity.

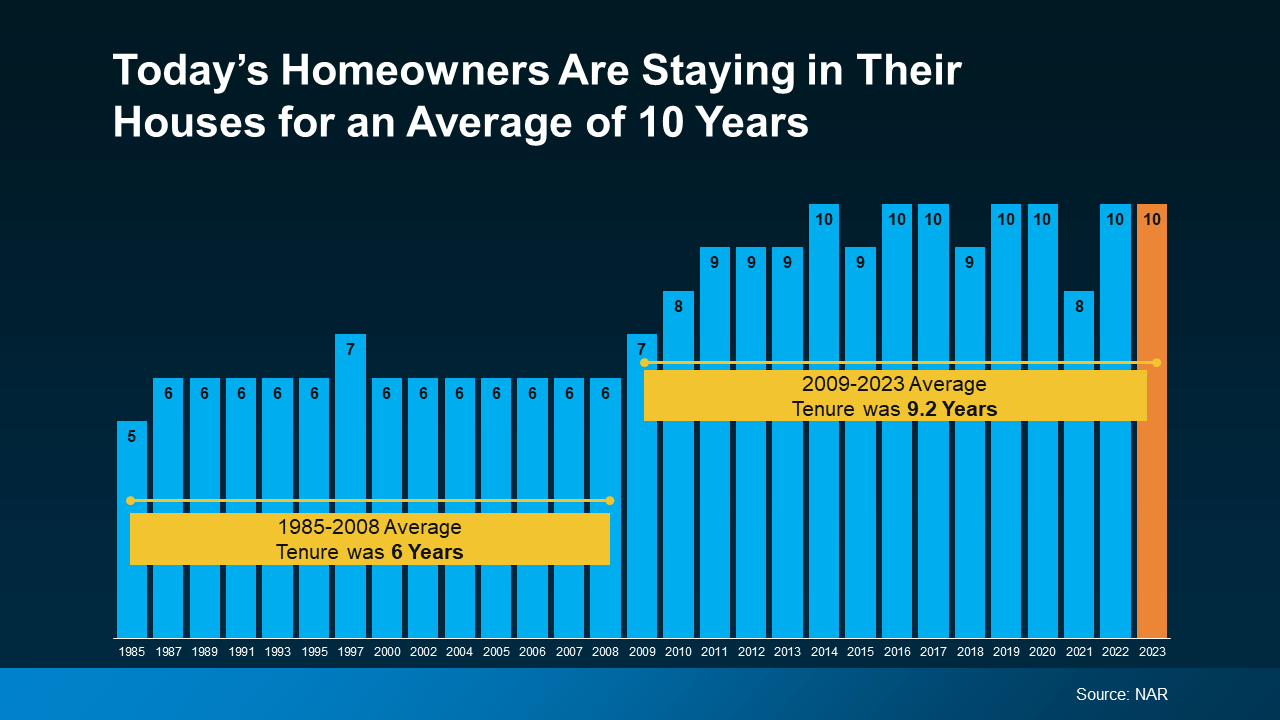

How Long You’ve Been in Your Home

First up is homeowner tenure. That’s how long homeowners live in a house, on average, before selling or choosing to move. From 1985 to 2009, the average length of time homeowners stayed put was roughly six years.

But according to the National Association of Realtors (NAR), that number has been climbing. Now, the average tenure is 10 years (see graph below):

Here’s why that’s such a big deal. You gain equity as you pay down your home loan and as home prices climb. And when you combine all of your mortgage payments with how much prices have gone up over the span of 10 years, that adds up. So, if you’ve lived in your house for a while now, you may be sitting on a pile of equity.

Here’s why that’s such a big deal. You gain equity as you pay down your home loan and as home prices climb. And when you combine all of your mortgage payments with how much prices have gone up over the span of 10 years, that adds up. So, if you’ve lived in your house for a while now, you may be sitting on a pile of equity.

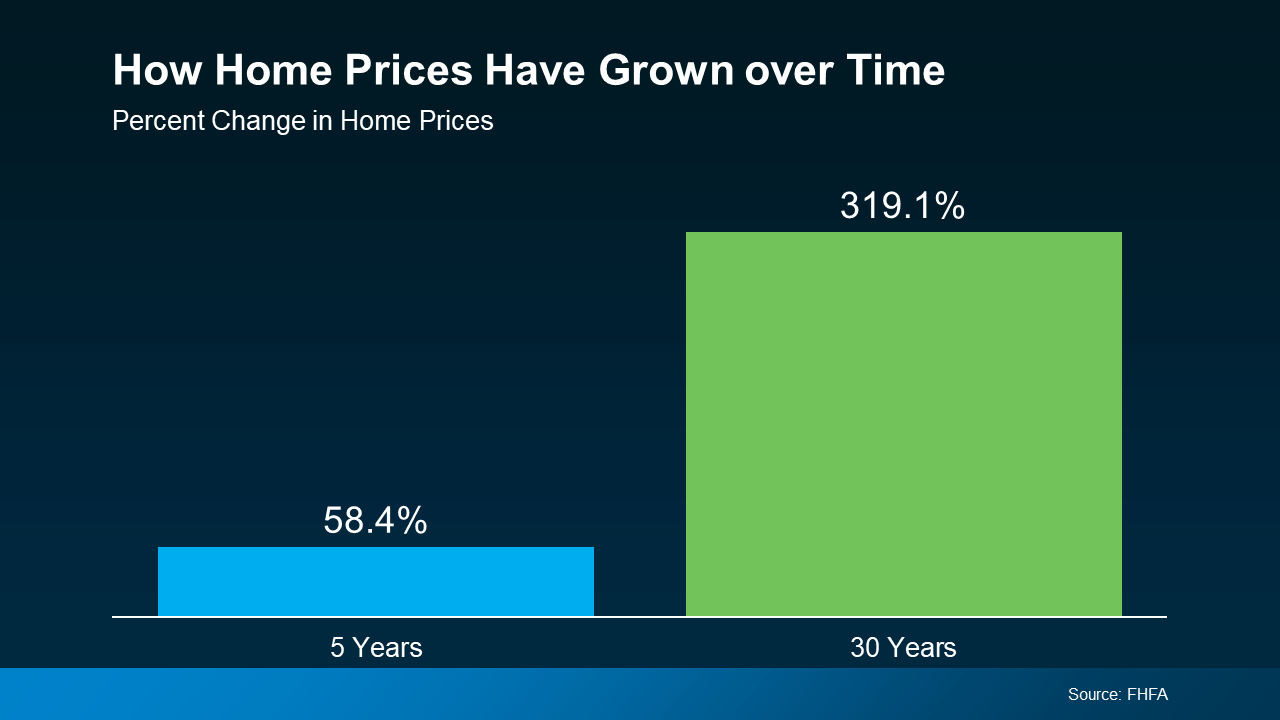

How Home Prices Appreciate over Time

To help show how much the price appreciation piece adds up, take a look at this data from the Federal Housing Finance Agency (FHFA) (see graph below):

Here’s what this means for you. While home prices vary by area, the typical homeowner who’s been in their house for five years saw it increase in value by nearly 60%. And the average homeowner who’s owned their home for 30 years saw it more than triple in value in that time.

Here’s what this means for you. While home prices vary by area, the typical homeowner who’s been in their house for five years saw it increase in value by nearly 60%. And the average homeowner who’s owned their home for 30 years saw it more than triple in value in that time.

Whether you’re looking to downsize, relocate to a dream destination, or move so you can live closer to friends or loved ones, your equity can be a game changer.

Bottom Line

If you want to find out how much equity you’ve built up over the years and how you can use it to buy your next home, let’s connect.

The Latest on the Luxury Home Market

The Latest on the Luxury Home Market

Luxury living is about more than just stunning views and cutting-edge smart home technology—it’s about elevating your lifestyle. And if you’re in the market for a million-dollar home, now is an excellent time to explore the thriving luxury market. Here’s why.

The Number of Luxury Homes Is Growing

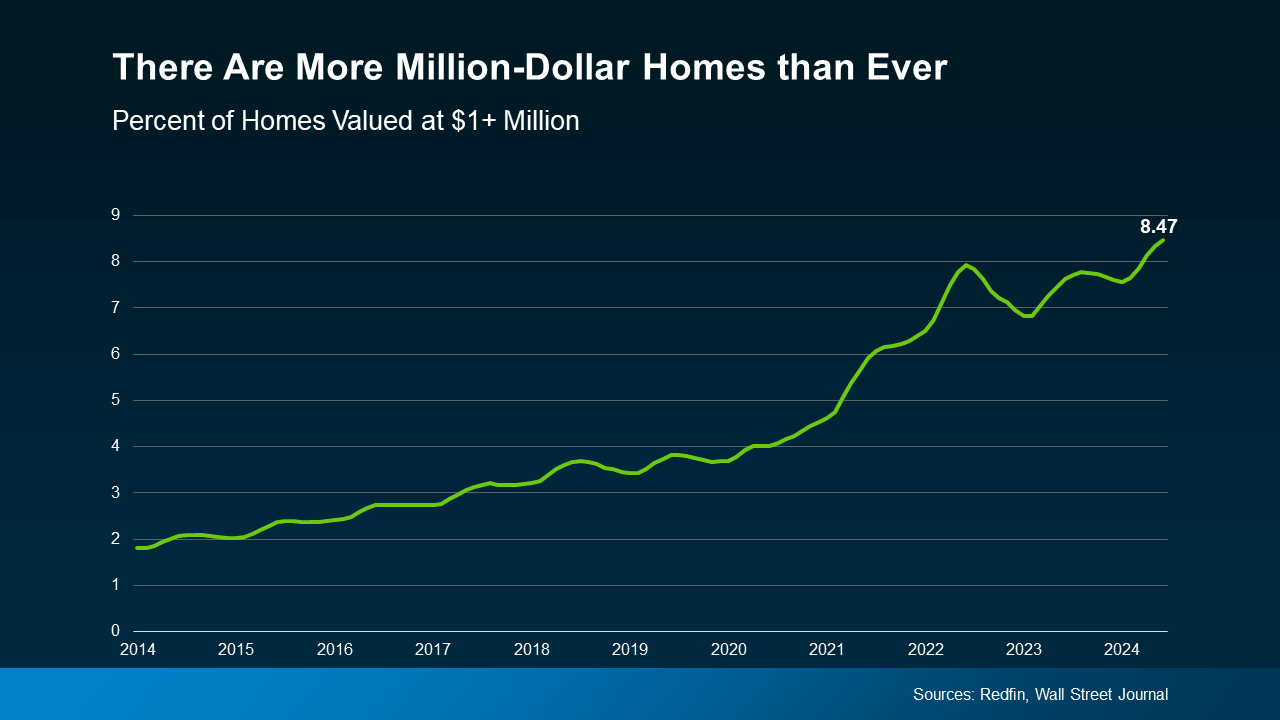

The top of the market, or luxury homes, can mean different things depending on where you live. But in general, these are homes that are in the top 5% price range in any area. According to a recent report from Redfin, the average value of those homes has risen to over one million dollars:

“The median sale price for U.S. luxury homes, defined as the top 5% of listings, rose 9% year-over-year to a record $1.18 million during the second quarter.”

That same report goes on to show the percentage of homes valued at a million dollars or more has risen to an all-time high (see graph below):

That means, if this is your desired price range, you have options to choose from, each with different features and styles.

That means, if this is your desired price range, you have options to choose from, each with different features and styles.

Whether you’re looking for the latest designs, like modern kitchens with high-end appliances, exclusive amenities, or enhanced privacy and security, the market that fits this lifestyle is growing.

Your Luxury Home Is an Investment

In addition, a luxury home could help you build significant long-term wealth. As the Redfin quote mentioned earlier says, luxury home prices are rising. That may be the reason there are a lot of people investing in luxury real estate right now. According to the August Luxury Market Report:

“By the end of July, the overall growth in the volume of sales in 2024 stood at 14.82% for single-family homes and 11.35% for attached homes compared to the same period in 2023.”

Bottom Line

With more million-dollar homes on the market and prices going up, you have luxury options to choose from and a chance to build significant long-term wealth. Want to see the best homes in our area? Let’s get in touch today.

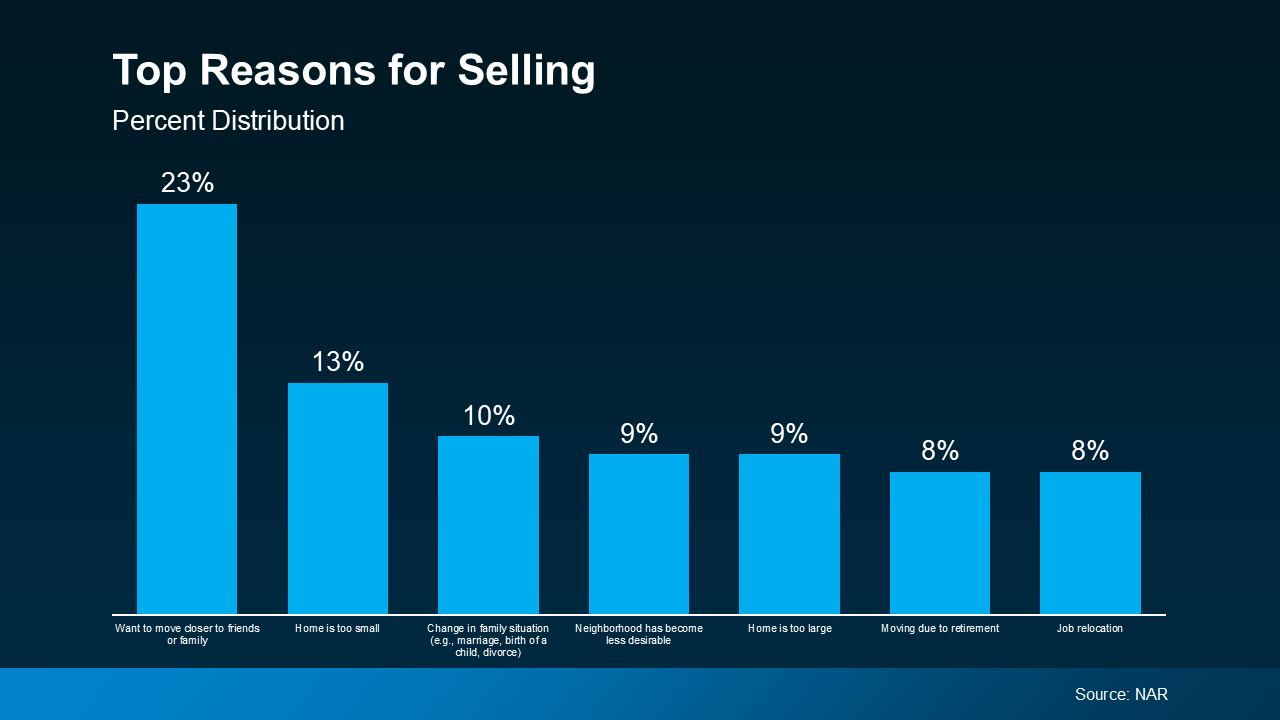

Should You Sell Now? The Lifestyle Factors That Could Tip the Scale

Should You Sell Now? The Lifestyle Factors That Could Tip the Scale

Are you on the fence about whether to sell your house now or hold off? It’s a common dilemma, but here’s a key point to consider: your lifestyle might be the biggest factor in your decision. While financial aspects are important, sometimes the personal motivations for moving are reason enough to make the leap sooner rather than later.

