| Tweet |

What Mortgage Rate Are You Waiting For?

What Mortgage Rate Are You Waiting For?

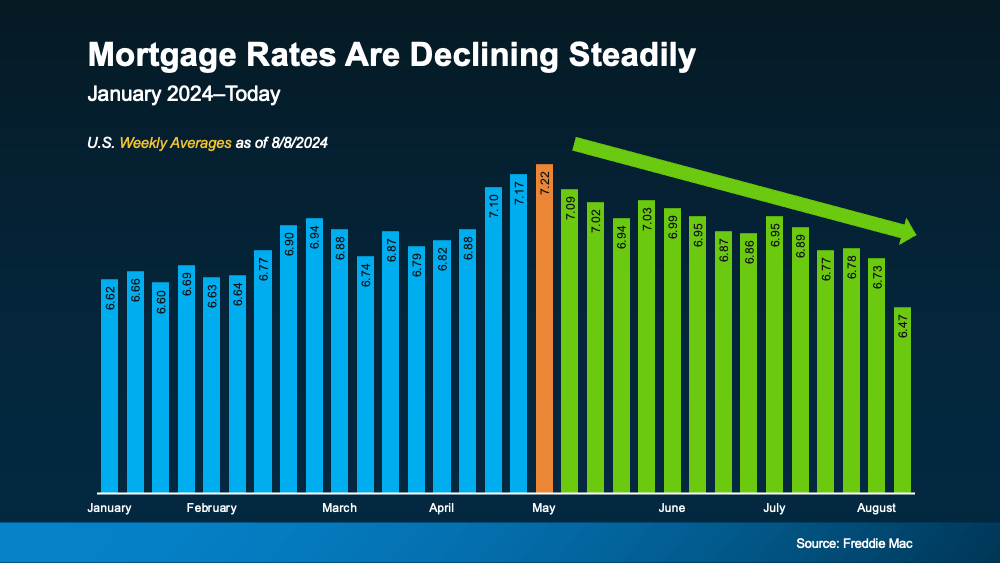

You won’t find anyone who’s going to argue that mortgage rates have had a big impact on housing affordability over the past couple of years. But there is hope on the horizon. Rates have actually started to come down. And, recently they hit the lowest point we’ve seen in 2024, according to Freddie Mac (see graph below):

And if you’re thinking about buying a home, that may leave you wondering: how much lower are they going to go? Here’s some information that can help you know what to expect.

And if you’re thinking about buying a home, that may leave you wondering: how much lower are they going to go? Here’s some information that can help you know what to expect.

Expert Projections for Mortgage Rates

Experts say the overall downward trend should continue as long as inflation and the economy keeps cooling. But as new reports come out on those key indicators, there’s going to be some volatility here and there.

What you need to remember is it’s not wise to let those blips distract you from the larger trend. Rates are still down roughly a full percentage point from the recent peak compared to May.

And the general consensus is that rates in the low 6s are possible in the months ahead, it just depends on what happens with the economy and what the Federal Reserve decides to do moving forward.

Most experts are already starting to revise their 2024 mortgage rate forecasts to be more optimistic that lower rates are ahead. For example, Realtor.com says:

“Mortgage rates have been revised slightly lower as signals from the economy suggest that it will be appropriate for the Fed to begin to cut its Federal Funds rate in 2024. Our yearly mortgage rate average forecast is down to 6.7%, and we revised our year-end forecast to 6.3% from 6.5%.”

Know Your Number for Mortgage Rates

So, what does this mean for you and your plans to move? If you’ve been holding out and waiting for rates to come down, know that it’s already happening. You just have to decide, based on the expert projections and your own budget, when you’ll be willing to jump back in. As Sam Khater, Chief Economist at Freddie Mac, says:

“The decline in mortgage rates does increase prospective homebuyers’ purchasing power and should begin to pique their interest in making a move.”

As a next step, ask yourself this: what number do I want to see rates hit before I’m ready to move?

Maybe it’s 6.25%. Maybe it’s 6.0%. Or maybe it’s once they hit 5.99%. The exact percentage where you feel comfortable kicking off your search again is personal. Once you have that number in mind, you don’t need to follow rates yourself and wait for it to become a reality.

Instead, connect with a local real estate professional. They’ll help you stay up to date on what’s happening and have a conversation about when to make your move. And once rates hit your target, they’ll be the first to let you know.

Bottom Line

If you’ve put your moving plans on hold because of higher mortgage rates, think about the number you want to see rates hit that would make you re-enter the market.

Once you have that number in mind, let’s connect so you have someone on your side to let you know when we get there.

Today’s Biggest Housing Market Myths

Today’s Biggest Housing Market Myths

Have you ever heard the phrase: don’t believe everything you hear? That’s especially true if you’re thinking about buying or selling a home in today’s housing market. There’s a lot of misinformation out there. And right now, making sure you have someone you can go to for trustworthy information is extra important.

If you partner with a real estate agent, they can clear up some common misconceptions and reassure you by backing them up with research-driven facts. Here are just a few misconceptions they can help disprove.

1. I’ll Get a Better Deal Once Prices Crash

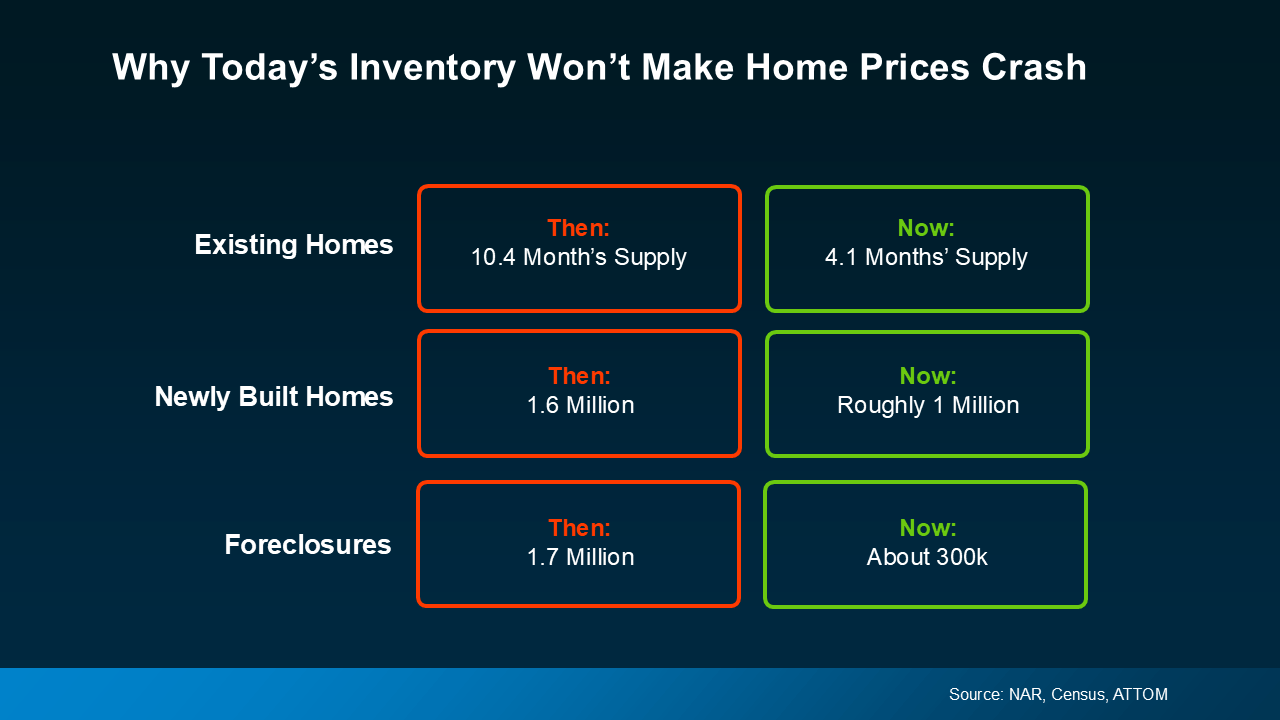

If you’ve heard home prices are going to come crashing down, it’s time to look at what’s actually happening. While prices vary by local market, there’s a lot of data out there from numerous sources that shows a crash is not going to happen. Back in 2008, there was a dramatic oversupply of homes that led to prices crashing. Across the board, there’s an undersupply of homes for sale today. That makes this market a whole different scenario (see chart below):

So, if you think waiting will score you a deal, know that data shows there’s not a crash on the horizon, and waiting isn’t going to pay off the way you’d hoped.

So, if you think waiting will score you a deal, know that data shows there’s not a crash on the horizon, and waiting isn’t going to pay off the way you’d hoped.

2. I Won’t Be Able To Find Anything To Buy

If this nagging fear about finding the right home if you move is still holding you back, you probably haven’t talked with an expert real estate agent lately. Throughout the year, the supply of homes for sale has grown. Data from Realtor.com helps put this into context. While there are still fewer homes on the market than in a more normal year like 2019, inventory is still above where it was at this time last year (see graph below):

So, if you’re remembering all that media coverage about record-low supply during the pandemic, you can rest a bit easier. While the market isn’t back to normal just yet, inventory is moving in a healthier direction. And that means as your options improve, you can let go of this now outdated myth because finding a home to buy won’t feel quite so impossible anymore.

So, if you’re remembering all that media coverage about record-low supply during the pandemic, you can rest a bit easier. While the market isn’t back to normal just yet, inventory is moving in a healthier direction. And that means as your options improve, you can let go of this now outdated myth because finding a home to buy won’t feel quite so impossible anymore.

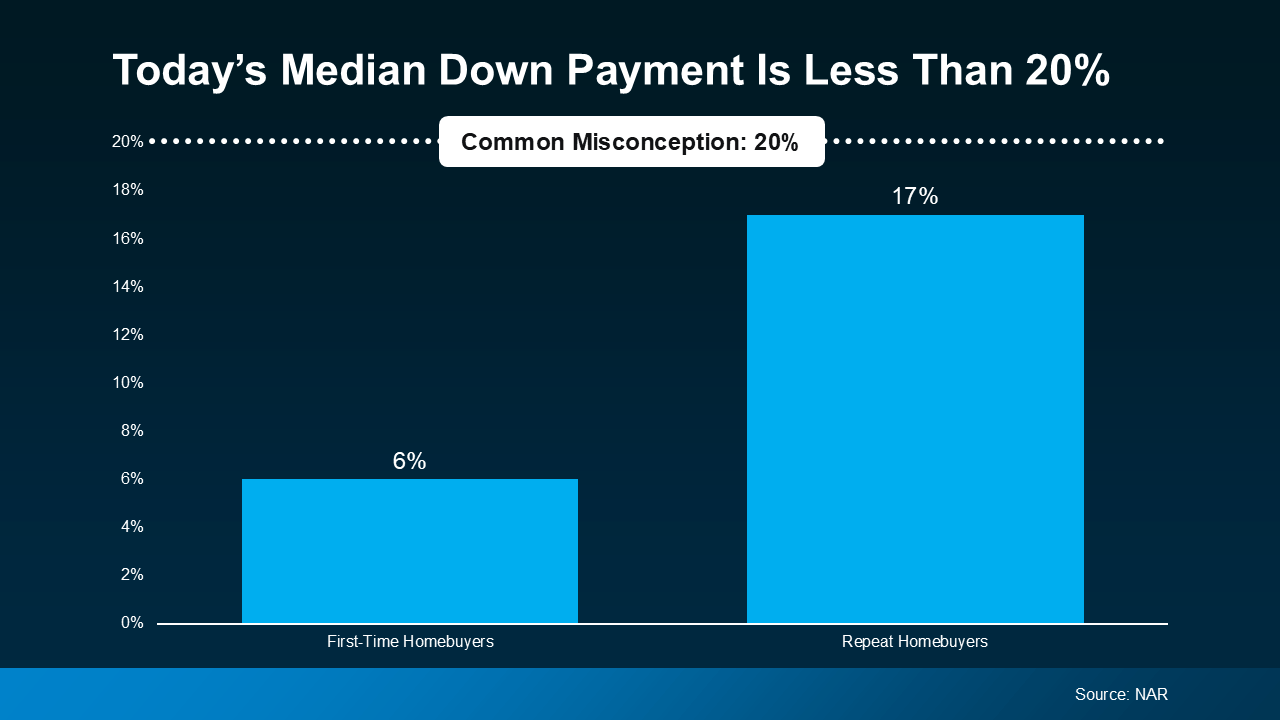

3. I Have To Wait Until I Have Enough for a 20% Down Payment

Many people still believe you need a 20% down payment to buy a home. To show just how widespread this myth is, Fannie Mae says:

“Approximately 90% of consumers overstate or don’t know the minimum required down payment for a typical mortgage.”