An annual report from the National Association of Realtors (NAR) offers insight into why homeowners like you chose to sell. All of the top reasons are related to life changes. As the graph below highlights:

As the visual shows, the biggest motivators were the desire to be closer to friends or family, outgrowing their current house, or experiencing a significant life change like getting married or having a baby. The need to downsize or relocate for work also made the list.

As the visual shows, the biggest motivators were the desire to be closer to friends or family, outgrowing their current house, or experiencing a significant life change like getting married or having a baby. The need to downsize or relocate for work also made the list.

If you, like the homeowners in this report, find yourself needing features, space, or amenities your current home just can’t provide, it may be time to consider talking to a real estate agent about selling your house. Your needs matter. That agent will walk you through your options and what you can expect from today’s market, so you can make a confident decision based on what matters most to you and your loved ones.

Your agent will also be able to help you understand how much equity you have and how it can make moving to meet your changing needs that much easier. As Danielle Hale, Chief Economist at Realtor.com, explains:

“A consideration today’s homeowners should review is what their home equity picture looks like. With the typical home listing price up 40% from just five years ago, many home sellers are sitting on a healthy equity cushion. This means they are likely to walk away from a home sale with proceeds that they can use to offset the amount of borrowing needed for their next home purchase.”

Bottom Line

Your lifestyle needs may be enough to motivate you to make a change. If you want help weighing the pros and cons of selling your house, let’s have a conversation.

Could a 55+ Community Be Right for You?

Could a 55+ Community Be Right for You?

If you’re thinking about downsizing, you may be hearing about 55+ communities and wondering if they’d be a good fit for you. Here’s some information that could help you make your decision.

What Is a 55+ Community?

It’s important to note that these communities aren’t just for people who need extra support – they can be pretty vibrant, too. Many people who are downsizing opt for this type of home because they’re looking to be surrounded by people in a similar season of life. U.S. News explains:

“The terms ‘55-plus community,’ ‘active adult community,’ ‘lifestyle communities’ and ‘planned communities’ refer to a setting that caters to the needs and preferences of adults over the age of 55. These communities are designed for seniors who are able to care for themselves but may be looking to downsize to a community with others their same age and with similar interests.”

Why It’s Worth Considering This Type of Home

If that sounds like something that may interest you, here’s one thing to consider. You may find you’ve got a growing list of options if you look at this type of community. According to 55places.com, the number of listings tailored for homebuyers in this age group has increased by over 50% compared to last year.

And a bigger pool of options could make your move much less stressful because it’s easier to find something that’s specifically designed to meet your needs.

Other Benefits of 55+ Communities

On top of that, there are other benefits to seeking out this type of home. An article from 55places.com, highlights just a few:

- Lower-Maintenance Living: Tired of mowing the lawn or pulling weeds? Many of these communities take care of this for you. So, you can spend more time doing fun things, and less time on maintenance.

- On-Site Amenities: Some feature lifestyle amenities like a clubhouse, fitness center, and more, so it’s easy to stay active. Plus, others offer media rooms, libraries, spas, arts and craft studios, and more.

- Like-Minded Neighbors: Additionally, these types of homes usually offer clubs, outings, meet-ups, and more to foster a close-knit community.

- Accessible Floor Plans: Not to mention, many have first-floor living options, ample storage spaces, and modern floor plans so you can have a home tailored to this phase in your life.

Bottom Line

If this sounds appealing to you, let’s talk about what’s available in our area, and the unique amenities for each community. You may find a 55+ home is exactly what you’ve been searching for.

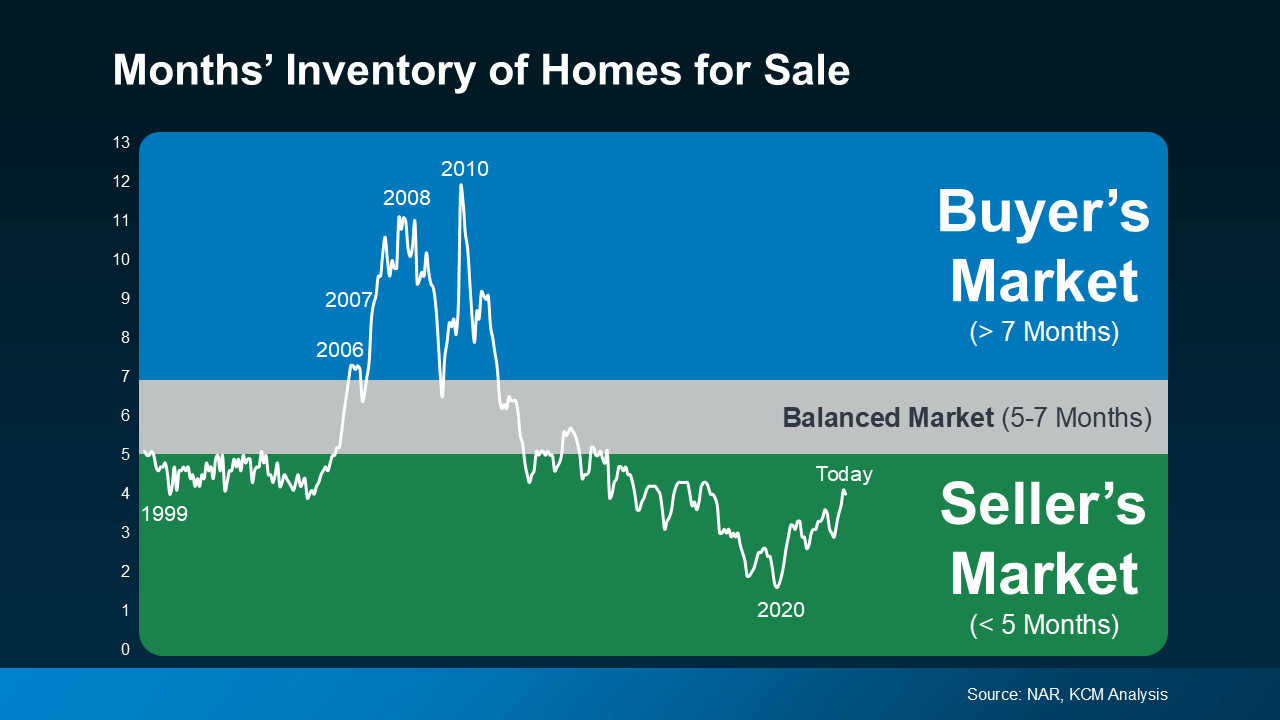

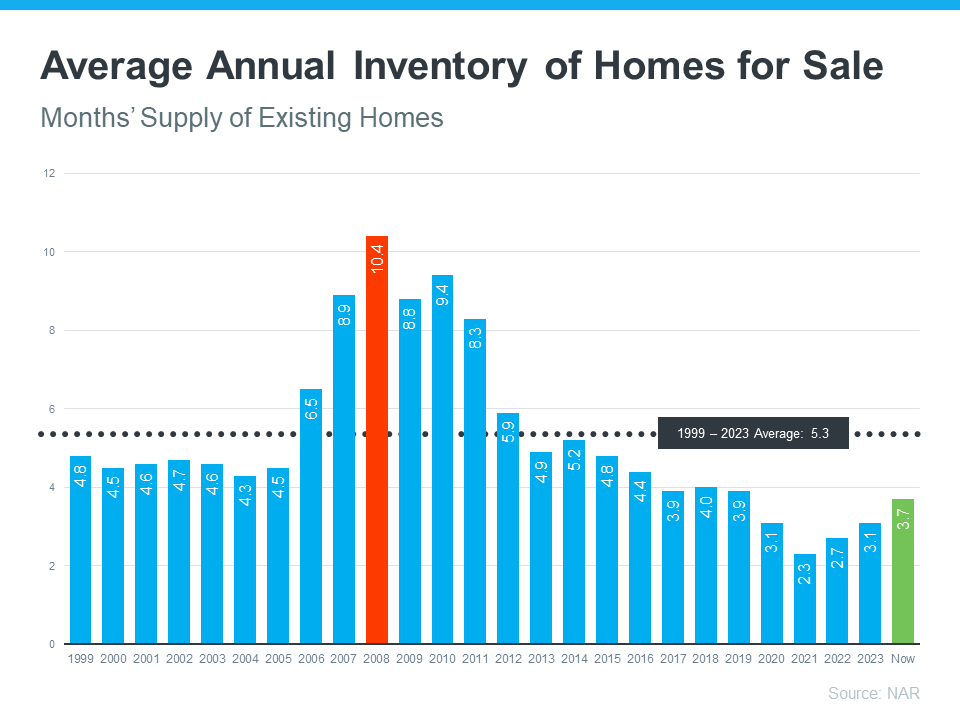

Are We Heading into a Balanced Market?

Are We Heading into a Balanced Market?

If you’ve been keeping an eye on the housing market over the past couple of years, you know sellers have had the upper hand. But is that going to shift now that inventory is growing? Here’s a breakdown of what you need to know.

What Is a Balanced Market?

A balanced market is generally defined as a market with about a five-to-seven-month supply of homes available for sale. In this type of market, neither buyers nor sellers have a clear advantage. Prices tend to stabilize, and there’s a healthier number of homes to choose from. And after many years when sellers had all the leverage, a more balanced market would be a welcome sight for people looking to move. The question is – is that really where the market is headed?

After starting the year with a three-month supply of homes nationally, inventory has increased to four months. That may not sound like a lot, but it means the market is getting closer to balanced – even though it’s not quite there yet. It’s important to note this increase in inventory is not leading to an oversupply that would cause a crash. Even with the growth lately, there’s still nowhere near enough supply for that to happen.

The graph below uses data from the National Association of Realtors (NAR) to give you an idea of where inventory has been in the past, and where it’s at today:

For now, this is still seller’s market territory – it’s just not as frenzied of a seller’s market as it’s been over the past few years. As Mark Fleming, Chief Economist at First American, says:

For now, this is still seller’s market territory – it’s just not as frenzied of a seller’s market as it’s been over the past few years. As Mark Fleming, Chief Economist at First American, says:

“The faster housing supply increases, the more affordability improves and the strength of a seller’s market wanes.”

What This Means for You and Your Move

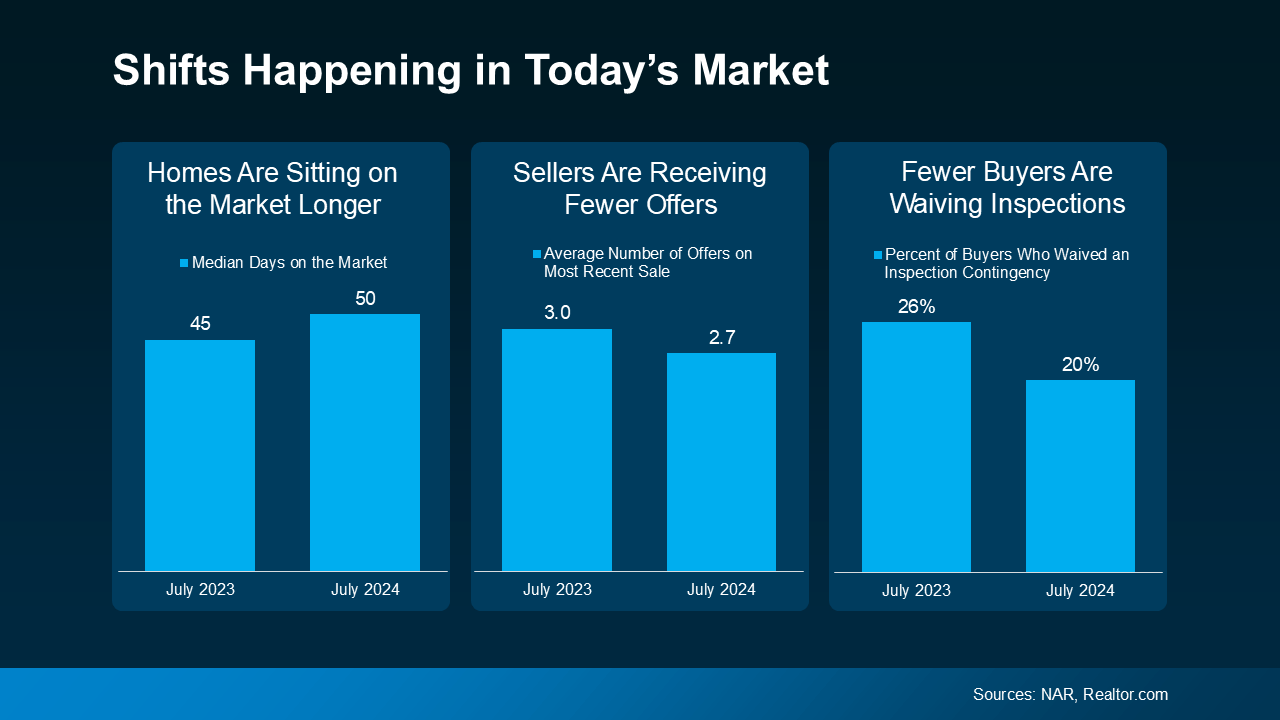

Here’s how this shift impacts you and the market conditions you’ll face when you move. Lawrence Yun, Chief Economist at NAR, explains:

“Homes are sitting on the market a bit longer, and sellers are receiving fewer offers. More buyers are insisting on home inspections and appraisals, and inventory is definitively rising on a national basis.”

The graphs below use the latest data from NAR and Realtor.com to help show examples of these changes:

Homes Are Sitting on the Market Longer: Since more homes are on the market, they’re not selling quite as fast. For buyers, this means you may have more time to find the right home. For sellers, it’s important to price your house right if you want it to sell. If you don’t, buyers might choose better-priced options.

Homes Are Sitting on the Market Longer: Since more homes are on the market, they’re not selling quite as fast. For buyers, this means you may have more time to find the right home. For sellers, it’s important to price your house right if you want it to sell. If you don’t, buyers might choose better-priced options.