And if you look at the data from the National Association of Realtors (NAR), you can see the typical homeowner isn’t putting down as much as you might expect (see graph below):

First-time homebuyers are typically only putting down 6%. That’s far less than the 20% so many people think they need. And if you’re looking at that graph and you’re more focused on how the number for repeat buyers is closer to 20%, here’s what you need to realize. That’s only because they have so much equity built up in their current house that can be used to make a larger down payment for their next move.

This goes to show you don’t have to put 20% down, unless it’s specified by your loan type or lender. Many people put down a lot less. Not to mention, depending on the type of home loan you get, you may only need to put 3.5% or even 0% down. So, if you’re buying your first home, you likely don’t need nearly as much for your down payment as you may think.

An Agent’s Role in Fighting Misconceptions

If you put your move on pause because you heard one or more of these myths yourself, it’s time to talk to a trusted agent. An expert agent has more data and the facts, just like this, to reassure you and help break through any misconceptions that may be holding you back.

Bottom Line

If you have questions about what you’re hearing or reading, let’s connect. You deserve to have someone you can trust to get the facts.

How To Choose a Great Local Real Estate Agent

How To Choose a Great Local Real Estate Agent

Selecting the right real estate agent can make a world of difference when buying or selling a home. But how do you find the best one? Here are some tips to help you make that big decision as you determine your partner in the process.

Check Their Reputation

Start by gathering information about agents in your area. From there, try to narrow down the list. Ask the people you trust if they have someone they’d recommend. You’ll want to find an agent with a strong online presence, plenty of positive reviews, and someone whose great reputation truly precedes them. As Freddie Mac explains:

“. . . you may want to look for a real estate agent who specializes in the type of home you’re searching for. For example, if you are looking for an energy-efficient home, look for an agent who has experience with finding and negotiating offers for those homes. If you are looking for new construction, you’ll want to find an agent who has experience with new construction and isn’t affiliated with the builder . . .”

Look for Local Market Expertise

A great agent should have in-depth knowledge of what’s happening at the national and local level. That way they can clear up any misconceptions sparked by what you’re reading or hearing in the news. And they can tell you how your area compares to the national data. As an added perk, they’ll also be familiar with the neighborhoods you’re interested in and community amenities. As a recent article from Business Insider says:

“Spend some time talking with prospective agents about the local real estate market and how it could impact your purchase or sale. You want to get an understanding of how knowledgeable they are about local market conditions. Whether they’re helping you sell or buy, their strategy for you should account for those conditions.”

Get a Feel for Their Communication Style and Availability

Effective communication is key in real estate transactions. Choose an agent who listens to your needs, answers your questions quickly, and keeps you informed throughout the process. If an agent is juggling too many clients, they might not be able to give you the attention you deserve. You want someone who will be readily available and responsive. So, what’s the best way to get a feel for their communication style and preferences? Bankrate offers this advice:

“Interviews also give you a chance to find out the agent’s preferred method of communication and their availability. For example, if you’re most comfortable texting and expect to visit homes after work hours during the week, you’ll want an agent who’s happy to do the same.”

Trust Your Gut

Last, rely on your instincts. If you feel like you do or don’t click with one of the agents you’re talking to, that matters. Choose an agent you feel at ease with and who inspires confidence. The right agent should be someone you trust to guide you through one of the most significant transactions of your life. As Business Insider says:

“As long as you’ve properly vetted the agents you’re considering and ensured they have the necessary expertise, it’s ok to go with your gut . . . Maybe you have a better rapport with one of the agents you’re considering, or you just feel like they’re easier to approach. You’re going to be working closely with this person, so it’s important to choose an agent you’re comfortable with.”

Bottom Line

By following these tips, you can pick an agent who’ll provide the support and expertise you need to help make the process as smooth as possible. It’d be an honor to apply for that job. Let’s connect so we can have a conversation and see if we’d be a good fit for working together.

How Mortgage Rate Changes Impact Your Homebuying Power

How Mortgage Rate Changes Impact Your Homebuying Power

If you’re thinking about buying or selling a home, you’ve probably got mortgage rates on your mind. That’s because you’ve likely heard that mortgage rates impact how much you can afford in your monthly mortgage payment, and you want to factor that into your planning. Here’s what you need to know.

What’s Happening with Mortgage Rates?

Mortgage rates have been trending down recently. While that’s good news for your homebuying plans, it’s important to know that rates can be unpredictable because they’re affected by many factors.

Things like the economy, job market, inflation, and decisions made by the Federal Reserve all play a part. So, even as rates go down, they can still bounce around a bit based on new economic data. As Odeta Kushi, Deputy Chief Economist at First American, says:

“The ongoing deceleration in inflation, coupled with the Federal Reserve’s recent indication of potential rate cuts [in 2024], suggests an environment supportive of modest declines in mortgage rates. Barring any unforeseen circumstances and resurgence in inflation, lower mortgage rates could be on the horizon, but the journey towards them might be slow and bumpy.”

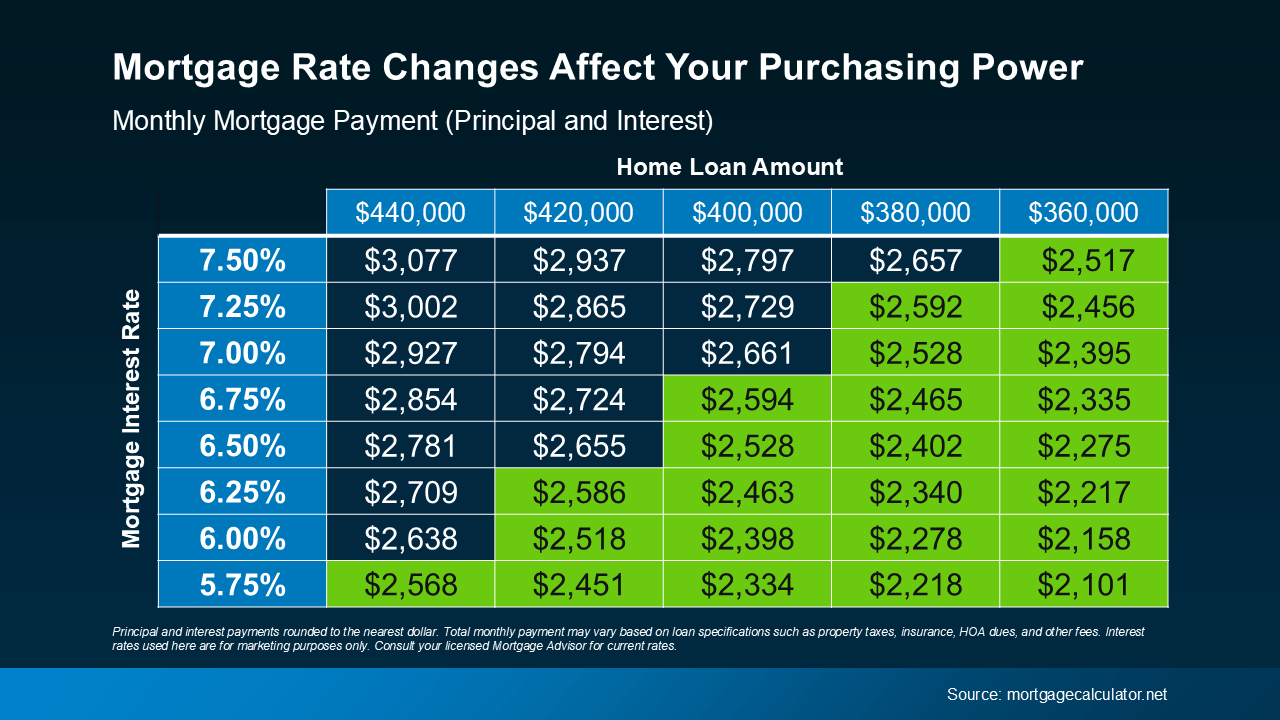

How Do These Changes Affect You?

When mortgage rates change, it affects how much you pay each month for your home loan. Even a small rate change can make a big difference to your monthly bill.

Take a look at the chart below to see how different mortgage rates impact your house payment each month for various loan amounts. Imagine you can afford a monthly payment of $2,600 for your home loan. The green part in the chart shows payments in that range or lower based on varying mortgage rates (see chart below):

Understanding how mortgage rates impact your payment helps you make better decisions.

Understanding how mortgage rates impact your payment helps you make better decisions.

How Can You Keep Track of the Latest on Rates?

Real estate agents have the expertise to help you understand what’s happening and what it means for you. They can provide tools and visuals, like the chart above, to show how rate changes impact your buying power.

You don’t need to be a mortgage expert; you just need a professional by your side. Someone who can help you make sense of the market and guide you through your homebuying or selling journey.

Bottom Line

If you have questions about the housing market, let’s connect. That way you’ll understand what’s going on and how to navigate it.

What Credit Score Do You Really Need To Buy a House?

What Credit Score Do You Really Need To Buy a House?

When you’re thinking about buying a home, your credit score is one of the biggest pieces of the puzzle. Think of it like your financial report card that lenders look at when trying to figure out if you qualify, and which home loan will work best for you. As the Mortgage Report says:

“Good credit scores communicate to lenders that you have a track record for properly managing your debts. For this reason, the higher your score, the better your chances of qualifying for a mortgage.”

The trouble is most buyers overestimate the minimum credit score they need to buy a home. According to a report from Fannie Mae, only 32% of consumers have a good idea of what lenders require. That means nearly 2 out of every 3 people don’t.

So, here’s a general ballpark to give you a rough idea. Experian says:

“The minimum credit score needed to buy a house can range from 500 to 700, but will ultimately depend on the type of mortgage loan you’re applying for and your lender. Most lenders require a minimum credit score of 620 to buy a house with a conventional mortgage.”

Basically, it varies. So, even if your credit isn’t perfect, there are still options out there. FICO explains:

“While many lenders use credit scores like FICO Scores to help them make lending decisions, each lender has its own strategy, including the level of risk it finds acceptable. There is no single “cutoff score” used by all lenders, and there are many additional factors that lenders may use . . .”

And if your credit score needs a little TLC, don’t worry—Experian says there are some easy steps you can take to give it a boost, including:

1. Pay Your Bills on Time

Lenders want to see that you can reliably pay your bills on time. This includes everything from credit cards to utilities and cell phone bills. Consistent, on-time payments show you’re a responsible borrower.

2. Pay Off Outstanding Debt

Paying down what you owe can help lower your overall debt and make you less of a risk to lenders. Plus, it improves your credit utilization ratio (how much credit you’re using compared to your total limit). A lower ratio means you’re more reliable to lenders.

3. Don’t Apply for Too Much Credit

While it might be tempting to open more credit cards to build your score, it’s best to hold off. Too many new credit applications can lead to hard inquiries on your report, which can temporarily lower your score.

Bottom Line

Your credit score is crucial when buying a home. Even if your score isn’t perfect, there are still pathways to homeownership.

Working with a trusted lender is the best way to get more information on how your credit score could factor into your home loan.

The Great Wealth Transfer: A New Era of Opportunity

The Great Wealth Transfer: A New Era of Opportunity

![]()

In recent years, there’s been a significant shift in how wealth is distributed among generations. It’s called the Great Wealth Transfer.

Historically, the transfer of wealth from one generation to the next was a more gradual process, often limited to smaller amounts of inheritance or family savings. But today, the scale has increased in a big way. As a recent article from Bankrate says:

“The biggest wave of wealth in history is about to pass from Baby Boomers over the next 20 years, and it’s going to have major impacts on many facets of life. Called The Great Wealth Transfer, $84 trillion is poised to move from older Americans to Gen X and millennials. If it’s managed smartly, Americans will be able to grow their wealth and ensure their financial security.”

Basically, as more Baby Boomers retire, sell businesses, or downsize their homes, more substantial assets are being passed down to younger generations. And this creates a powerful ripple effect that’ll continue over the next few decades. The graph below uses data from Merrill and Cerulli Associates to give you an idea of how much inherited money is set to change hands through 2045:

Impact on the Housing Market

Impact on the Housing Market

One of the most immediate effects of this wealth transfer is on the housing market. Home affordability has been a concern for many aspiring buyers, especially in high-demand areas. The increase in generational wealth is expected to ease some of these challenges by providing future homeowners with greater financial resources. As assets are passed down through generations, buyers may find themselves in a better position to afford homes. Merrill talks about that benefit in a recent article:

“While millennials face steep barriers . . . to buying a first home in many markets, ‘that’s a for-now story, not a forever story’ . . . The Great Wealth Transfer should enable more of them to become homeowners — or trade up or add a second home — either through inherited property or the funds for a down payment.”

Impact on the Economy

But the Great Wealth Transfer doesn’t just impact housing. It’s also going to provide a new avenue for entrepreneurial spirits to fuel economic growth. If someone is looking to start a business and they’re receiving funds like this, that money can used as the necessary capital to start a new company. This helps the next generation of innovators and business owners bring their ideas to life.

Bottom Line

While affordability remains a challenge in today’s housing market, the ongoing Great Wealth Transfer is poised to unlock new opportunities. As wealth is passed down and put to use, it’s expected to ease some of the barriers to homeownership and fuel other entrepreneurial endeavors.

Is Affordability Starting To Improve?

Is Affordability Starting To Improve?

Over the past couple of years, a lot of people have had a hard time buying a home. And while affordability is still tight, there are signs it’s getting a little better and might keep improving throughout the rest of the year. Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), says:

“Housing affordability is improving ever so modestly, but it is moving in the right direction.”

Here’s a look at the latest data on the three biggest factors affecting home affordability: mortgage rates, home prices, and wages.

1. Mortgage Rates

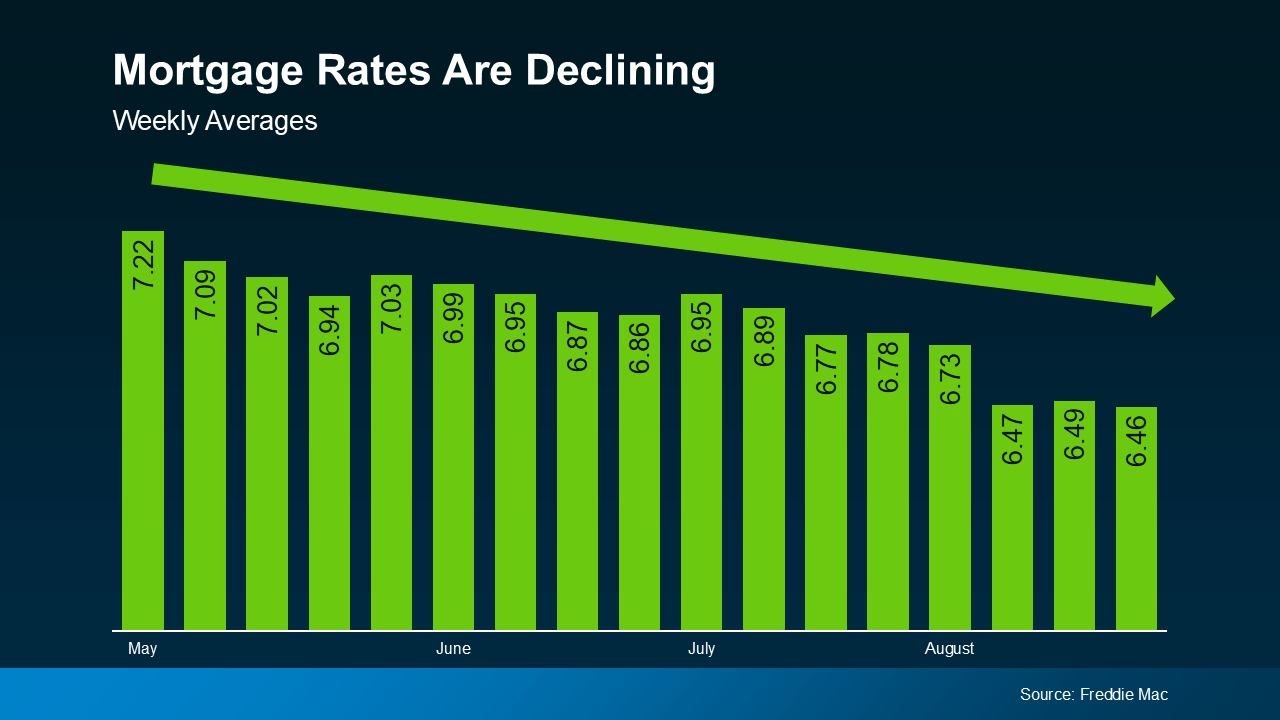

Mortgage rates have been volatile this year, bouncing around from the mid-6% to low 7% range. But there’s some good news. Data from Freddie Mac shows rates have been trending down overall since May (see graph below):

Mortgage rates have improved lately in part because of recent economic, employment, and inflation data. Moving forward, some rate volatility is to be expected. But if future economic data continues to show signs of cooling, experts say mortgage rates could keep going down.

Mortgage rates have improved lately in part because of recent economic, employment, and inflation data. Moving forward, some rate volatility is to be expected. But if future economic data continues to show signs of cooling, experts say mortgage rates could keep going down.

Even a small drop can help you out. When rates decline, it’s easier to afford the home you want because your monthly payment will be lower. Just don’t expect them to go back down to 3%.

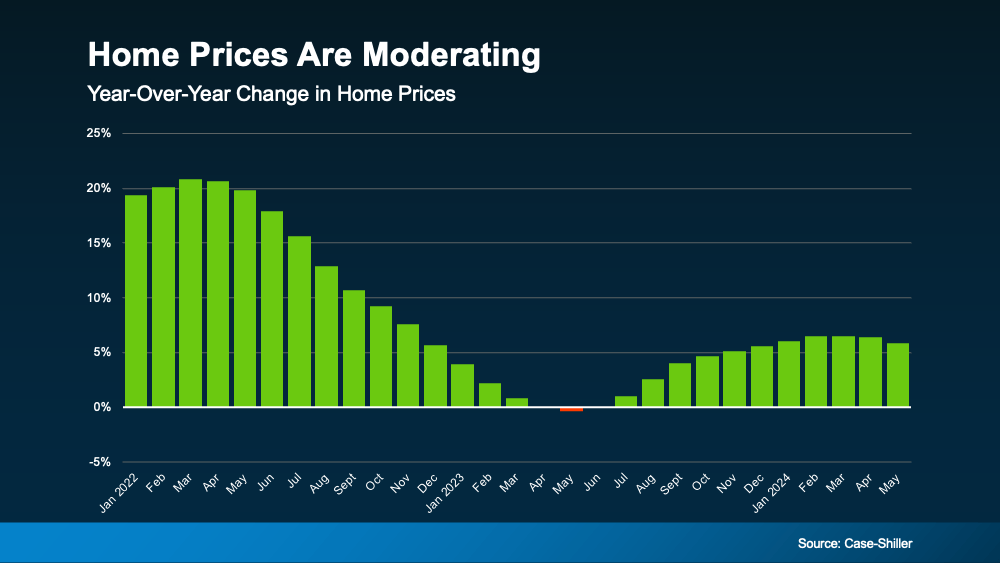

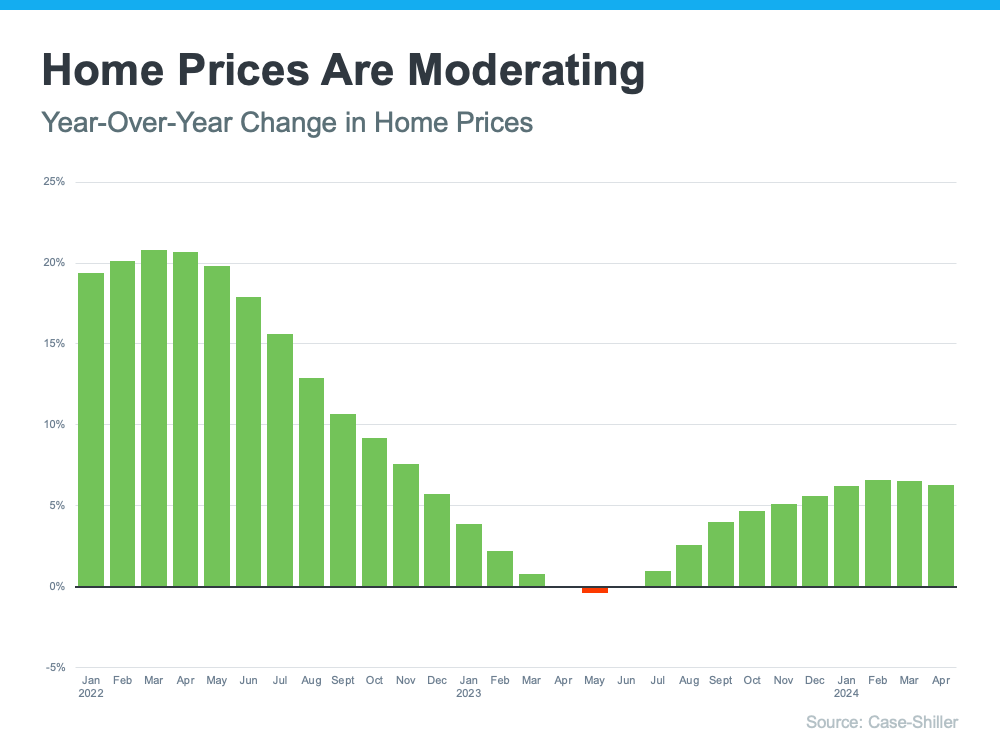

2. Home Prices

The second big thing to think about is home prices. Nationally, they’re still going up this year, but not as fast as they did a couple of years ago. The graph below uses home price data from Case-Shiller to illustrate that point:

If you’re thinking about buying a home, slower price growth is good news. Home prices went up a lot during the pandemic, making it hard for many people to buy. Now, with prices rising more slowly, buying a home may feel less out of reach. As Odeta Kushi, Deputy Chief Economist at First American, says:

If you’re thinking about buying a home, slower price growth is good news. Home prices went up a lot during the pandemic, making it hard for many people to buy. Now, with prices rising more slowly, buying a home may feel less out of reach. As Odeta Kushi, Deputy Chief Economist at First American, says:

“While housing affordability is low for potential first-time home buyers, slowing price appreciation and lower mortgage rates could help – so the dream of homeownership isn’t boarded up just yet.”