Sellers Are Receiving Fewer Offers: As a seller, you might need to be more flexible and willing to compromise on price or terms to close the deal. For buyers, you could start to face less intense competition since you have more options to choose from.

Fewer Buyers Are Waiving Inspections: As a buyer, you have more negotiation power now. And that’s why fewer buyers are waiving inspections. For sellers, this means you need to be ready to negotiate and address repair requests to keep the sale moving forward.

How a Real Estate Agent Can Help

But this is just the national picture. The type of market you’re in is going to vary a lot based on how much inventory is available. So, lean on a local real estate agent for insight into how your area stacks up.

Whether you’re buying or selling, understanding how the market is changing gives you a big advantage. Your agent has the latest data and local insights, so you know exactly what’s happening and how to navigate it.

Bottom Line

The real estate market is always changing, and it’s important to stay informed. Whether you’re buying or selling, understanding this shift toward a balanced market can help. If you have any questions or need expert advice, don’t hesitate to reach out.

2025 Housing Market Forecasts: What To Expect

2025 Housing Market Forecasts: What To Expect

Looking ahead to 2025, it’s important to know what experts are projecting for the housing market. And whether you’re thinking of buying or selling a home next year, having a clear picture of what they’re calling for can help you make the best possible decision for your homeownership plans.

Here’s an early look at the most recent projections on mortgage rates, home sales, and prices for 2025.

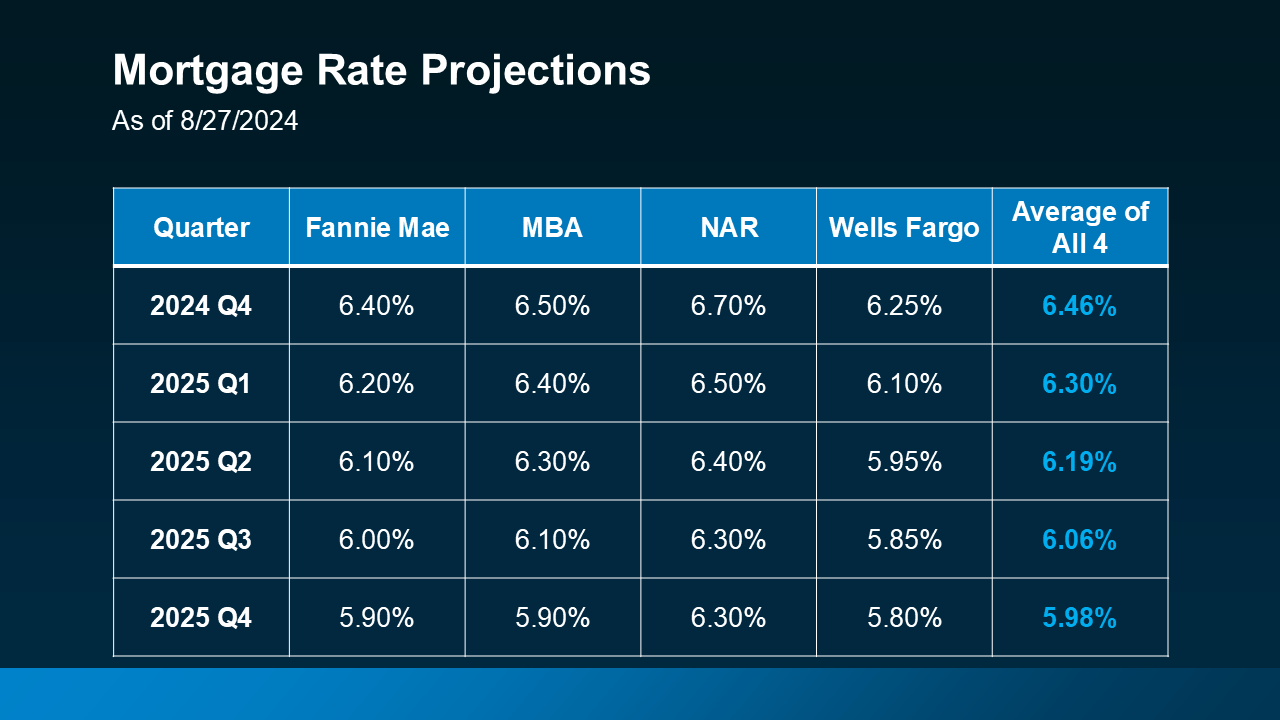

Mortgage Rates Are Projected To Come Down Slightly

Mortgage rates play a significant role in the housing market. The forecasts for 2025 from Fannie Mae, the Mortgage Bankers Association (MBA), the National Association of Realtors (NAR), and Wells Fargo show an expected gradual decline in mortgage rates over the course of the next year (see chart below):

Mortgage rates are projected to come down because continued easing of inflation and a slight rise in unemployment rates are key signs of a strong but slowing economy. And many experts believe these signs will encourage the Federal Reserve to lower the Federal Funds Rate, which tends to lead to lower mortgage rates. As Morgan Stanley says:

Mortgage rates are projected to come down because continued easing of inflation and a slight rise in unemployment rates are key signs of a strong but slowing economy. And many experts believe these signs will encourage the Federal Reserve to lower the Federal Funds Rate, which tends to lead to lower mortgage rates. As Morgan Stanley says:

“With the U.S. Federal Reserve widely expected to begin cutting its benchmark interest rate in 2024, mortgage rates could drop as well—at least slightly.”

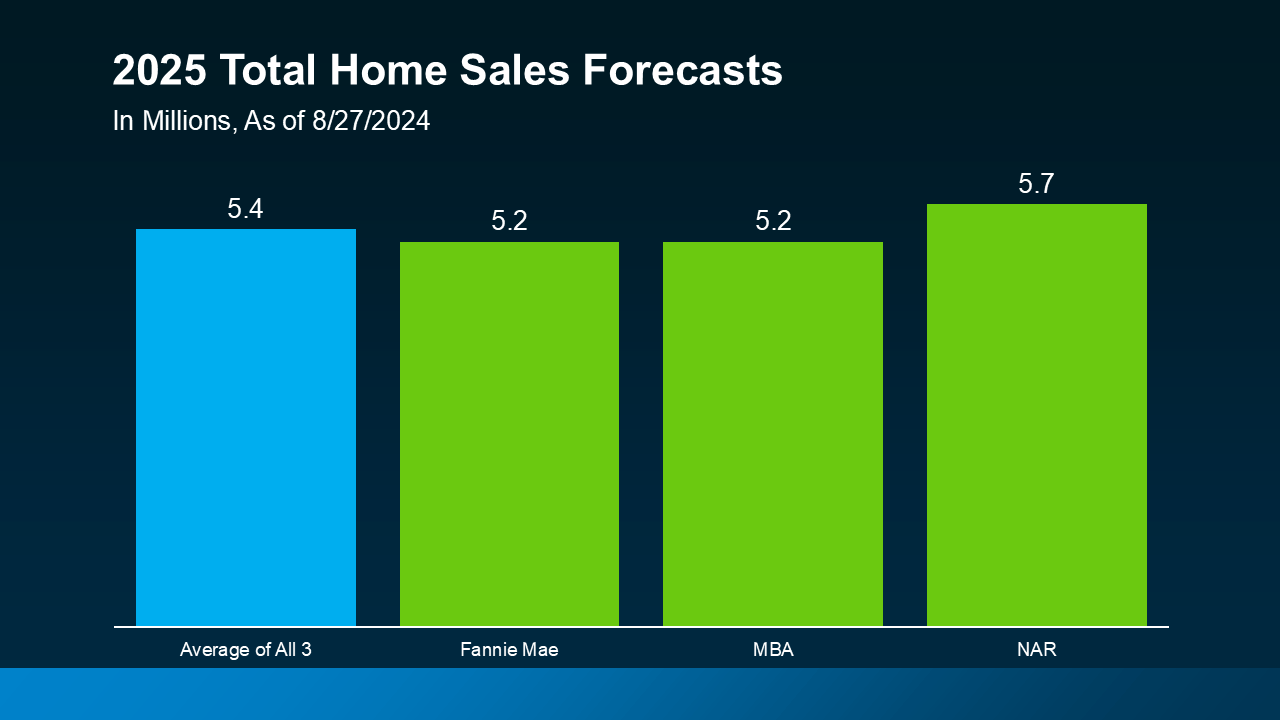

Expect More Homes To Sell

The market will see an increase in both the supply of available homes on the market, as well as a rise in demand, as more buyers and sellers who have been sitting on the sidelines because of higher rates choose to make a move. That’s one big reason why experts are projecting an increase in home sales next year.

According to Fannie Mae, MBA, and NAR, total home sales are forecast to climb slightly, with an average of about 5.4 million homes expected to sell in 2025 (see graph below):

That would represent a modest uptick from the lower sales numbers in 2023 and 2024. For reference, about 4.8 million total homes were sold in 2023, and expectations are for around 4.5 million homes to sell this year.

That would represent a modest uptick from the lower sales numbers in 2023 and 2024. For reference, about 4.8 million total homes were sold in 2023, and expectations are for around 4.5 million homes to sell this year.

While slightly lower mortgage rates are not expected to bring a flood of buyers and sellers back to the market, they certainly will get more people moving. That means more homes available for sale – and competition among buyers who want to purchase them.

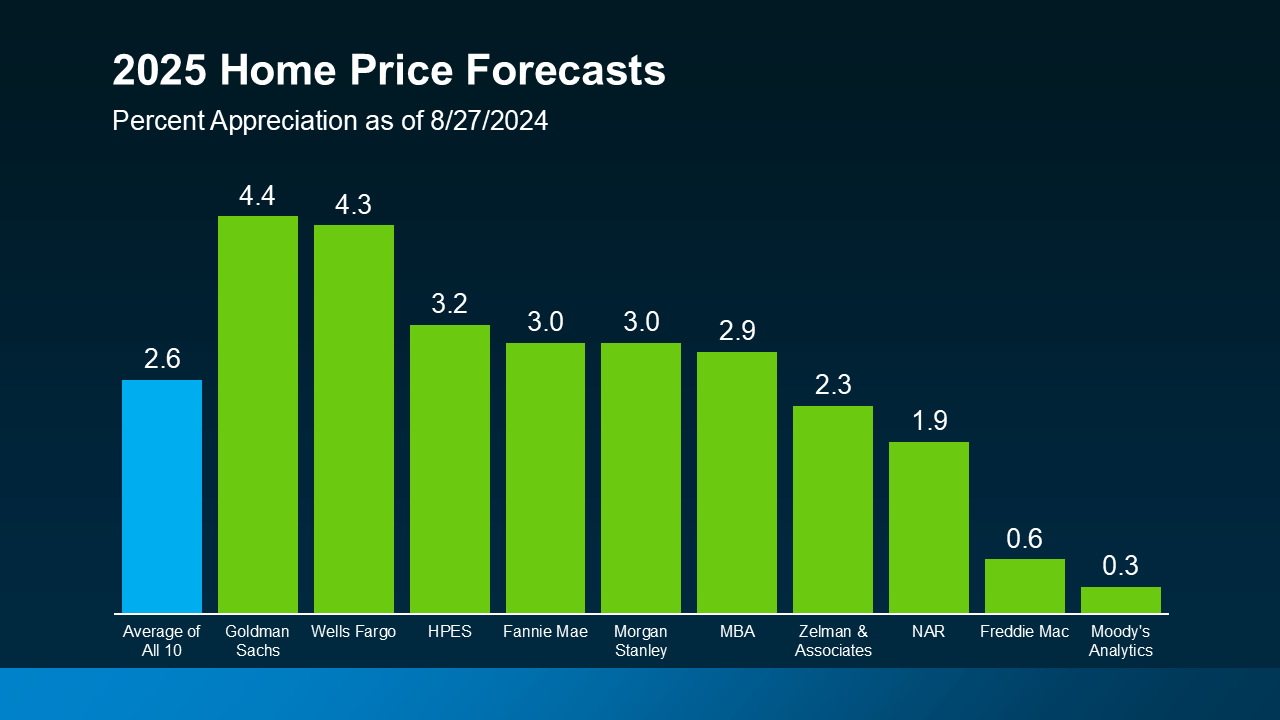

Home Prices Will Go Up Moderately

More buyers ready to jump into the market will put continued upward pressure on prices. Take a look at the latest price forecasts from 10 of the most trusted sources in real estate (see graph below):

On average, experts forecast home prices will rise nationally by about 2.6% next year. But as you can see, there’s a range of opinions on how much prices will climb. Experts agree, however, that home prices will continue to increase moderately next year at a slower, more normal rate. But keep in mind, prices will always vary by local market.

On average, experts forecast home prices will rise nationally by about 2.6% next year. But as you can see, there’s a range of opinions on how much prices will climb. Experts agree, however, that home prices will continue to increase moderately next year at a slower, more normal rate. But keep in mind, prices will always vary by local market.

Bottom Line

Understanding 2025 housing market forecasts can help you plan your next move. Whether you’re buying or selling, staying informed about these trends will ensure you make the best decision possible. Let’s connect to discuss how these forecasts could impact your plans.

What’s the Impact of Presidential Elections on the Housing Market?

What’s the Impact of Presidential Elections on the Housing Market?

It’s no surprise that the upcoming Presidential election might have you speculating about what’s ahead. And those unanswered thoughts can quickly spiral, causing fear and uncertainty to swirl through your mind. So, if you’ve been considering buying or selling a home this year, you’re probably curious about what the election might mean for the housing market – and if it’s still a good time to make your move.

Here’s the good news that may surprise you: typically, Presidential elections have only had a small, temporary impact on the housing market. But your questions are definitely worth answering, so you don’t have to pause your plans in the meantime.

Here’s a look at decades of data that shows exactly what’s happened to home sales, prices, and mortgage rates in previous Presidential election cycles, so you can move forward with the facts as you weigh the pros and cons of your homeownership decision.