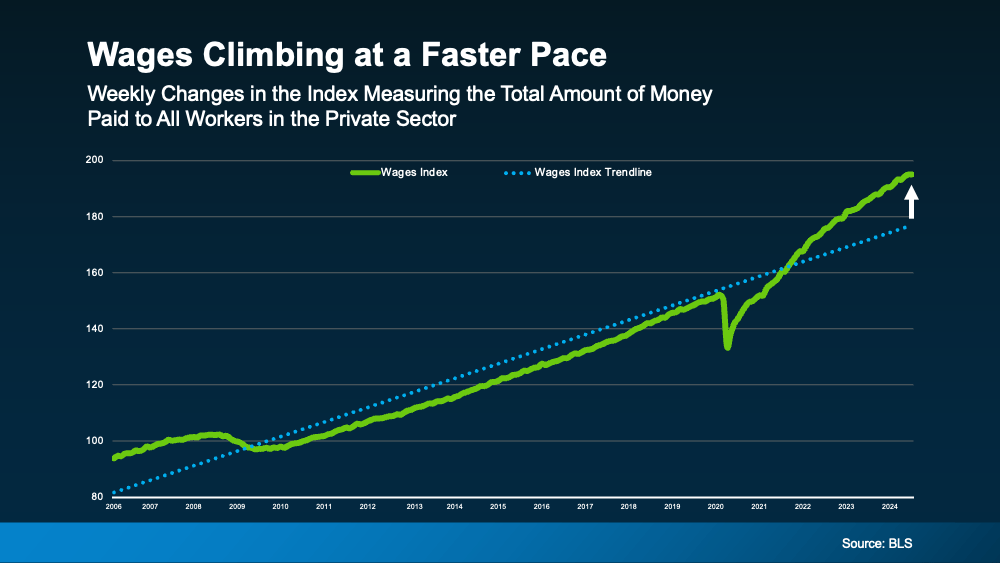

3. Wages

Another factor helping with affordability is rising wages. The graph below uses data from the Bureau of Labor Statistics (BLS) to show how wages have increased over time:

Look at the blue dotted line. It shows how wages usually go up in a typical year. On the right side of the graph, you’ll see wages are rising even faster than normal right now – that’s the green line.

Look at the blue dotted line. It shows how wages usually go up in a typical year. On the right side of the graph, you’ll see wages are rising even faster than normal right now – that’s the green line.

This helps you because if your income increases, it’s easier to afford a home. That’s because you won’t have to spend as much of your paycheck on your monthly mortgage payment.

Bottom Line

When you put all these factors together, you see mortgage rates are trending down, home prices are rising more slowly, and wages are going up faster than usual. Though affordability is still a challenge, these trends are early signs things might be starting to improve.

Are There More Homes for Sale Where You Live?

Are There More Homes for Sale Where You Live?

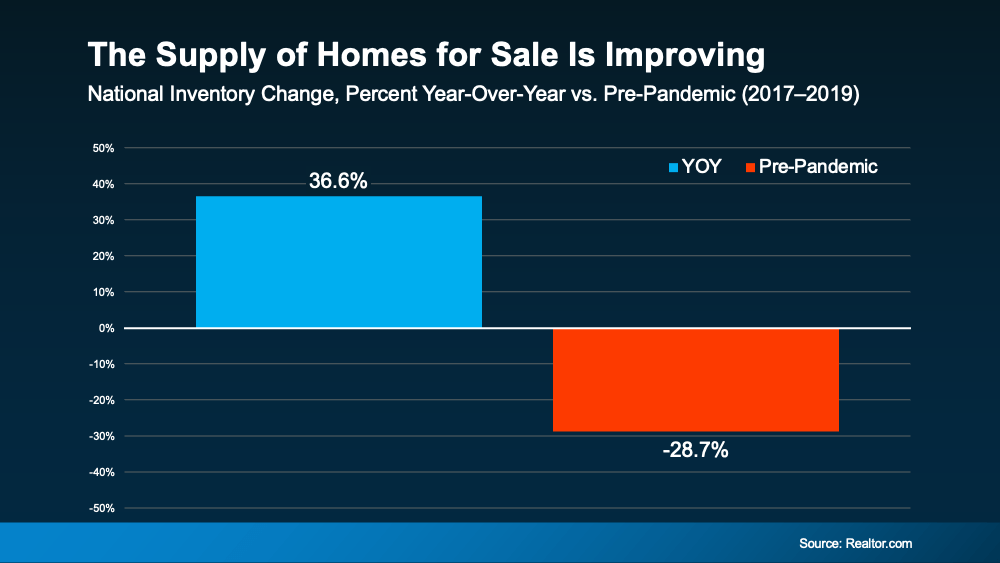

One of the biggest bright spots in today’s housing market is how much the supply of homes for sale has grown since the beginning of this year.

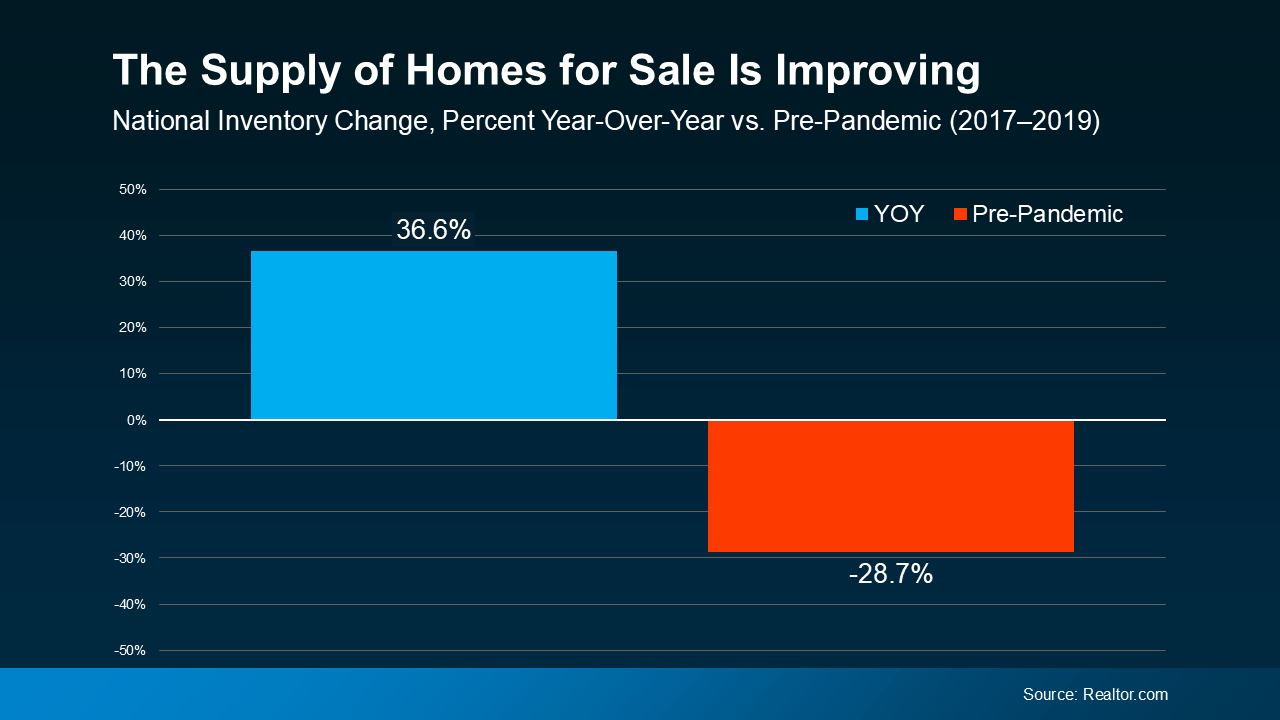

Recent data from Realtor.com shows that nationally, there are 36.6% more homes actively for sale now compared to the same time last year. That’s a significant improvement. It gives you far more options for your move than you would’ve had just a year ago. And with supply improving, you’re also regaining a bit of negotiation power. So, if you’re someone who thought about buying a home over the last few years but was discouraged by how limited inventory was, this should be welcome news.

As Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), says:

“Increased housing supply spells good news for consumers who want to see more properties before making purchasing decisions.”

But just so you have perspective, even though inventory has grown, that doesn’t mean we’ve suddenly flipped to an oversupply of homes on the market. There are nowhere near enough homes for sale to make prices crash. If you compare today’s inventory levels to more normal, pre-pandemic numbers (2017–2019), there are still roughly 29% fewer homes actively for sale now (see graph below):

So, while we’re up by almost 37% year-over-year, we’re still not back to how much inventory there’d be in a normal market.

So, while we’re up by almost 37% year-over-year, we’re still not back to how much inventory there’d be in a normal market.

As Bill McBride, Housing Analyst for Calculated Risk, explains:

“ . . . currently inventory is increasing year-over-year but is still well below pre-pandemic levels.”

But that’s okay. It’s to be expected. As a country, it’ll take a while to get back to the typical level of homes for sale. And the good news for buyers is, in some select markets, it’s closer to being a reality.