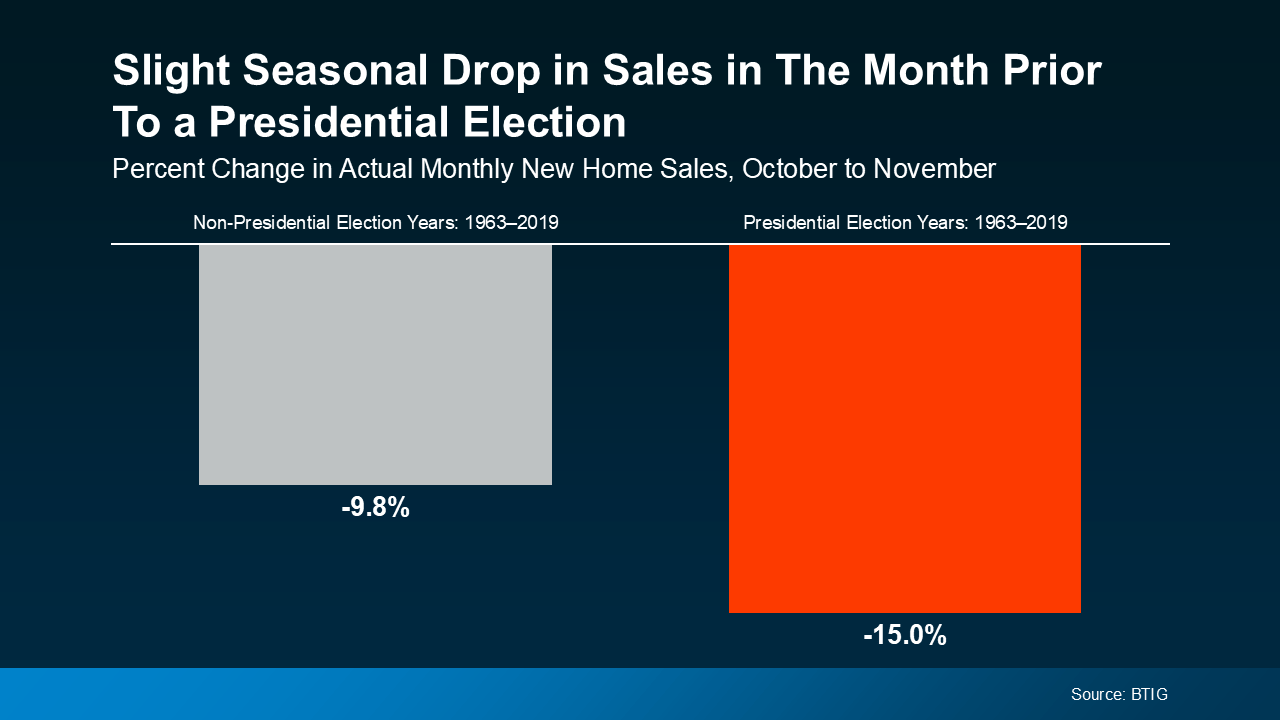

Home Sales

In the month leading up to a Presidential election, from October to November, there’s typically a slight slowdown in home sales (see graph below):

Some consumers will simply wait it out before they make their purchase decision. However, it’s important to know this slowdown is small and temporary.

Some consumers will simply wait it out before they make their purchase decision. However, it’s important to know this slowdown is small and temporary.

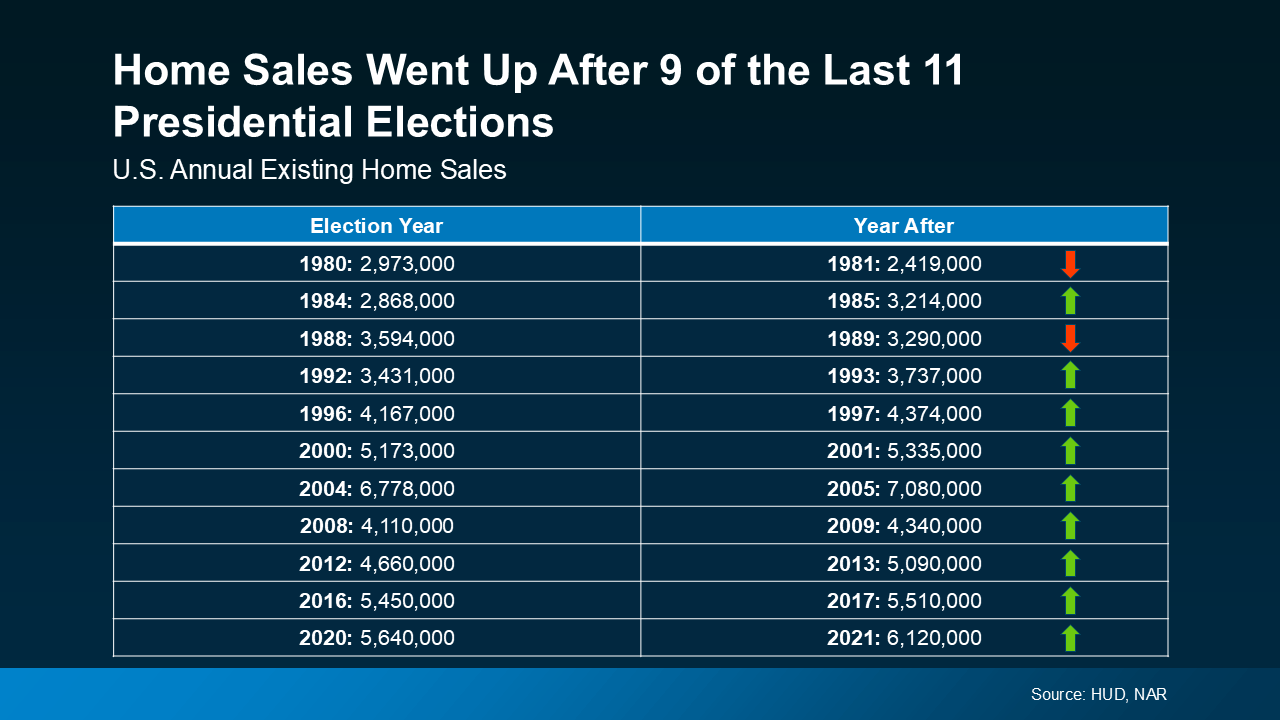

Historically, home sales bounce right back and continue to rise the following year.

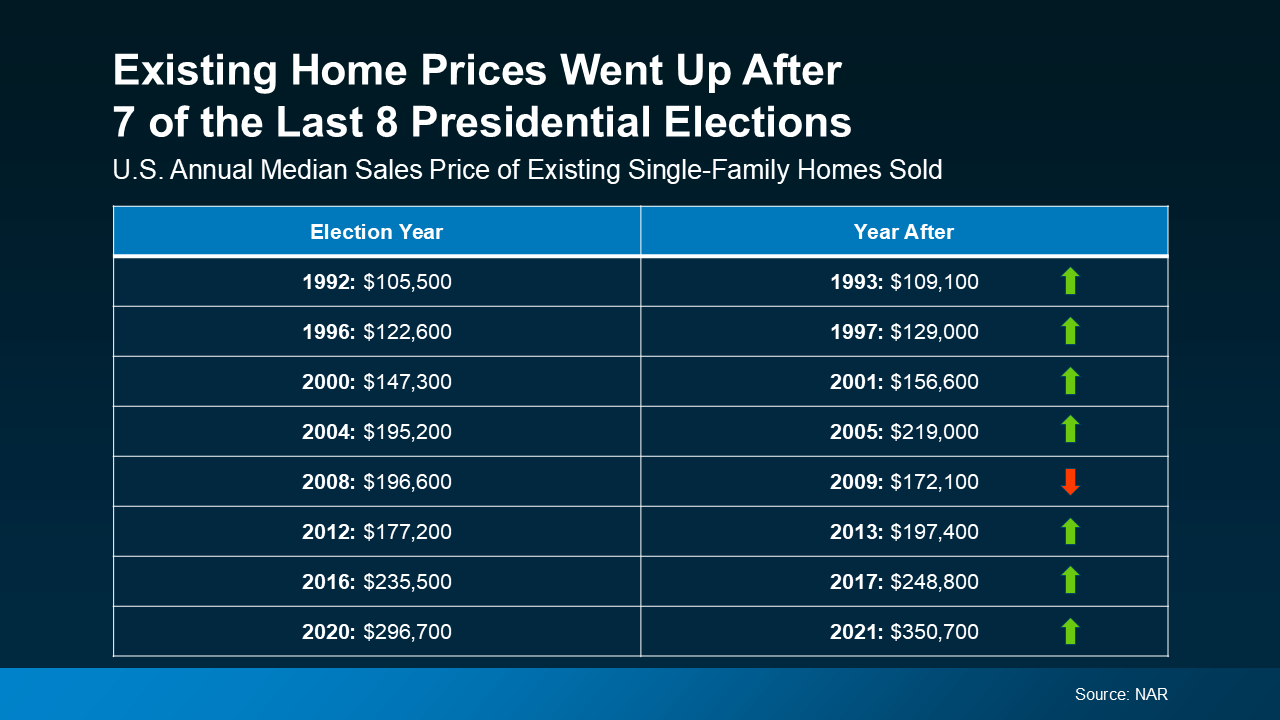

In fact, data from the Department of Housing and Urban Development (HUD) and the National Association of Realtors (NAR) shows after 9 of the last 11 Presidential elections, home sales went up the year after the election, and it’s been happening consistently since the early 1990s (see chart below):

Home Prices

Home Prices

Home Prices

Home PricesYou may also be wondering about home prices. Do prices come down during election years? Not typically. As residential appraiser and housing analyst Ryan Lundquist notes:

“An election year doesn’t alter the price trend that is already happening in the market.”

Home prices generally rise over time, regardless of an election cycle. So, based on what history shows, you can expect the current pricing trend in your local market to likely continue, barring any unusual market or economic circumstances.

The latest data from NAR reveals that after 7 of the last 8 Presidential elections, home prices increased the following year (see chart below):

The one outlier was from 2008 to 2009, which was during the height of the housing market crash. That was certainly not a typical year. Today’s market, however, is much more resilient. And while prices are moderating nationally, they aren’t on an overall decline.

The one outlier was from 2008 to 2009, which was during the height of the housing market crash. That was certainly not a typical year. Today’s market, however, is much more resilient. And while prices are moderating nationally, they aren’t on an overall decline.

Mortgage Rates

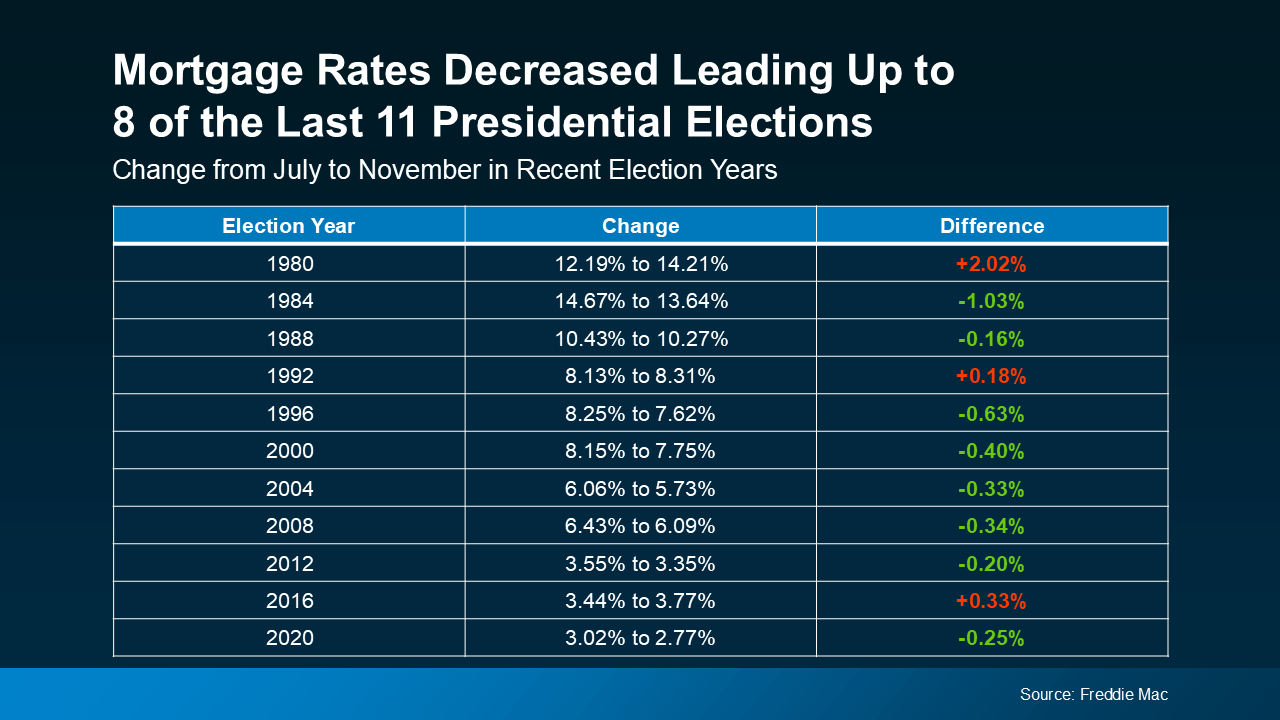

And the third thing that’s likely on your mind is mortgage rates, since they impact your monthly payment if you’re financing a home. Looking at the last 11 Presidential election years, data from Freddie Mac shows mortgage rates decreased from July to November in 8 of them (see chart below):

And this year, we’ve already started to see that happen. Most experts also forecast mortgage rates will ease slightly throughout the rest of 2024. If that happens – and all signs right now indicate it should – this year will continue to follow the trend of declining rates. So, if you’re looking to buy a home in the coming months, this could be great news for your purchasing power.

And this year, we’ve already started to see that happen. Most experts also forecast mortgage rates will ease slightly throughout the rest of 2024. If that happens – and all signs right now indicate it should – this year will continue to follow the trend of declining rates. So, if you’re looking to buy a home in the coming months, this could be great news for your purchasing power.

What This Means for You

What’s the big takeaway? While Presidential elections do have some impact on the housing market, the effects are usually minimal. As Lisa Sturtevant, Chief Economist at Bright MLS, says:

“Historically, the housing market doesn’t tend to look very different in presidential election years compared to other years.”

For most buyers and sellers, elections don’t have a major impact on their plans.

Bottom Line

While it’s natural to feel a bit uncertain during an election year, history shows the housing market remains strong and resilient. And this means you don’t have to pause your plans in the meantime. For help navigating the market during this election cycle, let’s connect.

Today’s Biggest Housing Market Myths

Today’s Biggest Housing Market Myths

Have you ever heard the phrase: don’t believe everything you hear? That’s especially true if you’re thinking about buying or selling a home in today’s housing market. There’s a lot of misinformation out there. And right now, making sure you have someone you can go to for trustworthy information is extra important.

If you partner with a real estate agent, they can clear up some common misconceptions and reassure you by backing them up with research-driven facts. Here are just a few misconceptions they can help disprove.