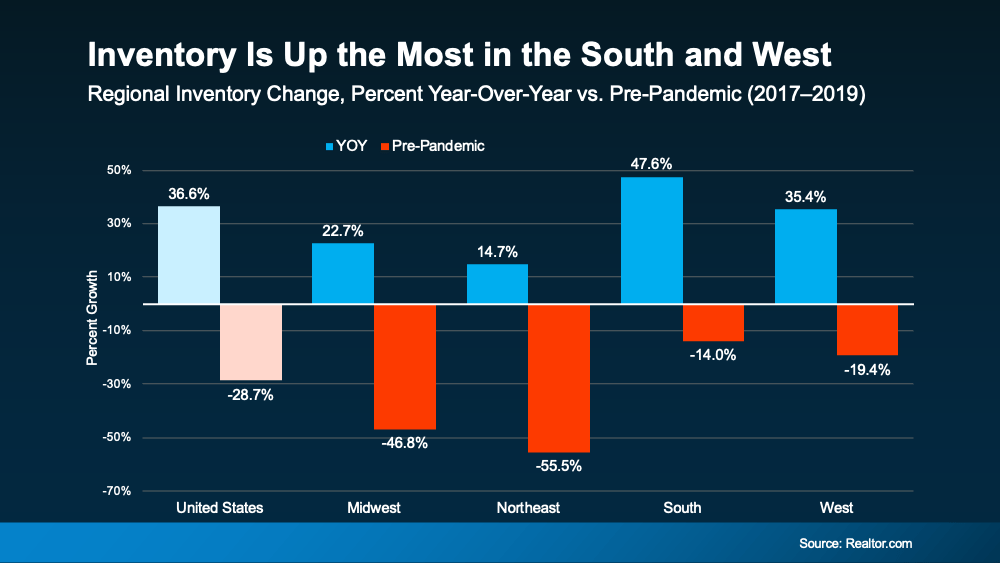

Here’s a rundown of what today’s inventory growth looks like by region (see graph below):

Real estate will always be hyper-local. If you want to find out what inventory numbers look like where you live, reach out to a local agent. They’ll be able to tell you what they’re seeing and how it stacks up to the national market. You may find you have even more opportunity to move where you are.

Real estate will always be hyper-local. If you want to find out what inventory numbers look like where you live, reach out to a local agent. They’ll be able to tell you what they’re seeing and how it stacks up to the national market. You may find you have even more opportunity to move where you are.

Bottom Line

The supply of homes across the country is improving in a big way. As a buyer, that gives you more options for your home search, and ultimately, a better chance of finding what you like.

So, what are you looking for in a home? And what’s your budget? Let’s go over that together to find the options that may be right for you.

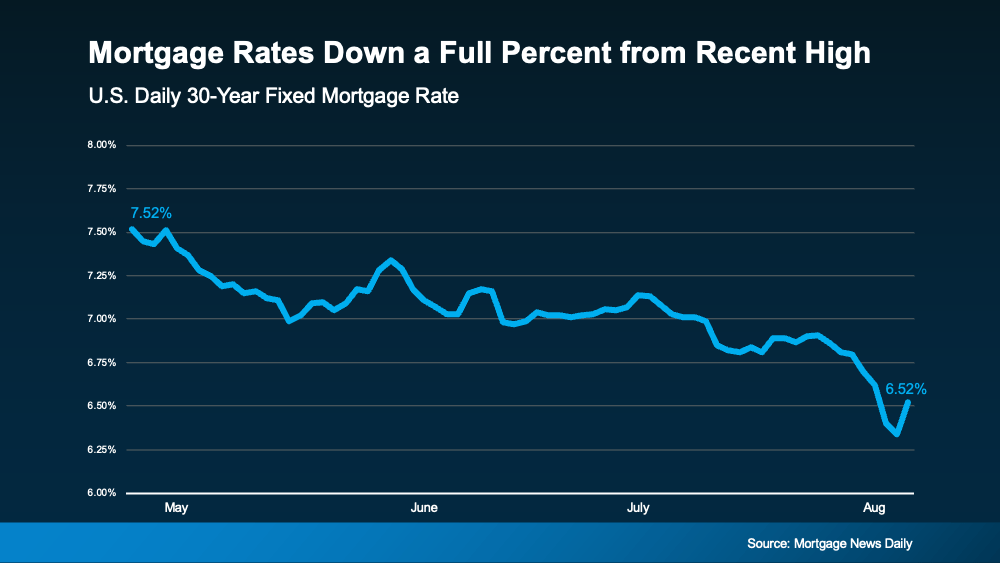

Mortgage Rates Down a Full Percent from Recent High

Mortgage Rates Down a Full Percent from Recent High

Mortgage rates have been one of the hottest topics in the housing market lately because of their impact on affordability. And if you’re someone who’s looking to make a move, you’ve probably been waiting eagerly for rates to come down for that very reason. Well, if the past few weeks are any indication, you may be getting your wish.

Mortgage Rates Trend Down in Recent Weeks

There’s big news for mortgage rates. After the latest reports on the economy, inflation, the unemployment rate, and the Federal Reserve’s recent comments, mortgage rates started dropping a bit. And according to Freddie Mac, they’re now at a level we haven’t seen since February. To help show the downward trend, check out the graph below:

Maybe you’re seeing this and wondering if you should ride the wave and see how low they’ll go. If that’s the case, here’s some important perspective. Remember, the record-low rates from the pandemic are a thing of the past. If you’re holding out hope to see a 3% mortgage rate again, you’re waiting for something experts agree won’t happen. As Greg McBride, Chief Financial Analyst at Bankrate, says:

Maybe you’re seeing this and wondering if you should ride the wave and see how low they’ll go. If that’s the case, here’s some important perspective. Remember, the record-low rates from the pandemic are a thing of the past. If you’re holding out hope to see a 3% mortgage rate again, you’re waiting for something experts agree won’t happen. As Greg McBride, Chief Financial Analyst at Bankrate, says:

“The hopes for lower interest rates need the reality check that ‘lower’ doesn’t mean we’re going back to 3% mortgage rates. . . the best we may be able to hope for over the next year is 5.5 to 6%.”

And with the decrease in recent weeks, you’ve got a big opportunity in front of you right now. It may be enough for you to want to jump back in.

The Relationship Between Rates and Demand

If you wait for mortgage rates to drop further, you might find yourself dealing with more competition as other buyers re-ignite their home searches too.

In the housing market, there’s generally a relationship between mortgage rates and buyer demand. Typically, the higher rates are, the lower buyer demand is. But when rates start to come down, things change. Buyers who were on the fence over higher rates will resume their searches. Here’s what that means for you. As a recent article from Bankrate says:

“If you’re ready to buy, now might be the time to strike. Home prices have been rising primarily because of a longstanding shortage of homes for sale. That’s unlikely to change, and if mortgage rates do fall below 6%, it’s possible buyers would enter the market en masse, further pushing up prices and resurrecting bidding wars.”

Bottom Line

If you’ve been waiting to make your move, the recent downward trend in mortgage rates may be enough to get you off the sidelines. Rates have hit their lowest point in months, and that gives you the opportunity to jump back in before all the other buyers do too.

If you’re ready and able to start the process, reach out and let’s get started.

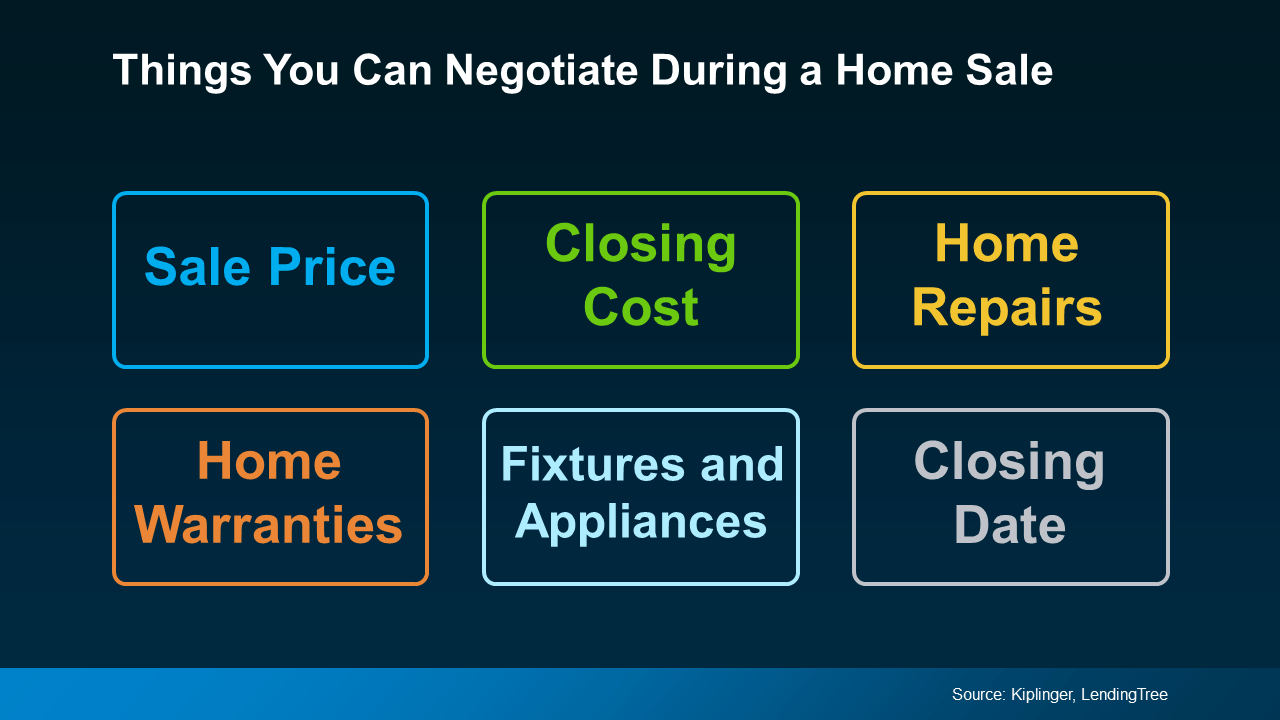

Helpful Negotiation Tactics for Today’s Housing Market

Helpful Negotiation Tactics for Today’s Housing Market

If you haven’t already heard, homebuyers are regaining some negotiating power in today’s market. And while that doesn’t make this a buyer’s market, it does mean buyers may be able to ask for a little more. So, sellers need to be ready for that possibility and know what they’re willing to negotiate.

Whether you’re looking to buy or sell a house, here’s a quick rundown of potential negotiations that may pop up during your transaction. That way, you’re prepared no matter which side of the deal you’re on.

What Can You Negotiate?

Most things in a home purchase are on the negotiation table. Here’s a list of just a few of those options, according to Kiplinger and LendingTree:

- Sale Price: The most obvious is the price of the home. And that lever is being pulled more often today. Buyers don’t want to overpay when affordability is already so tight. And sellers who aren’t realistic about their asking price may have to consider adjusting their price.

- Home Repairs: Based on the inspection, a buyer is within their rights to ask the seller to make reasonable repairs. If the seller doesn’t want to do that, they could offer to reduce the home price or cover some closing costs, so the buyer has the money to take them on themselves.

- Fixtures: Buyers can also ask for appliances or furniture to convey when the house changes hands. Having the seller throw in the washer and dryer cuts down on expenses the buyer would have when moving in. As the seller, you could leave your existing ones behind to sweeten the deal for your buyer, and get yourself new ones for your next place.

- Closing Costs: Closing costs typically run about 2-5% of the home’s purchase price. Buyers can ask the seller to pay for some or all of these expenses to offset the cash the buyer has to bring to the table.

- Home Warranties: Buyers can also ask the seller to pay for a home warranty. This is great for buyers worried about the maintenance costs that may pop up after taking possession of the home. And since this concession usually isn’t terribly expensive for the seller, it can be a good option for both parties.