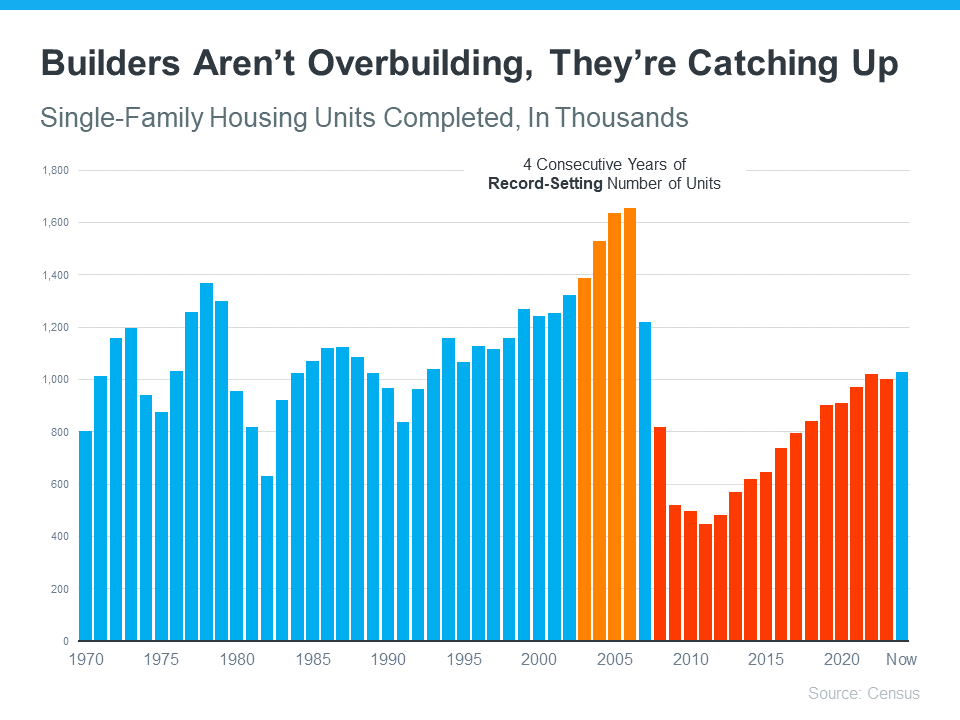

1. I’ll Get a Better Deal Once Prices Crash

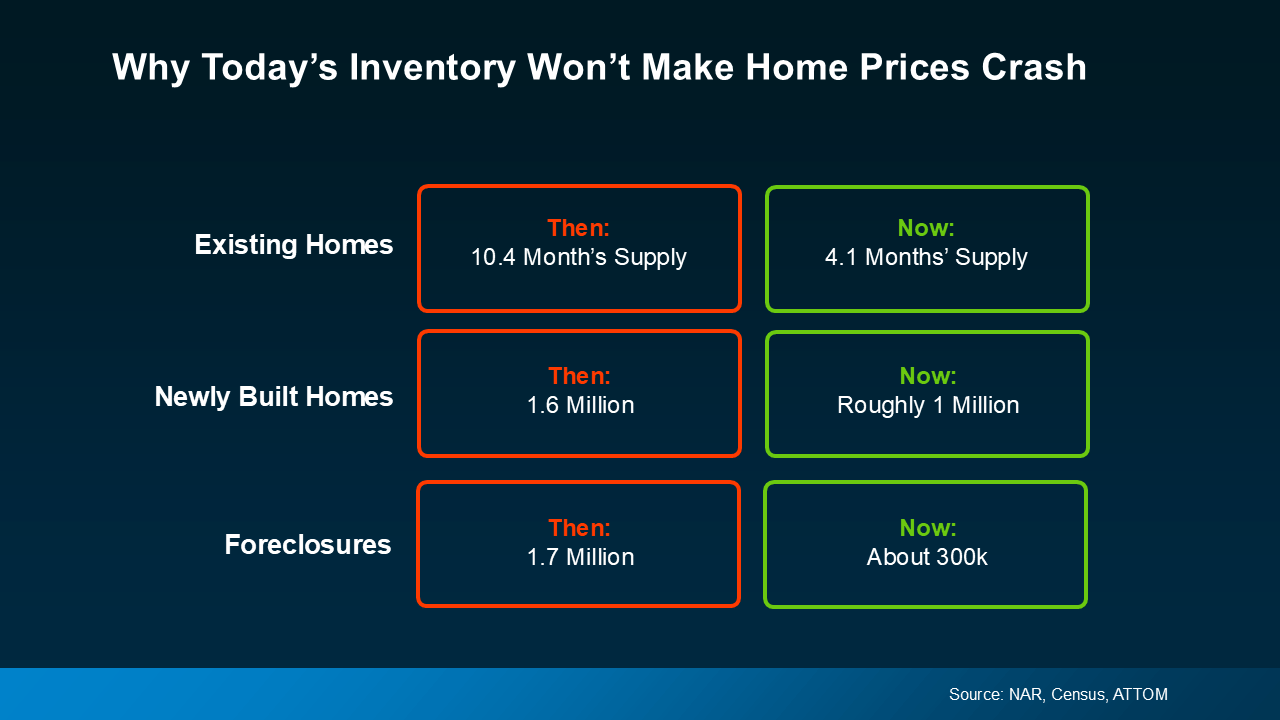

If you’ve heard home prices are going to come crashing down, it’s time to look at what’s actually happening. While prices vary by local market, there’s a lot of data out there from numerous sources that shows a crash is not going to happen. Back in 2008, there was a dramatic oversupply of homes that led to prices crashing. Across the board, there’s an undersupply of homes for sale today. That makes this market a whole different scenario (see chart below):

So, if you think waiting will score you a deal, know that data shows there’s not a crash on the horizon, and waiting isn’t going to pay off the way you’d hoped.

So, if you think waiting will score you a deal, know that data shows there’s not a crash on the horizon, and waiting isn’t going to pay off the way you’d hoped.

2. I Won’t Be Able To Find Anything To Buy

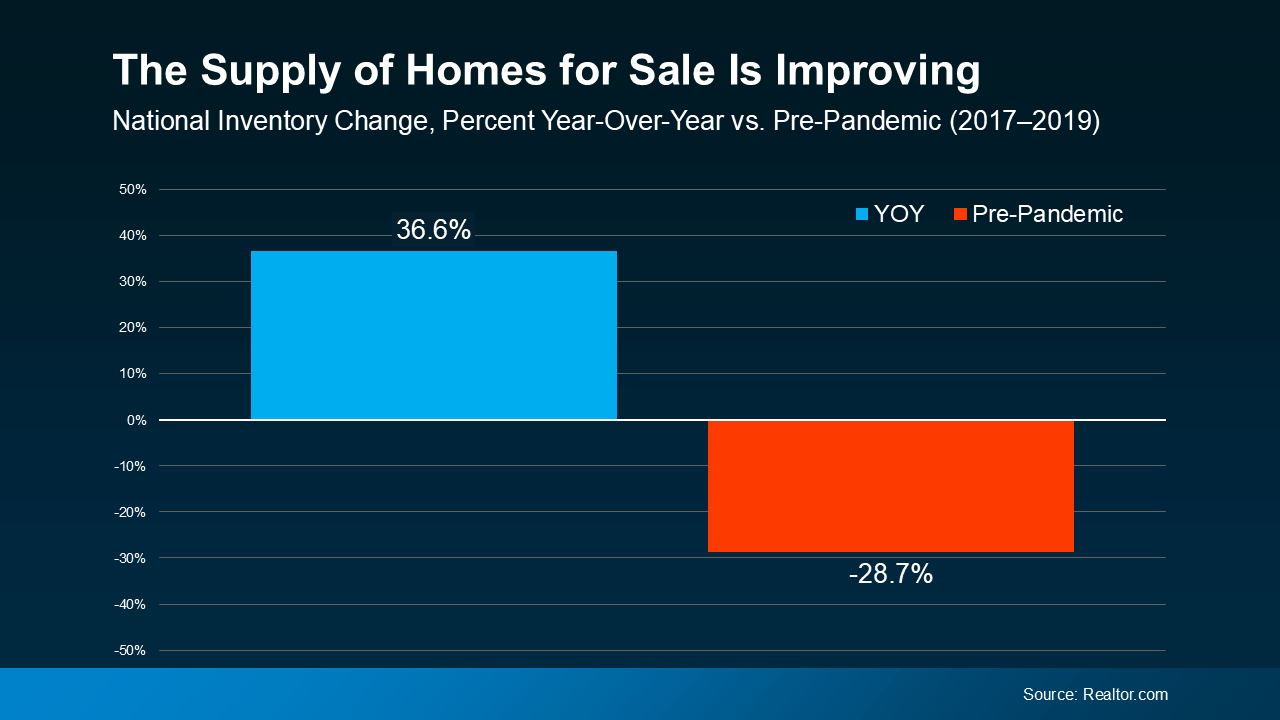

If this nagging fear about finding the right home if you move is still holding you back, you probably haven’t talked with an expert real estate agent lately. Throughout the year, the supply of homes for sale has grown. Data from Realtor.com helps put this into context. While there are still fewer homes on the market than in a more normal year like 2019, inventory is still above where it was at this time last year (see graph below):

So, if you’re remembering all that media coverage about record-low supply during the pandemic, you can rest a bit easier. While the market isn’t back to normal just yet, inventory is moving in a healthier direction. And that means as your options improve, you can let go of this now outdated myth because finding a home to buy won’t feel quite so impossible anymore.

So, if you’re remembering all that media coverage about record-low supply during the pandemic, you can rest a bit easier. While the market isn’t back to normal just yet, inventory is moving in a healthier direction. And that means as your options improve, you can let go of this now outdated myth because finding a home to buy won’t feel quite so impossible anymore.

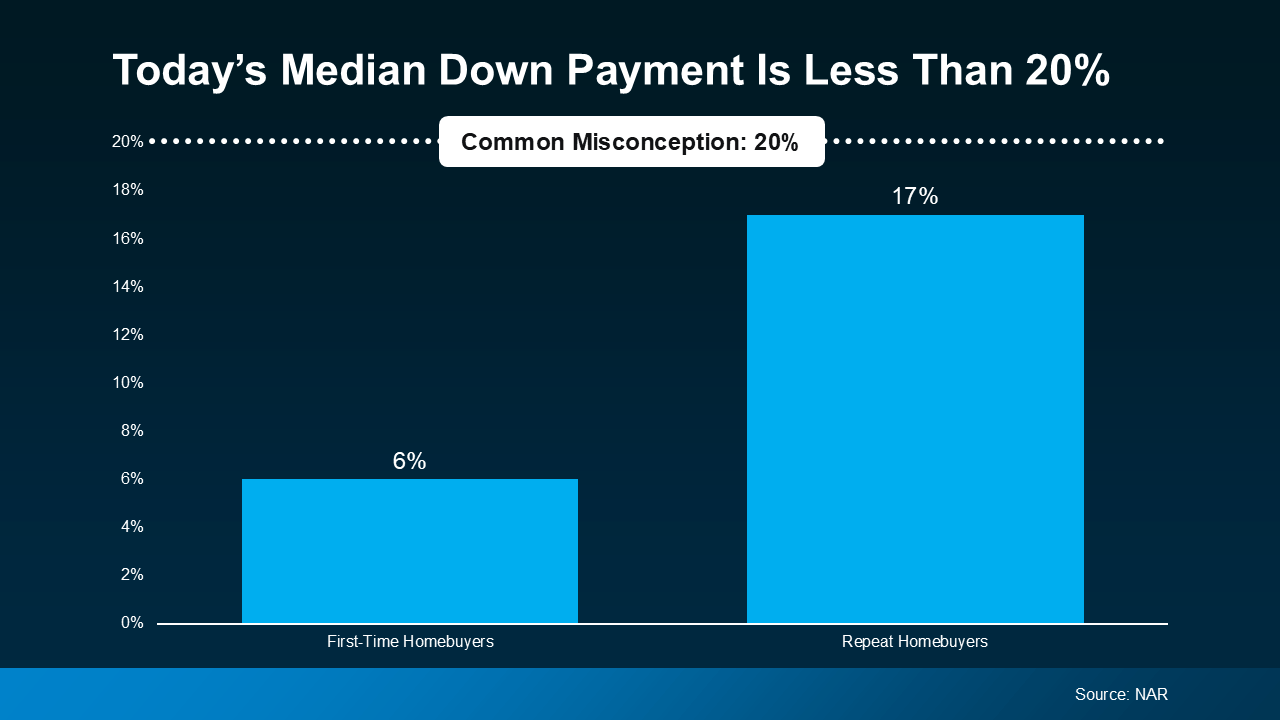

3. I Have To Wait Until I Have Enough for a 20% Down Payment

Many people still believe you need a 20% down payment to buy a home. To show just how widespread this myth is, Fannie Mae says:

“Approximately 90% of consumers overstate or don’t know the minimum required down payment for a typical mortgage.”

And if you look at the data from the National Association of Realtors (NAR), you can see the typical homeowner isn’t putting down as much as you might expect (see graph below):

First-time homebuyers are typically only putting down 6%. That’s far less than the 20% so many people think they need. And if you’re looking at that graph and you’re more focused on how the number for repeat buyers is closer to 20%, here’s what you need to realize. That’s only because they have so much equity built up in their current house that can be used to make a larger down payment for their next move.

This goes to show you don’t have to put 20% down, unless it’s specified by your loan type or lender. Many people put down a lot less. Not to mention, depending on the type of home loan you get, you may only need to put 3.5% or even 0% down. So, if you’re buying your first home, you likely don’t need nearly as much for your down payment as you may think.

An Agent’s Role in Fighting Misconceptions

If you put your move on pause because you heard one or more of these myths yourself, it’s time to talk to a trusted agent. An expert agent has more data and the facts, just like this, to reassure you and help break through any misconceptions that may be holding you back.

Bottom Line

If you have questions about what you’re hearing or reading, let’s connect. You deserve to have someone you can trust to get the facts.