- Closing Date: Buyers can ask for a faster or extended closing window based on their own timetable. The seller can also advocate for what they need based on their move to find the right compromise.

One thing is true whether you’re a buyer or a seller, and that’s how much your agent can help you throughout the process. Your agent is your go-to for any back-and-forth. They’ll handle the conversations and advocate for your best interests along the way. As Bankrate says:

“Agents have expert negotiating skills. Without one, you must negotiate the terms of the contract on your own.”

They may also be able to uncover what the buyer or seller is looking for in their discussions with the other agent. And that insight can be really valuable at the negotiation table.

Bottom Line

Buyers are regaining a bit of negotiation power in today’s market. Buyers, knowing what levers you can pull will help you feel confident and empowered going into your purchase. Sellers, having a heads up of what they may ask for gives you the chance to think through what you’ll be willing to offer.

Want to chat more about what to expect and the options you have? Let’s connect.

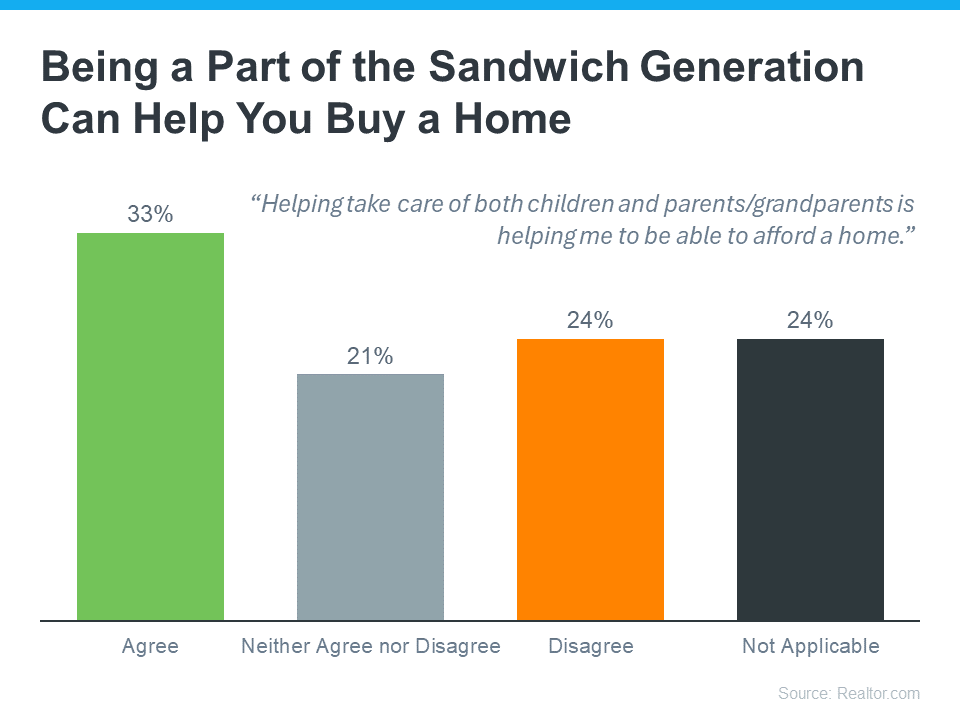

Why the Sandwich Generation Is Buying Multi-Generational Homes

Why the Sandwich Generation Is Buying Multi-Generational Homes

Are you a part of the Sandwich Generation? According to Realtor.com, that’s a name for the roughly one in six Americans who take care of their children and their parents or grandparents at the same time.

If that sounds familiar to you, juggling all the responsibilities involved certainly must have its challenges. But it turns out there’s one pretty significant benefit: it can actually make it a bit easier for you to buy a home.

How Can It Help You Buy a Home?

Realtor.com asked members of the Sandwich Generation if they agree or disagree that taking care of children and parents at the same time is helping them afford a home. A third of respondents said their situation made it easier to buy (see graph below):

Here are a few ways their caretaking situation might be helping those 33% buy a home:

Here are a few ways their caretaking situation might be helping those 33% buy a home:

- Sharing Expenses: If you live in a multi-generational household, you can pool your resources and split the costs. Your parents might contribute to the mortgage or help with other bills. This can make a big difference, especially in today’s housing market. It may help you afford a larger home than you could on your own.

- Built-In Childcare: Having grandparents in the home could also save you money on childcare. They can help watch your kids while you’re at work, which means you can save on daycare costs too.

Beyond just the financial reasons, buying a multi-generational home has other advantages. The Profile of Home Buyers and Sellers from the National Association of Realtors (NAR) highlights some of the most popular, including:

- Easier To Care for Aging Parents: It’s more convenient to take care of someone when you live with them. Also, your elderly parents may very well be happier and healthier, thanks to more social interaction and a feeling of connectedness.

- Spending More Time Together: Once you live together, you get to spend more time and create even more lasting memories with your loved ones.

The Mortgage Reports sums it up this way:

“Buying a house with your parents can be a great way to ease caregiving, support young children, or simply bring loved ones closer together. And considering the steep rise in home prices over the last few years, it can make homeownership a lot more affordable.”

How a Real Estate Agent Can Help

If you’re in the Sandwich Generation and thinking about buying a multi-generational home, working with a local real estate agent is essential. Finding a home that works for so many people can be tricky. An agent will use their expertise to help you find one that meets the needs of, and has enough space for, everyone who’s going to live there.

Bottom Line

Being a part of the Sandwich Generation comes with its challenges – but it also might come with one truly great perk. If you’re looking to buy a home, your caregiving situation can actually make it a bit easier for you to afford a home. To learn more, let’s connect.

Are Home Prices Going To Come Down?

Are Home Prices Going To Come Down?

Today’s headlines and news stories about home prices are confusing and make it tough to know what’s really happening. Some say home prices are heading for a correction, but what do the facts say? Well, it helps to start by looking at what a correction means.

Here’s what Danielle Hale, Chief Economist at Realtor.com, says:

“In stock market terms, a correction is generally referred to as a 10 to 20% drop in prices . . . We don’t have the same established definitions in the housing market.”

In the context of today’s housing market, it doesn’t mean home prices are going to fall dramatically. It only means prices, which have been increasing rapidly over the last couple years, are normalizing a bit. In other words, they’re now growing at a slower pace. Prices vary a lot by local market, but rest assured, a big drop off isn’t what’s happening at a national level.

The Real Estate Market Is Normalizing

From 2020 to 2022, home prices skyrocketed. That rapid increase was due to high demand, low interest rates, and a shortage of homes for sale. But, that kind of aggressive growth couldn’t continue forever.

Today, price growth has started to slow down, which is a sign the market is beginning to normalize. The most recent data from Case-Shiller shows that after being basically flat for a couple of months last year, prices are going up at a national level – just not as quickly as before (see graph below):

The big takeaway? So far this year, there’s been a much healthier pace of price growth compared to the pandemic.

The big takeaway? So far this year, there’s been a much healthier pace of price growth compared to the pandemic.

Of course, that’s what’s happening now, but you may be wondering what’s next for prices. Marco Santarelli, the Founder of Norada Real Estate Investments, says:

“Expert forecasts lean towards a moderation in home price growth over the next five years. This translates to a slower and more sustainable pace of appreciation compared to the breakneck speed witnessed in recent years, rather than a freefall in prices.”

It’s all about supply and demand. Increasing inventory plus limited buyer demand, due to relatively high mortgage rates, will continue to ease some of the upward pressure on prices.

What This Means for You

If you’re thinking about buying a home, slowing price growth is welcome news. Skyrocketing home prices during the pandemic left many would-be homebuyers feeling priced-out.

While it’s still a good thing to know the value of the home you buy will likely continue to go up once you own it, slowing price gains are making things feel more manageable. Odeta Kushi, Deputy Chief Economist at First American, says:

“While housing affordability is low for potential first-time home buyers, slowing price appreciation and lower mortgage rates could help — so the dream of homeownership isn’t boarded up just yet.”

Bottom Line

At the national level, home prices are not going down. And most experts forecast they’ll continue growing moderately moving forward. But prices vary a lot by local market. That’s where a trusted real estate agent comes into play. If you have questions about what’s happening with prices in our area, reach out.

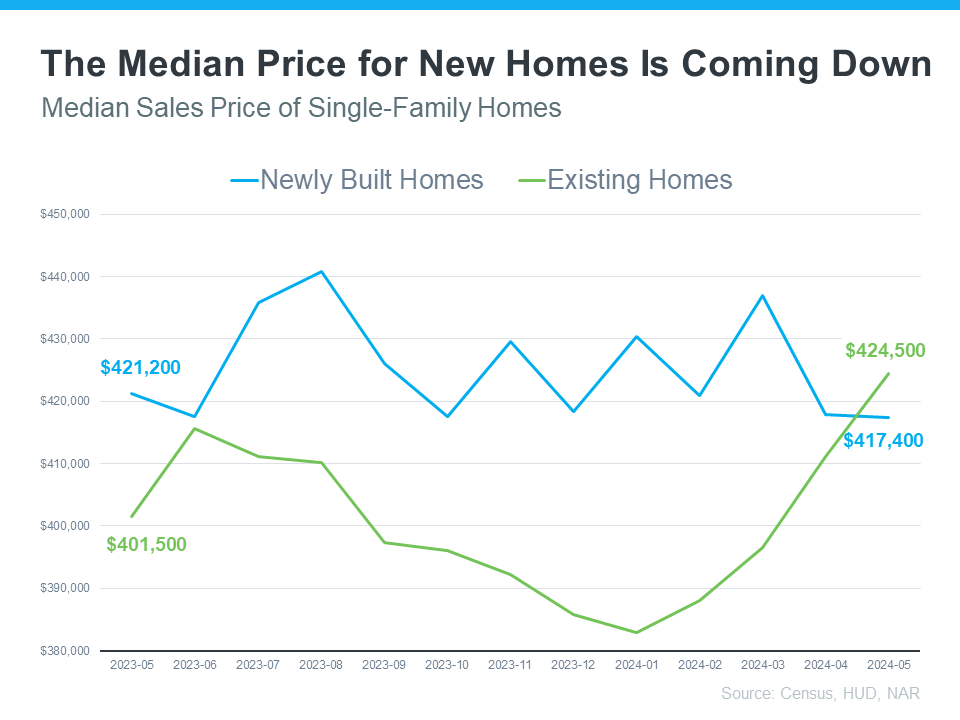

A Newly Built Home May Actually Be More Budget-Friendly

A Newly Built Home May Actually Be More Budget-Friendly

If you’re in the market to buy a home, there’s some exciting news for you. Many people assume that newly built homes are more expensive than existing ones (houses that have already been lived in), but that’s not always the case. In fact, exploring newly built homes can sometimes lead to more cost-effective options, especially today. Hard to believe, right? But the data doesn’t lie.

Here are two key reasons working with your agent to look into new home construction could help you find a more budget-friendly option.

Reason 1: Lower Median Prices for Newly Built Homes

The median sales price for newly built homes is lower than the median sales price for existing homes today. This might seem surprising, but it’s true according to the latest data from the Census and the National Association of Realtors (NAR):

Why is that? Builders are focused on building what they can sell. And right now, there’s a very real need for smaller and more affordable homes – so that’s what they’ve been bringing to the market. At the same time, there are also more newly built homes already on the market than there have been over the past few years, so builders are motivated to make sure they’re selling what they’ve got available before adding more.