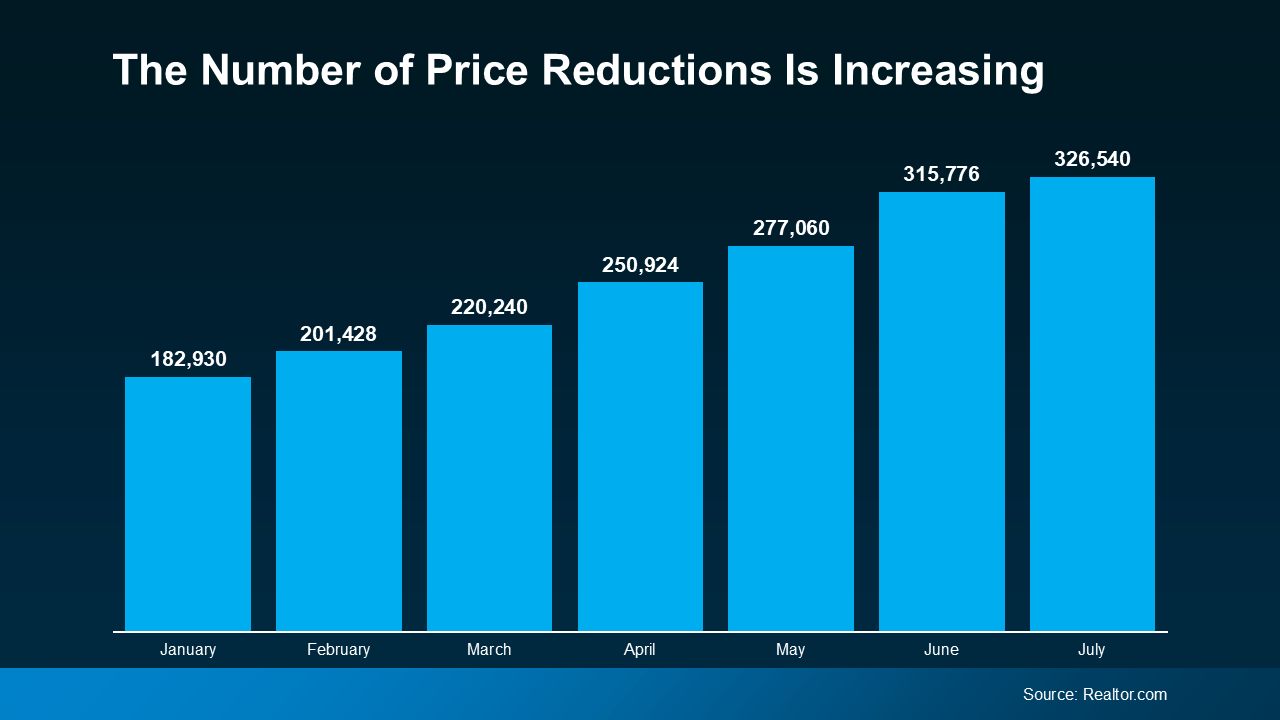

The Number One Mistake Sellers Are Making: Overpricing Their House

The Number One Mistake Sellers Are Making: Overpricing Their House

In today’s housing market, many sellers are making a critical mistake: overpricing their houses. This common error can lead to a home sitting on the market for a long time without any offers. And when that happens, the homeowner may have to drop their asking price to try to re-ignite buyer interest.

Data from Realtor.com shows the number of homeowners realizing this mistake and doing a price reduction is climbing (see graph below):

If you’re thinking about making a move yourself, here’s what you need to know. The best way to avoid making a costly mistake is to work with a trusted real estate agent to find the right price. Here’s a look at what’s at stake if you don’t.

If you’re thinking about making a move yourself, here’s what you need to know. The best way to avoid making a costly mistake is to work with a trusted real estate agent to find the right price. Here’s a look at what’s at stake if you don’t.

Not Paying Attention To Current Market Conditions

Understanding current market conditions is key to accurate pricing. You don’t want to set your asking price based on what happened during the pandemic. The market has moderated a lot since then, so it’s far better to align your price with today’s reality.

Real estate agents stay updated on market trends and how they impact the pricing strategy for your house.

Pricing It Based on What You Want To Make (Not What It’s Worth)

Another misstep is pricing it based on what you want to make on the sale, and not necessarily current market value. You may see other homes in your neighborhood selling for top dollar and assume yours can do the same. But you may not be considering differences in size, condition, and features. For example, maybe that other house is waterfront or has a finished basement. To sum it up, Bankrate explains:

“How do you find that sweet spot of pricing for profit but not overpricing? The expertise of your agent can be truly valuable here. A knowledgeable agent will understand fair market value in your area, how much your house is worth and how much you might reasonably expect to get for it in the current market.”

An agent will do a comparative market analysis (CMA) to make sure your house is compared with truly similar properties to get an accurate look at how it should be priced.

Pricing High to Leave Room for Negotiation

Another common, yet misguided strategy is to price your house high on purpose, so you have more room to negotiate down during the sale. But this can backfire. A price that seems too high often deters potential buyers from even considering the home. So rather than leaving room for negotiation, what you’ll actually be doing is turning buyers away. U.S. News Real Estate explains:

“You want to sell your house for top dollar, but be realistic about the value of the property and how buyers will see it. If you’ve overpriced your home, chances are you’ll eventually need to lower the number, but the peak period of activity that a new listing experiences is already gone.”

An agent can help you set a fair price that attracts buyers and encourages more competitive offers.

Bottom Line

Overpricing your home can have serious consequences. A knowledgeable real estate agent brings an objective perspective, in-depth market knowledge, and a strategic approach to pricing.

Let’s connect so you can avoid making a pricing mistake that’ll cost you.

How To Choose a Great Local Real Estate Agent

How To Choose a Great Local Real Estate Agent

Selecting the right real estate agent can make a world of difference when buying or selling a home. But how do you find the best one? Here are some tips to help you make that big decision as you determine your partner in the process.

Check Their Reputation

Start by gathering information about agents in your area. From there, try to narrow down the list. Ask the people you trust if they have someone they’d recommend. You’ll want to find an agent with a strong online presence, plenty of positive reviews, and someone whose great reputation truly precedes them. As Freddie Mac explains:

“. . . you may want to look for a real estate agent who specializes in the type of home you’re searching for. For example, if you are looking for an energy-efficient home, look for an agent who has experience with finding and negotiating offers for those homes. If you are looking for new construction, you’ll want to find an agent who has experience with new construction and isn’t affiliated with the builder . . .”

Look for Local Market Expertise

A great agent should have in-depth knowledge of what’s happening at the national and local level. That way they can clear up any misconceptions sparked by what you’re reading or hearing in the news. And they can tell you how your area compares to the national data. As an added perk, they’ll also be familiar with the neighborhoods you’re interested in and community amenities. As a recent article from Business Insider says:

“Spend some time talking with prospective agents about the local real estate market and how it could impact your purchase or sale. You want to get an understanding of how knowledgeable they are about local market conditions. Whether they’re helping you sell or buy, their strategy for you should account for those conditions.”

Get a Feel for Their Communication Style and Availability

Effective communication is key in real estate transactions. Choose an agent who listens to your needs, answers your questions quickly, and keeps you informed throughout the process. If an agent is juggling too many clients, they might not be able to give you the attention you deserve. You want someone who will be readily available and responsive. So, what’s the best way to get a feel for their communication style and preferences? Bankrate offers this advice:

“Interviews also give you a chance to find out the agent’s preferred method of communication and their availability. For example, if you’re most comfortable texting and expect to visit homes after work hours during the week, you’ll want an agent who’s happy to do the same.”

Trust Your Gut

Last, rely on your instincts. If you feel like you do or don’t click with one of the agents you’re talking to, that matters. Choose an agent you feel at ease with and who inspires confidence. The right agent should be someone you trust to guide you through one of the most significant transactions of your life. As Business Insider says:

“As long as you’ve properly vetted the agents you’re considering and ensured they have the necessary expertise, it’s ok to go with your gut . . . Maybe you have a better rapport with one of the agents you’re considering, or you just feel like they’re easier to approach. You’re going to be working closely with this person, so it’s important to choose an agent you’re comfortable with.”

Bottom Line

By following these tips, you can pick an agent who’ll provide the support and expertise you need to help make the process as smooth as possible. It’d be an honor to apply for that job. Let’s connect so we can have a conversation and see if we’d be a good fit for working together.

The Great Wealth Transfer: A New Era of Opportunity

The Great Wealth Transfer: A New Era of Opportunity

![]()

In recent years, there’s been a significant shift in how wealth is distributed among generations. It’s called the Great Wealth Transfer.

Historically, the transfer of wealth from one generation to the next was a more gradual process, often limited to smaller amounts of inheritance or family savings. But today, the scale has increased in a big way. As a recent article from Bankrate says:

“The biggest wave of wealth in history is about to pass from Baby Boomers over the next 20 years, and it’s going to have major impacts on many facets of life. Called The Great Wealth Transfer, $84 trillion is poised to move from older Americans to Gen X and millennials. If it’s managed smartly, Americans will be able to grow their wealth and ensure their financial security.”

Basically, as more Baby Boomers retire, sell businesses, or downsize their homes, more substantial assets are being passed down to younger generations. And this creates a powerful ripple effect that’ll continue over the next few decades. The graph below uses data from Merrill and Cerulli Associates to give you an idea of how much inherited money is set to change hands through 2045:

Impact on the Housing Market

One of the most immediate effects of this wealth transfer is on the housing market. Home affordability has been a concern for many aspiring buyers, especially in high-demand areas. The increase in generational wealth is expected to ease some of these challenges by providing future homeowners with greater financial resources. As assets are passed down through generations, buyers may find themselves in a better position to afford homes. Merrill talks about that benefit in a recent article:

“While millennials face steep barriers . . . to buying a first home in many markets, ‘that’s a for-now story, not a forever story’ . . . The Great Wealth Transfer should enable more of them to become homeowners — or trade up or add a second home — either through inherited property or the funds for a down payment.”

Impact on the Economy

But the Great Wealth Transfer doesn’t just impact housing. It’s also going to provide a new avenue for entrepreneurial spirits to fuel economic growth. If someone is looking to start a business and they’re receiving funds like this, that money can used as the necessary capital to start a new company. This helps the next generation of innovators and business owners bring their ideas to life.

Bottom Line

While affordability remains a challenge in today’s housing market, the ongoing Great Wealth Transfer is poised to unlock new opportunities. As wealth is passed down and put to use, it’s expected to ease some of the barriers to homeownership and fuel other entrepreneurial endeavors.

Where Will You Go After You Sell?

Where Will You Go After You Sell?

If you’re planning to sell your house and move, you probably know there’s been a shortage of options available. But here’s the good news: the supply of homes for sale has grown in a lot of markets this year – and that’s not just existing, or previously-owned, homes. It’s true for newly built homes too.

So how do you decide which route to go? Do you buy an existing home or a brand-new one? The choice is yours – you just need to figure out what’s most important to you.

Perks of a Newly Built Home

Here are some benefits of buying a newly built home right now:

- Have brand new everything with never-been-used appliances and materials

- Use energy efficient options to save money and leave a smaller footprint

- Minimize the need for repairs and benefit from builder warranties

- Take advantage of builder concessions that can help with affordability

In today’s market, a lot of builders are focusing on selling their current inventory before they add more homes to their mix. And some of them are offering concessions and are more willing to negotiate to make a sale happen.

That, coupled with the fact builders are primarily building smaller, more affordable homes, has led to one other potential perk. The median price for a newly built home in today’s market is actually lower than the median price of an existing home – which isn’t usually the case. Ralph McLaughlin, Senior Economist at Realtor.com, shares:

“Homebuyers who are looking for that ‘new-home smell’ may be in a relatively friendlier market than times past when new homes were considerably more expensive than used ones.”

If you’re interested in seeing what builders nearby have to offer, lean on your real estate agent. Their knowledge of local builders, new communities, and builder contracts will be important in this process.

Perks of an Existing Home

Now, let’s compare that to the benefits of buying an existing home.

- Join an established neighborhood that you can get a feel for before moving in

- Choose from a wider variety of floorplans and styles

- Appreciate the lived-in charm that only an older home can provide

- Enjoy the privacy and curb appeal of mature trees and landscaping

In addition to these lifestyle benefits, there’s strategic value to buying an existing home, too. Remember, you can always make upgrades to an existing home down the road to give it some of the latest features available. This gives you the best of both worlds: you’ll get the charm, the neighborhood, and over time, you can still add those on-trend elements you may see in a brand-new home. And if you do, you’ll likely increase the home’s value too. An article from LendingTree explains:

“. . . they can personalize it and possibly increase its potential resale value with cosmetic upgrades . . . Plus, if a home comes with physical details or stories that add charm, in some cases, these elements are attractive enough to add to a home’s resale value . . .”

Want to see what’s available? Your real estate agent can show you what homes are for sale in your area, so you can see if there’s one that works for you and your needs.

Bottom Line

There are a lot of factors that go into deciding whether to buy an existing home or a newly built one after you sell, but it’s essential in today’s market to understand the opportunities you can find in both. Let’s connect so you have expert guidance as you explore the options in our area.

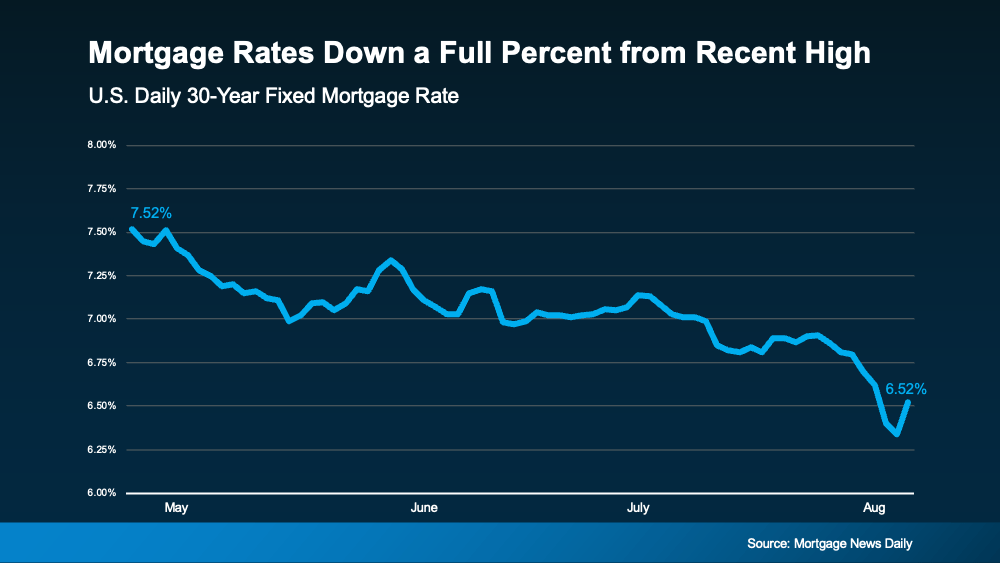

Mortgage Rates Down a Full Percent from Recent High

Mortgage Rates Down a Full Percent from Recent High

Mortgage rates have been one of the hottest topics in the housing market lately because of their impact on affordability. And if you’re someone who’s looking to make a move, you’ve probably been waiting eagerly for rates to come down for that very reason. Well, if the past few weeks are any indication, you may be getting your wish.

Mortgage Rates Trend Down in Recent Weeks

There’s big news for mortgage rates. After the latest reports on the economy, inflation, the unemployment rate, and the Federal Reserve’s recent comments, mortgage rates started dropping a bit. And according to Freddie Mac, they’re now at a level we haven’t seen since February. To help show the downward trend, check out the graph below:

Maybe you’re seeing this and wondering if you should ride the wave and see how low they’ll go. If that’s the case, here’s some important perspective. Remember, the record-low rates from the pandemic are a thing of the past. If you’re holding out hope to see a 3% mortgage rate again, you’re waiting for something experts agree won’t happen. As Greg McBride, Chief Financial Analyst at Bankrate, says:

Maybe you’re seeing this and wondering if you should ride the wave and see how low they’ll go. If that’s the case, here’s some important perspective. Remember, the record-low rates from the pandemic are a thing of the past. If you’re holding out hope to see a 3% mortgage rate again, you’re waiting for something experts agree won’t happen. As Greg McBride, Chief Financial Analyst at Bankrate, says:

“The hopes for lower interest rates need the reality check that ‘lower’ doesn’t mean we’re going back to 3% mortgage rates. . . the best we may be able to hope for over the next year is 5.5 to 6%.”

And with the decrease in recent weeks, you’ve got a big opportunity in front of you right now. It may be enough for you to want to jump back in.

The Relationship Between Rates and Demand

If you wait for mortgage rates to drop further, you might find yourself dealing with more competition as other buyers re-ignite their home searches too.

In the housing market, there’s generally a relationship between mortgage rates and buyer demand. Typically, the higher rates are, the lower buyer demand is. But when rates start to come down, things change. Buyers who were on the fence over higher rates will resume their searches. Here’s what that means for you. As a recent article from Bankrate says:

“If you’re ready to buy, now might be the time to strike. Home prices have been rising primarily because of a longstanding shortage of homes for sale. That’s unlikely to change, and if mortgage rates do fall below 6%, it’s possible buyers would enter the market en masse, further pushing up prices and resurrecting bidding wars.”

Bottom Line

If you’ve been waiting to make your move, the recent downward trend in mortgage rates may be enough to get you off the sidelines. Rates have hit their lowest point in months, and that gives you the opportunity to jump back in before all the other buyers do too.

If you’re ready and able to start the process, reach out and let’s get started.

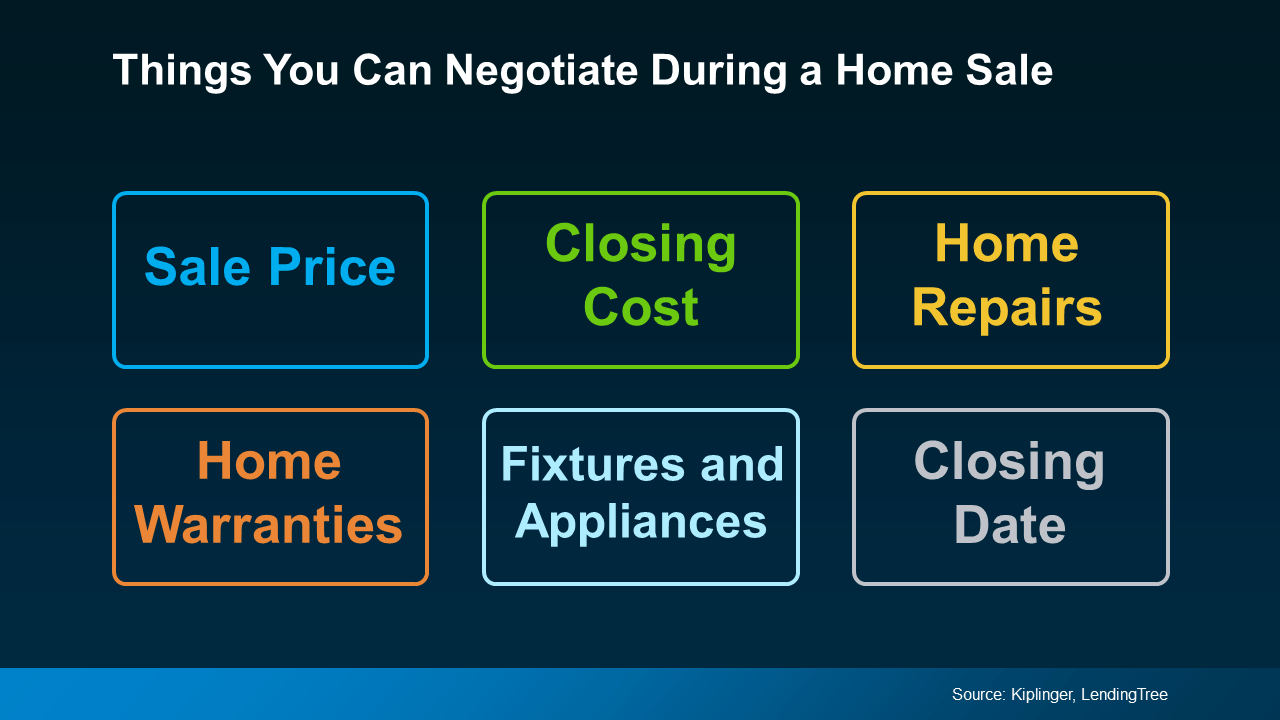

Helpful Negotiation Tactics for Today’s Housing Market

Helpful Negotiation Tactics for Today’s Housing Market

If you haven’t already heard, homebuyers are regaining some negotiating power in today’s market. And while that doesn’t make this a buyer’s market, it does mean buyers may be able to ask for a little more. So, sellers need to be ready for that possibility and know what they’re willing to negotiate.

Whether you’re looking to buy or sell a house, here’s a quick rundown of potential negotiations that may pop up during your transaction. That way, you’re prepared no matter which side of the deal you’re on.

What Can You Negotiate?

Most things in a home purchase are on the negotiation table. Here’s a list of just a few of those options, according to Kiplinger and LendingTree:

- Sale Price: The most obvious is the price of the home. And that lever is being pulled more often today. Buyers don’t want to overpay when affordability is already so tight. And sellers who aren’t realistic about their asking price may have to consider adjusting their price.

- Home Repairs: Based on the inspection, a buyer is within their rights to ask the seller to make reasonable repairs. If the seller doesn’t want to do that, they could offer to reduce the home price or cover some closing costs, so the buyer has the money to take them on themselves.

- Fixtures: Buyers can also ask for appliances or furniture to convey when the house changes hands. Having the seller throw in the washer and dryer cuts down on expenses the buyer would have when moving in. As the seller, you could leave your existing ones behind to sweeten the deal for your buyer, and get yourself new ones for your next place.

- Closing Costs: Closing costs typically run about 2-5% of the home’s purchase price. Buyers can ask the seller to pay for some or all of these expenses to offset the cash the buyer has to bring to the table.

- Home Warranties: Buyers can also ask the seller to pay for a home warranty. This is great for buyers worried about the maintenance costs that may pop up after taking possession of the home. And since this concession usually isn’t terribly expensive for the seller, it can be a good option for both parties.

- Closing Date: Buyers can ask for a faster or extended closing window based on their own timetable. The seller can also advocate for what they need based on their move to find the right compromise.

One thing is true whether you’re a buyer or a seller, and that’s how much your agent can help you throughout the process. Your agent is your go-to for any back-and-forth. They’ll handle the conversations and advocate for your best interests along the way. As Bankrate says:

“Agents have expert negotiating skills. Without one, you must negotiate the terms of the contract on your own.”

They may also be able to uncover what the buyer or seller is looking for in their discussions with the other agent. And that insight can be really valuable at the negotiation table.

Bottom Line

Buyers are regaining a bit of negotiation power in today’s market. Buyers, knowing what levers you can pull will help you feel confident and empowered going into your purchase. Sellers, having a heads up of what they may ask for gives you the chance to think through what you’ll be willing to offer.

Want to chat more about what to expect and the options you have? Let’s connect.

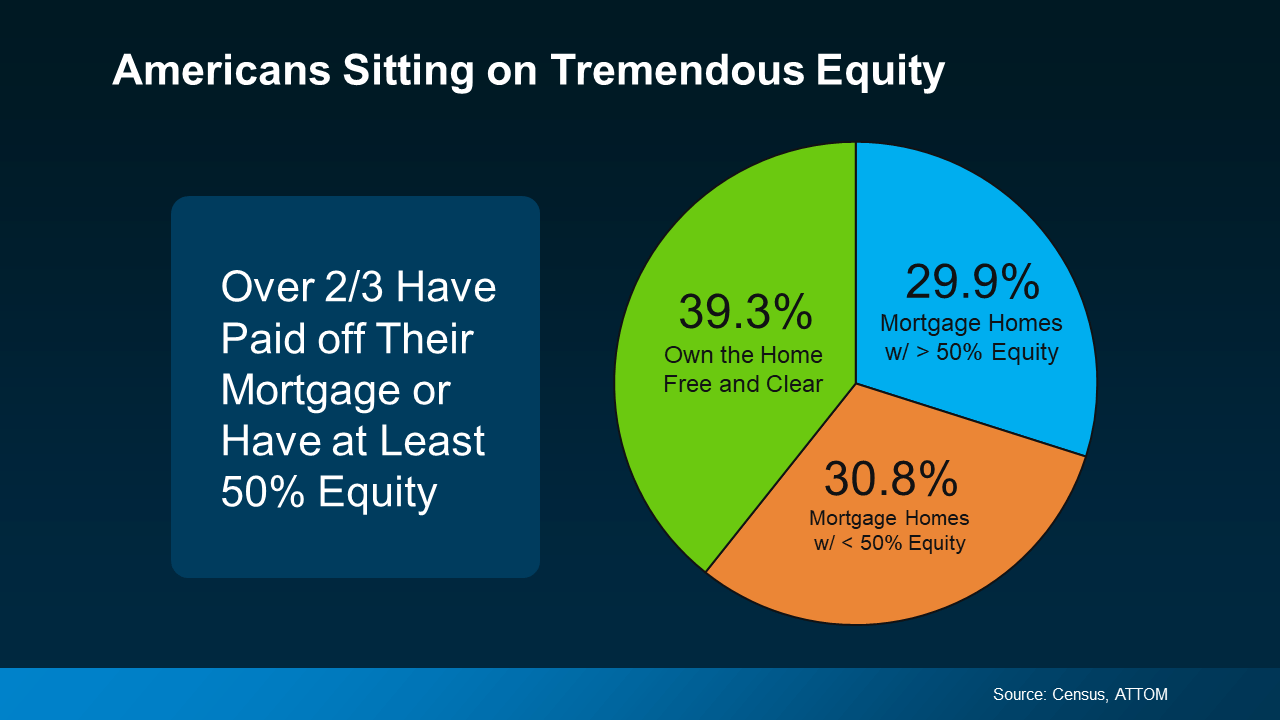

What Every Homeowner Should Know About Their Equity

What Every Homeowner Should Know About Their Equity

Curious about selling your home? Understanding how much equity you have is the first step to unlocking what you can afford when you move. And since home prices rose so much over the past few years, most people have much more equity than they may realize.

Here’s a deeper look at what you need to know if you’re ready to cash in on your investment and put your equity toward your next home.

Home Equity: What Is It and How Much Do You Have?

Home equity is the difference between how much your house is worth and how much you still owe on your mortgage. For example, if your house is worth $400,000 and you only owe $200,000 on your mortgage, your equity would be $200,000.

Recent data from the Census and ATTOM shows Americans have significant equity right now. In fact, more than two out of three homeowners have either completely paid off their mortgages (shown in green in the chart below) or have at least 50% equity in their homes (shown in blue in the chart below):

Today, more homeowners are getting a larger return on their homeownership investments when they sell. And if you have that much equity, it can be a powerful force to fuel your next move.

Today, more homeowners are getting a larger return on their homeownership investments when they sell. And if you have that much equity, it can be a powerful force to fuel your next move.

What You Should Do Next

If you’re thinking about selling your house, it’s important to know how much equity you have, as well as what that means for your home sale and your potential earnings. The best way to get a clear picture is to work with your agent, while also talking to a tax professional or financial advisor. A team of experts can help you understand your specific situation and guide you forward.

Bottom Line

Home prices have gone up, which means your equity probably has too. Let’s connect so you can find out how much you have in your home and move forward confidently when you sell.

Should You Rent Out or Sell Your House?

Should You Rent Out or Sell Your House?

Figuring out what to do with your house when you’re ready to move can be a big decision. Should you sell it and use the money for your next adventure, or keep it as a rental to build long-term wealth?

It’s a question many homeowners face, and the answer isn’t always straightforward. Whether you’re curious about the potential income from renting or worried about the responsibilities of being a landlord, there’s a lot to consider.

Let’s walk through some key questions to ask to help you make the best decision for your situation.

Is Your House a Good Fit for Renting?

Even if you’re interested in becoming a landlord, your current house might not be ideal for renting. Maybe you’re moving far away, so keeping up with the ongoing maintenance would be a hassle, the neighborhood isn’t great for rentals, or the house needs significant repairs before you could rent it out.

If any of this sounds like it might apply, selling might be your best option.

Are You Ready for the Realities of Being a Landlord?

Managing a rental property isn’t just about collecting rent checks. It’s a time-consuming and sometimes challenging job.

For example, you may get calls from tenants at all hours of the day with maintenance requests. Or you may find a tenant causes damage you have to repair before the next lease starts. You may even have to deal with people falling behind on payments or breaking their lease early. Investopedia highlights:

“It isn’t difficult to find horror stories of landlords troubled with more headaches than profits. Before deciding to rent, consider talking to other landlords and doing a detailed cost analysis. You might find that selling your home is a better financial decision and less stressful.”

Do You Have a Good Understanding of What It’ll Cost?

If you’re thinking about renting out your home primarily to generate extra income, remember that there are additional costs you’ll want to plan for. As an article from Bankrate explains:

- Mortgage and Property Taxes: You still need to pay these expenses, even if the rent doesn’t cover all of it.

- Insurance: Landlord insurance costs about 25% more than regular home insurance, and it’s necessary to cover damages and injuries.

- Maintenance and Repairs: Plan to spend at least 1% of the home’s value annually, more if the home is older.

- Finding a Tenant: This involves advertising costs and potentially paying for background checks.

- Vacancies: If the property sits empty between tenants, you’ll lose rental income.

- Management and HOA Fees: A property manager can ease the burden, but typically charges about 10% of the rent. HOA fees are an additional cost too, if applicable.

Bottom Line

To sum it all up, selling or renting out your home is a personal decision that depends on your circumstances. Whatever you decide, taking the time to evaluate your options will help you make the best choice for your future.

Make sure to weigh the pros and cons carefully and consult with professionals so you feel supported and informed as you make your decision. That’s what we’re here for.