Reason 2: Attractive Incentives from Home Builders

Another big reason to consider a newly built home is the range of incentives that many home builders are offering. Again, since builders are aiming to sell their current inventory, some are providing special deals to sweeten the pot for homebuyers. HousingWire explains today’s trend:

“Overall, the usage of sales incentives was up to 61% in June, compared to 59% in May.”

One of the most appealing incentives right now is how builders are able to offer competitive mortgage rates. They may also provide other incentives, such as covering closing costs, or offering free upgrades.

Why This Matters to You

Considering a newly built home could open up opportunities you hadn’t thought of before. With competitive pricing and attractive incentives, you might just find that a brand-new home is the most appealing option for you.

Bottom Line

Buying a home is a big decision, and it’s essential to consider all your options. By looking into newly built homes, you might find a perfect fit for your needs and your budget.

Let’s explore the possibilities together. If you have any questions or want to see what’s available, feel free to reach out.

Why a Foreclosure Wave Isn’t on the Horizon

Why a Foreclosure Wave Isn’t on the Horizon

Even though data shows inflation is cooling, a lot of people are still feeling the pinch on their wallets. And those high costs on everything from gas to groceries are fueling unnecessary concerns that more people are going to have trouble making their mortgage payments. But, does that mean there’s a big wave of foreclosures coming?

Here’s a look at why the data and the experts say that’s not going to happen.

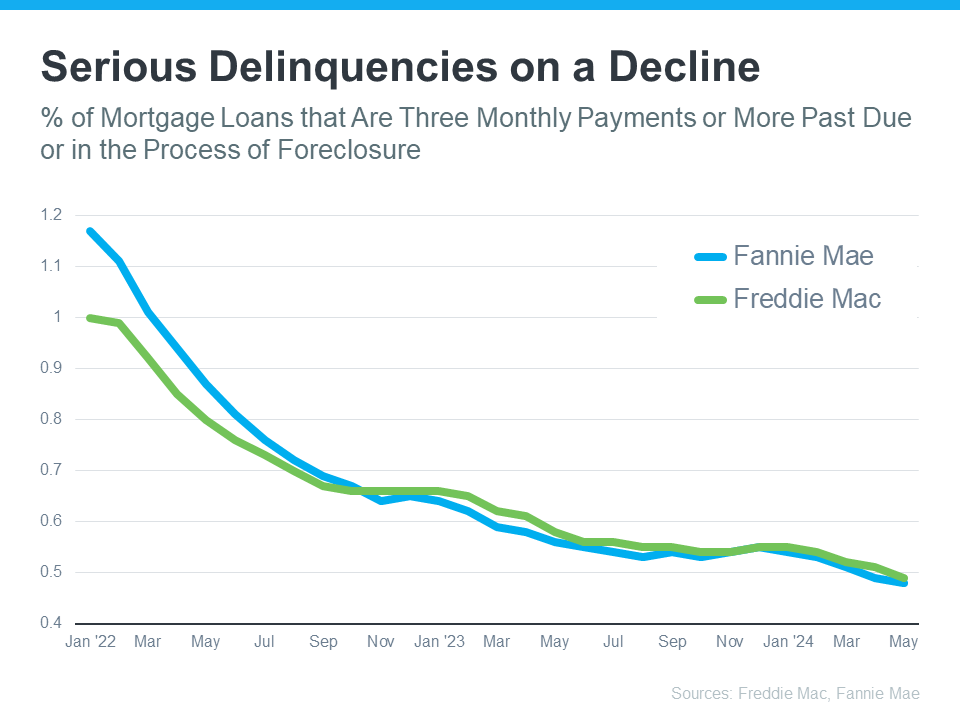

There Aren’t Many Homeowners Who Are Seriously Behind on Their Mortgages

One of the main reasons there were so many foreclosures during the last housing crash was because relaxed lending standards made it easy for people to take out mortgages, even when they couldn’t show they’d be able to pay them back. At that time, lenders weren’t being as strict when looking at applicant credit scores, income levels, employment status, and debt-to-income ratio.

But since then, lending standards have gotten a whole lot tighter. Lenders became much more diligent when assessing applicants for home loans. And that means we’re seeing more qualified buyers who have less of a risk of defaulting on their loans.

That’s why data from Freddie Mac and Fannie Mae shows the number of homeowners who are seriously behind on their mortgage payments (known in the industry as delinquencies) has been declining for quite some time. Take a look at the graph below:

What this means is that, not only are borrowers more qualified, but they’re also finding ways to navigate through their challenges, exploring their repayment options, or maybe even using the record amount of equity they have to sell and avoid foreclosure entirely.

The Answer Is: There’s No Sign of a Wave Coming

Before there can be a significant rise in foreclosures, the number of people who can’t make their mortgage payments would need to rise significantly. But, since so many buyers are making their payments today and homeowners have so much equity built up, a wave of foreclosures isn’t likely.

Take it from Bill McBride of Calculated Risk – an expert on the housing market who, after closely following the data and market leading up to the crash, was able to see the foreclosure crisis coming in 2008. McBride says:

“We will NOT see a surge in foreclosures that would significantly impact house prices (as happened following the housing bubble) for two key reasons: 1) mortgage lending has been solid, and 2) most homeowners have substantial equity in their homes.”

Bottom Line

If you’re worried about a potential foreclosure crisis, know there’s nothing in the data to suggest that’ll happen. Buyers are more qualified now, and that’s one reason why they’re not falling seriously behind on their mortgage payments.

How Affordability and Remote Work Are Changing Where People Live

How Affordability and Remote Work Are Changing Where People Live

There’s an interesting trend happening in the housing market. People are increasingly moving to more affordable areas, and remote or hybrid work is helping them do it.

Consider Moving to a More Affordable Area

Today’s high mortgage rates combined with continually rising home prices mean it’s tough for a lot of people to afford a home right now. That’s why many interested buyers are moving to places where homes are less expensive, and the cost of living is lower. As Orphe Divounguy, Senior Economist at Zillow, explains:

“Housing affordability has always mattered . . . and you’re seeing it across the country. Housing affordability is reshaping migration trends.”

If you’re hoping to buy a home soon, it might make sense to broaden your search area to include places where homes that fit your needs are more affordable. That’s what a lot of other people are doing right now to find a home within their budget. Extra Space Storage explains:

“55% of American adults are looking to relocate to a different state or city for more affordable homes and lower costs of living. . . Specifically, states with a strong economy, lower costs of living, and remote work options continue to be the ideal places to live in the U.S.”

Remote Work Opens Up More Home Options

If you work remotely or drive into the office only a few times each week, you have many more possibilities when looking for your next home. That’s because you can cast a broader net and include more suburban or rural areas nearby. As Market Place Homes says:

“People start to reconsider where they want to live when commute times are slashed in half or eliminated altogether. If they have a longer commute but don’t have to do it daily, they may feel like they can tolerate living farther away from their job. Or, if someone works entirely remotely, they can move to a cheaper area and get a lot of house for their dollar.”

How a Real Estate Agent Can Help

A real estate agent can help you find the perfect home for your budget. They’re especially valuable if you’re moving to a new, unfamiliar area. Bankrate says:

“If you’re moving far away, you may not have a good idea about which neighborhoods or towns will be the best fit. An experienced local agent can help you find the lifestyle you’re looking for in a home you can afford.”

So, if you’re thinking about relocating to somewhere with more affordable homes, what are you waiting for? With the added flexibility of remote work, you might have more options than before.

Bottom Line

Dreaming of a place where your money goes further? Let’s connect so you have someone to help you find your next home. Together, we’ll make your dream of homeownership a reality.

Unlocking Homebuyer Opportunities in 2024

Unlocking Homebuyer Opportunities in 2024

There’s no arguing this past year has been difficult for homebuyers. And if you’re someone who has started the process of searching for a home, maybe you put your search on hold because the challenges in today’s market felt like too much to tackle. You’re not alone in that. A Bright MLS study found some of the top reasons buyers paused their search in late 2023 and early 2024 were:

- They couldn’t find anything in their price range

- They didn’t have any successful offers or had difficulty competing

- They couldn’t find the right home

If any of these sound like why you stopped looking, here’s what you need to know. The housing market is in a transition in the second half of 2024. Here are four reasons why this may be your chance to jump back in.

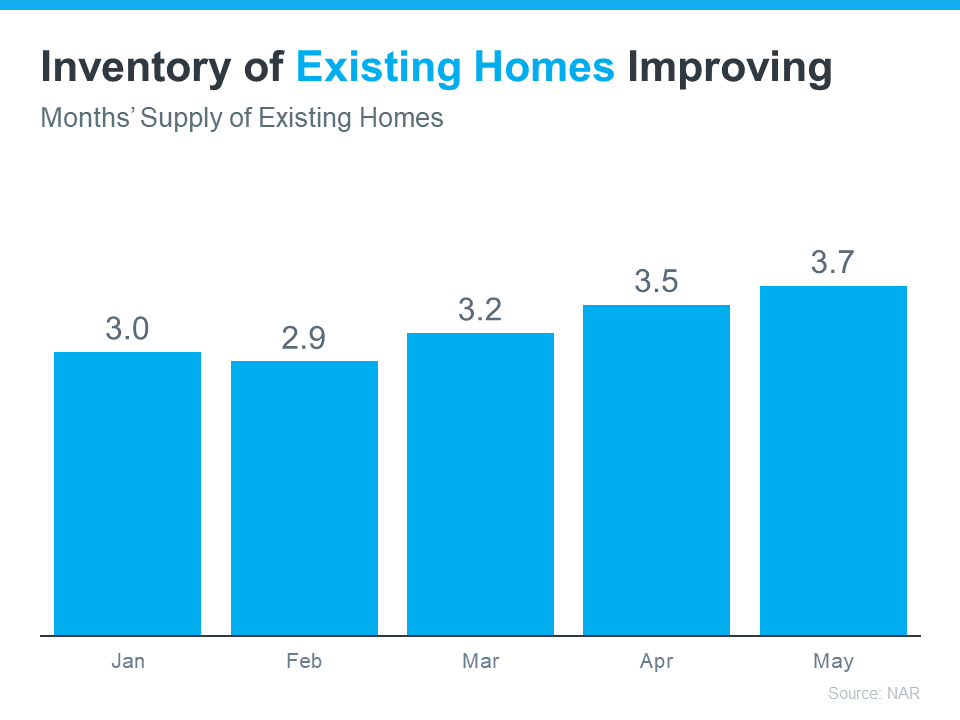

1. The Supply of Homes for Sale Is Growing

One of the most significant shifts in the market this year is how the months’ supply of homes for sale has increased. If you look at data from the National Association of Realtors (NAR), you’ll see how inventory has grown throughout 2024 (see graph below):

This graph shows the months’ supply of existing homes – homes that were previously lived in by another homeowner. The upward trend this year is clear.

This increase means you have a better chance of finding a home that suits your needs and preferences. And if the biggest reason you put off your home search was difficulty finding the right home, this is a big relief.