The Biggest Mistakes Sellers Are Making Right Now

The Biggest Mistakes Sellers Are Making Right Now

The housing market is going through a transition. Higher mortgage rates are causing more moderate buyer activity at the same time the supply of homes for sale is growing.

And if you aren’t working with an agent, you may not realize that. Here’s the downside. If you’re not informed, you can’t adjust your strategy or expectations to today’s market. And that can lead to a number of costly mistakes.

Here’s a look at some of the most common ones – and how an agent will help you avoid them when you sell.

1. Overpricing Your House

Many sellers set their asking price too high and that’s why there’s an uptick in homes with price reductions today. An unrealistic price will deter potential buyers, cause an appraisal issue, or lead to your house sitting on the market longer. An article from the National Association of Realtors (NAR) explains:

“Some sellers are pricing their homes higher than ever just because they can, but this may drive away serious buyers and result in unapproved appraisals . . .”

To avoid falling into this trap, partner with a pro. An agent uses recent sales of similar homes, the condition of your house, local market trends, and so much more to find the price that’ll attract more buyers and open the door for multiple offers and a faster sale.

2. Skipping the Small Stuff

You may try to skip important repairs, thinking you can pass the task on to your buyer. But visible issues (even if they’re small) can turn off potential buyers and result in lower offers or demands for concessions. As Money Talks News says:

“Home shoppers like to turn on lights, flush toilets and run the water. If these basic things don’t work, they may assume you’ve skipped other maintenance. Homes that appear neglected aren’t likely to fetch top price.”

If you want to get your house ready to sell, the best place to turn to for advice is your agent. They’ll be able to do a walk-through with you and point out anything you’ll need to tackle before the photographer comes in.

3. Not Looking at Things Objectively

Buyers today are feeling the pinch of high home prices and mortgage rates. With affordability that tight, they may come in with an offer that’s lower than you’d want to see – especially if you didn’t stage, price, or market the house well.

It’s important you don’t take this personally. Getting overly emotional can put the sale at risk. As an article from Ramsey Solutions says:

“Remember, a buyer’s offer is not a reflection of their opinion of your home or your housekeeping abilities. . . The sale of your home is strictly a business transaction. If they start out with a low offer, don’t take it personally and get emotional. Instead, channel that energy toward negotiating. Work with your agent and make a counteroffer.”

4. Being Unwilling To Negotiate

The supply of homes for sale has grown. That means buyers have more options, and with that comes more negotiation power. As a seller, you may see more buyers getting an inspection, requesting repairs, or asking for help with closing costs today. You need to be prepared to have those conversations. As U.S. News Real Estate explains:

“If you’ve received an offer for your house that isn’t quite what you’d hoped it would be, expect to negotiate . . . the only way to come to a successful deal is to make sure the buyer also feels like he or she benefits . . . consider offering to cover some of the buyer’s closing costs or agree to a credit for a minor repair the inspector found.”

An agent will walk you through what levers you may want to pull based on your own goals, budget, and timeframe.

5. Not Using a Real Estate Agent

Notice anything? For each of these mistakes, partnering with an agent helps prevent them from happening in the first place. That makes trying to sell your house without an agent’s help the biggest mistake of all.

Real estate agents have experience and expertise in pricing, marketing, negotiating, and more. That knowledge streamlines the selling process and usually results in drumming up more interest and ultimately can get you a higher final price.

Bottom Line

If you want to avoid making mistakes like these, let’s connect to make sure you’re set up for success.

Are Home Prices Going To Come Down?

Are Home Prices Going To Come Down?

Today’s headlines and news stories about home prices are confusing and make it tough to know what’s really happening. Some say home prices are heading for a correction, but what do the facts say? Well, it helps to start by looking at what a correction means.

Here’s what Danielle Hale, Chief Economist at Realtor.com, says:

“In stock market terms, a correction is generally referred to as a 10 to 20% drop in prices . . . We don’t have the same established definitions in the housing market.”

In the context of today’s housing market, it doesn’t mean home prices are going to fall dramatically. It only means prices, which have been increasing rapidly over the last couple years, are normalizing a bit. In other words, they’re now growing at a slower pace. Prices vary a lot by local market, but rest assured, a big drop off isn’t what’s happening at a national level.

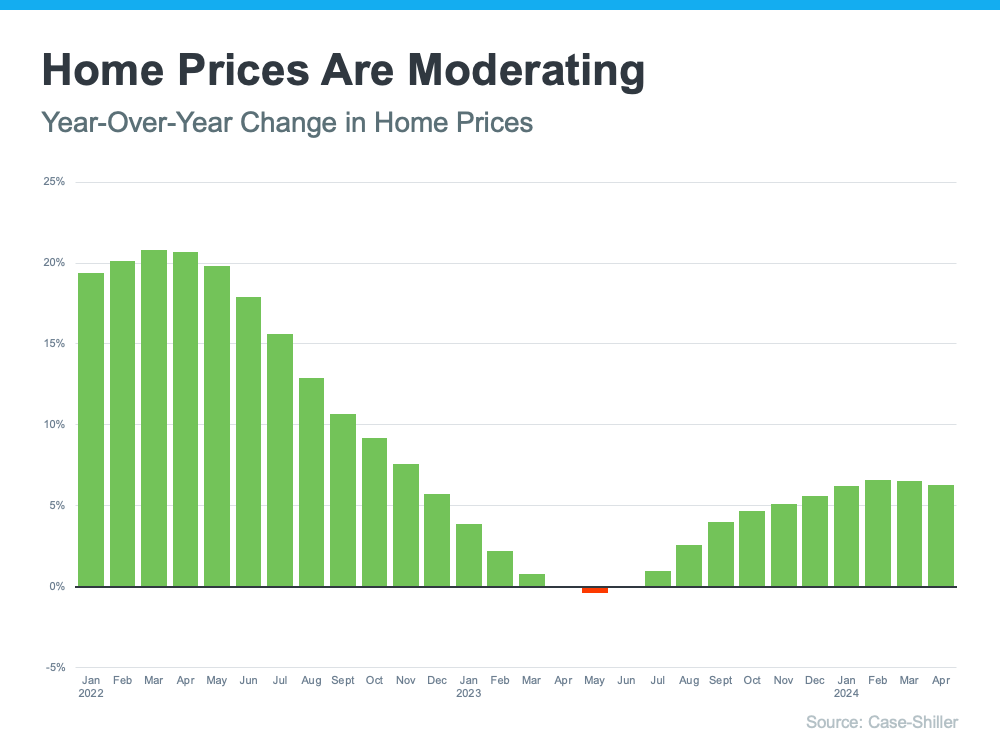

The Real Estate Market Is Normalizing

From 2020 to 2022, home prices skyrocketed. That rapid increase was due to high demand, low interest rates, and a shortage of homes for sale. But, that kind of aggressive growth couldn’t continue forever.

Today, price growth has started to slow down, which is a sign the market is beginning to normalize. The most recent data from Case-Shiller shows that after being basically flat for a couple of months last year, prices are going up at a national level – just not as quickly as before (see graph below):

The big takeaway? So far this year, there’s been a much healthier pace of price growth compared to the pandemic.

The big takeaway? So far this year, there’s been a much healthier pace of price growth compared to the pandemic.

Of course, that’s what’s happening now, but you may be wondering what’s next for prices. Marco Santarelli, the Founder of Norada Real Estate Investments, says:

“Expert forecasts lean towards a moderation in home price growth over the next five years. This translates to a slower and more sustainable pace of appreciation compared to the breakneck speed witnessed in recent years, rather than a freefall in prices.”

It’s all about supply and demand. Increasing inventory plus limited buyer demand, due to relatively high mortgage rates, will continue to ease some of the upward pressure on prices.

What This Means for You

If you’re thinking about buying a home, slowing price growth is welcome news. Skyrocketing home prices during the pandemic left many would-be homebuyers feeling priced-out.

While it’s still a good thing to know the value of the home you buy will likely continue to go up once you own it, slowing price gains are making things feel more manageable. Odeta Kushi, Deputy Chief Economist at First American, says:

“While housing affordability is low for potential first-time home buyers, slowing price appreciation and lower mortgage rates could help — so the dream of homeownership isn’t boarded up just yet.”

Bottom Line

At the national level, home prices are not going down. And most experts forecast they’ll continue growing moderately moving forward. But prices vary a lot by local market. That’s where a trusted real estate agent comes into play. If you have questions about what’s happening with prices in our area, reach out.

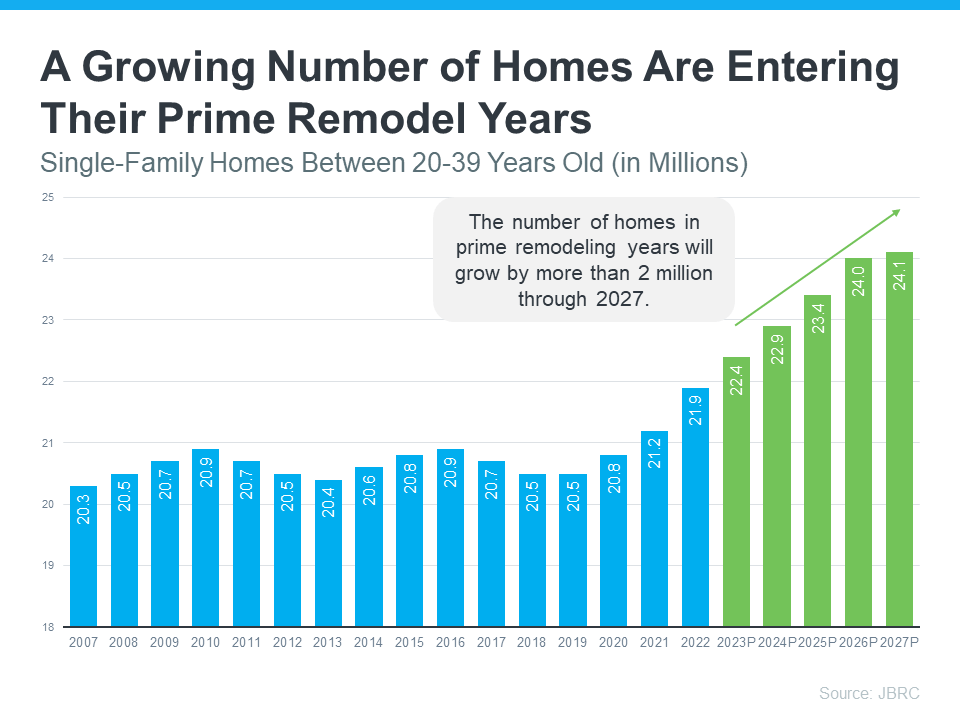

Why Fixing Up Your House Can Help It Sell Faster

Why Fixing Up Your House Can Help It Sell Faster

If you’re thinking about selling your house, you should know there are buyers who are ready and able to pay today’s high prices. But they want a home that’s move-in ready. A recent press release from Redfin explains:

“Buyers are still out there and they’re willing to pay today’s high prices, but only if the house is in really good shape. They don’t want to spend extra money on paint or new appliances.”

It makes sense when you think about it. They’re having to pay a lot of money for a house in today’s market. That means they may not be able to easily afford upgrades after they move in. So, if your home is outdated or needs some work, buyers might pass it by or offer a lower price than you were hoping for.

And there are a lot of homes that need upgrades right now. Millions are entering their prime remodel years, meaning they’re between 20 and 39 years old. Maybe yours is one of them. According to John Burns Research and Consulting (JBRC), the number of homes in their prime remodel years is high and growing (see graph below):

If your house falls into this category, it’s important to consider making selective updates to help it appeal to buyers, so it sells faster. But how do you know where to spend your time and money?

Why You Need a Real Estate Agent

By working with a local real estate agent to be strategic about the improvements you make, you can be sure you’re making a smart investment. Put simply, not all upgrades are worth the cost. As Bankrate says:

“Before you spend money on costly upgrades, be sure the changes you make will have a high return on investment. It doesn’t make sense to install new granite countertops, for example, if you only stand to break even on them, or even lose money.”

And, as that same Bankrate article goes on to say, that’s where a local real estate agent comes in:

“. . . a good real estate agent will know what local buyers expect and can help you decide what needs doing and what doesn’t.”

Your agent will know what buyers in your area are looking for and what they’re willing to pay for it. By working together, you can avoid spending money on upgrades that won’t pay off. Instead, they’ll fill you in on which changes will make your house more appealing and valuable.

Bottom Line

Selling a house right now requires more than just putting up a For Sale sign. You need to make sure it’s in good condition to attract buyers who are willing to pay today’s high prices.

The way to do that is by making smart improvements that will give you the best return on your investment. Let’s work together so you know what buyers are looking for and what your house needs before selling.

Why Moving to a Smaller Home After Retirement Makes Life Easier

Why Moving to a Smaller Home After Retirement Makes Life Easier

Retirement is a time for relaxation, adventure, and enjoying the things you love. As you imagine this exciting new chapter in your life, it’s important to think about whether your current home still fits your needs.

If it’s too big, too costly, or just not convenient anymore, downsizing might help you make the most of your retirement years. To find out if a smaller, more manageable home might be the perfect fit for your new lifestyle, ask yourself these questions:

- Do the original reasons I bought my current house still stand, or have my needs changed since then?

- Do I really need and want the space I have right now, or could somewhere smaller be a better fit?

- What are my housing expenses right now, and how much do I want to try to save by downsizing?

If you answered yes to any of these, consider the benefits that come with downsizing.

The Benefits of Moving into a Smaller Home

There are many reasons why you should downsize. Here are just a few from Bankrate:

Your Equity Can Help Make Downsizing Possible

If those perks sound like something you’d want, you may already have what you need to make it happen. A recent article from Seniors Guide shares:

“And at a time when homeowners age 62 and older have more than $12 trillion in home equity, downsizing makes sense . . .”

If you’ve been in your house for a while, odds are you’re one of those homeowners who’s built up a considerable amount of equity. And that equity is something you can use to help you buy a home that better fits your needs today. Greg McBride, Chief Financial Analyst at Bankrate, explains:

“Downsizing can mean taking that equity when the home is sold and using it to pay cash or make a large down payment on a lower-priced home, reducing your monthly living expenses.”

When you’re ready to use all that equity to fuel your next move, your real estate agent will be your guide through every step of the process. That includes setting the right price for your current house when you sell, finding the home that best fits your evolving needs, and understanding what you can afford at today’s mortgage rate.

Bottom Line

Starting your retirement journey? Think about downsizing – it could really help. When you’re ready, let’s connect.

Why Your Asking Price Matters Even More Right Now

Why Your Asking Price Matters Even More Right Now

If you’re thinking about selling your house, here’s something you really need to know. Even though it’s still a seller’s market today, you can’t pick just any price for your listing.