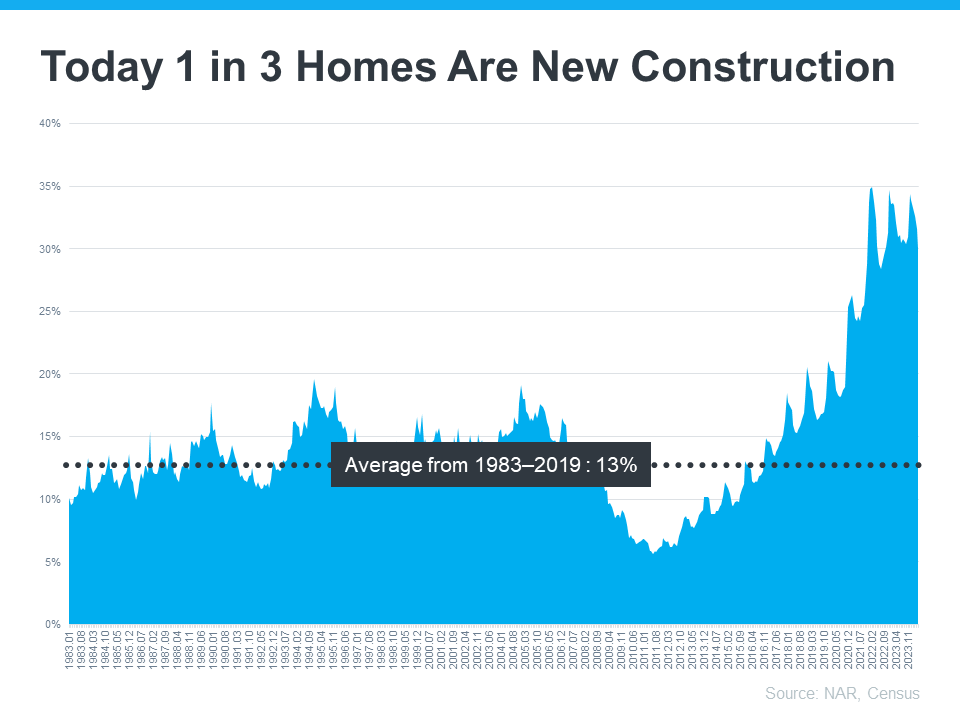

2. There’s More New Home Construction

And if you still don’t see an existing home you like, another big opportunity lies in the rise of new home construction. Builders have worked to increase the supply of newly built homes this year. And they’ve turned their attention to crafting smaller, more affordable homes based on what’s most needed in today’s market. This helps address the long-standing issue of housing undersupply throughout the country, and those smaller homes also offset some of the affordability challenges you’re feeling today.

According to data from the Census and NAR, one in three homes on the market is a newly built home (see graph below):

This means, that if you didn’t previously look at newly built homes as part of your search, you may have been cutting your pool of options by a third. Not to mention, some builders are also offering incentives like buying down mortgage rates to make it easier for buyers to get a home that fits their budget.

So, consider talking to your agent about what builders have to offer in your area. Your agent’s expertise on builder reputations, contracts, and more will help you weigh your options.

3. Less Buyer Competition

Mortgage rates are still hovering around 7%, so buyer demand isn’t as fierce as it once was. And when you combine that with more housing supply, you have a better chance of avoiding an intense bidding war. Danielle Hale, Chief Economist at Realtor.com, highlights the positive trend for the latter half of 2024, saying:

“Home shoppers who persist could see better conditions in the second half of the year, which tends to be somewhat less competitive seasonally, and might be even more so since inventory is likely to reach five-year highs.”

This creates a unique opportunity for you to find a home you want to buy with less stress and at a potentially better price.

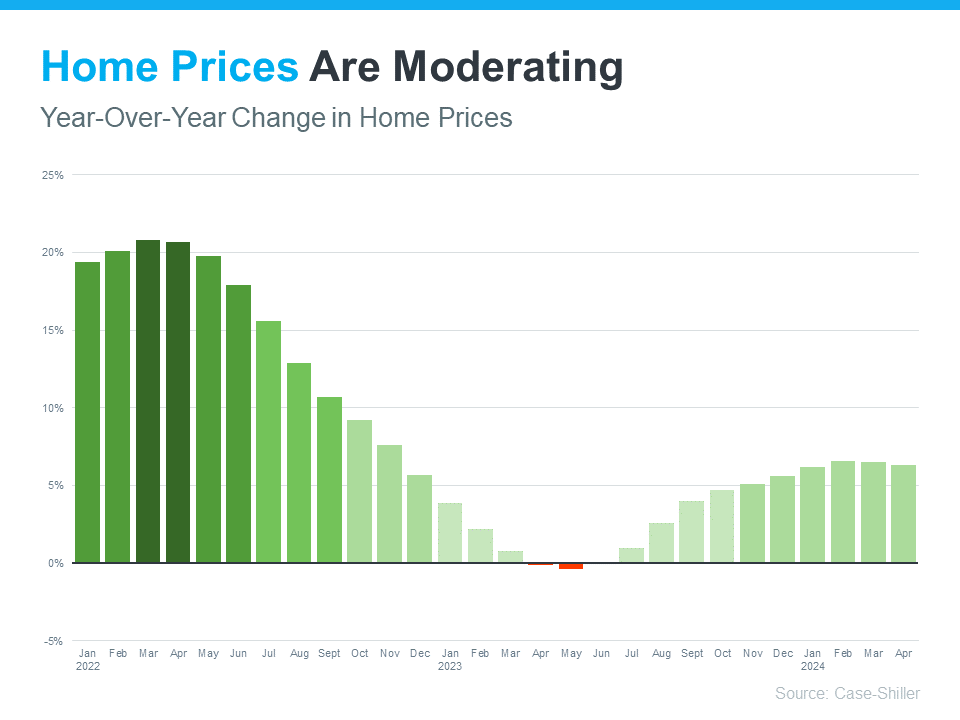

4. Home Prices Are Moderating

Speaking of prices, home prices are also showing signs of moderation – and that’s a welcome shift after the rapid appreciation seen in recent years (see graph below):

This moderation is mostly due to supply and demand. Supply is growing and demand is easing, so prices aren’t rising as fast. But make no mistake, that doesn’t mean prices are falling – they’re just rising at a more normal pace. You can see this in the graph. The bars are still showing prices increasing, just not as dramatic as it was before.

The average forecast for home price appreciation in 2024 is for positive growth around 3% to 5%, which is more in line with historical norms. That moderation means that you are less likely to face the steep price increases we saw a few years ago.

The Opportunity in Front of You

If you’re ready and able to buy, you may find that the second half of 2024 is a bit easier to navigate. There are still challenges, but some of the biggest hurdles you’ve faced are getting better as time wears on.

On the other hand, you could choose to wait. But if you do, here’s the risk you run. As more buyers recognize the shift in the market, competition will grow again. On a similar note, if mortgage rates do come down (as forecasts say), more buyers will flood back into the market. So, making a move now helps you take advantage of the current market conditions and get ahead of those other buyers.

Bottom Line

If you’ve put your dream of homeownership on hold, the second half of 2024 may be your chance to jump back in. Let’s connect to talk more about the opportunities you have in today’s market.

How To Determine if You’re Ready To Buy a Home

How To Determine if You’re Ready To Buy a Home

If you’re trying to decide if you’re ready to buy a home, there’s probably a lot on your mind. You’re thinking about your finances, today’s mortgage rates and home prices, the limited supply of homes for sale, and more. And, you’re juggling how all of those things will impact the choice you’ll make.

While housing market conditions are definitely a factor in your decision, your own personal situation and your finances matter too. As an article from NerdWallet says:

“Housing market trends give important context. But whether this is a good time to buy a house also depends on your financial situation, life goals and readiness to become a homeowner.”

Instead of trying to time the market, focus on what you can control. Here are a few questions that can give you clarity on whether you’re ready to make your move.

1. Do You Have a Stable Job?

One thing to consider is how stable you feel your employment is. Buying a home is a big purchase, and you’re going to sign a home loan stating you’ll pay that loan back. That’s a big commitment. Knowing you have a reliable job and a steady stream of income coming in can help put your mind at ease when making such a large purchase.

2. Have You Figured Out What You Can Afford?

If you have reliable paychecks coming in, the next thing to figure out is what you can afford. That’ll depend on your spending habits, debt, and more. To be sure you have a good idea of what to expect from a number’s perspective, start by talking to a trusted lender.

They’ll be able to tell you about the pre-approval process and what you’re qualified to borrow, current mortgage rates and your approximate monthly payment, closing costs to anticipate, and other expenses you’ll want to budget for. That way you can make an informed decision about whether you’re ready to buy.

3. Do You Have an Emergency Fund?

Another key factor is whether you’ll have enough cash left over in case of an emergency. While that’s not fun to think about, it’s an important thing to consider. You don’t want to overextend on the house, and then not be able to weather a storm if one comes along. As CNET says:

“You’ll want to have a financial cushion that can cover several months of living expenses, including mortgage payments, in case of unforeseen circumstances, such as job loss or medical emergencies.”

4. How Long Do You Plan To Live There?

It was mentioned above, but buying a home involves some upfront expenses. And while you’ll get that money back (and more) as you gain equity, that process takes time. If you plan to move too soon, you may not recoup your investment. For example, if you’re looking to sell and move again in a year, it might not make sense to buy right now. As Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), explains:

“Five years is a good, comfortable mark. If the price of your home appreciates considerably, then even three years would be fine.”

So, think about your future. If you plan to transfer to a new city with the upcoming promotion you’re working toward or you anticipate your loved ones will need you to move closer to take care of them, that’s something to factor in.

5. Above all else, the most important question to answer is: do you have a team of real estate professionals in place?

If not, finding a trusted local agent and a lender is a good first step. The pros can talk you through your options and help you decide if you’re ready to take the plunge or if you have a few more things to get in order first.

Bottom Line

If you want to have a conversation about all the things you need to consider to determine if you’re ready to buy, let’s connect.

Why Working with a Real Estate Professional Is Crucial Right Now

Why Working with a Real Estate Professional Is Crucial Right Now

Navigating the housing market can be tricky, especially these days. That’s why having an experienced guide when buying or selling a home is so important. The market isn’t exactly straightforward right now, and working with a real estate expert can offer insights and advice that make all the difference.

While today’s market conditions might seem confusing or overwhelming, you don’t have to handle them alone. With a trusted expert leading you through every step, you can navigate the process with the clarity and confidence you deserve.

Here are just a few of the ways a real estate expert is invaluable:

Contracts – Agents help with the disclosures and contracts necessary in today’s heavily regulated environment.

Experience – In today’s market, experience is crucial. Real estate professionals know the entire sales process, including how it’s changing right now.

Negotiations – Your real estate advisor acts as a buffer in negotiations with all parties, and advocates for your best interests throughout the entire transaction.

Industry Expertise– Knowledge is power in today’s market, and your advisor will simply and effectively explain processes, market conditions, and key terms, translating what they mean for you along the way along the way.

Pricing – A real estate professional understands current real estate values when setting the price of your home or helping you make an offer to purchase one. Pricing matters more than ever right now, so having expert advice will help ensure you’re set up for success.

A real estate agent is a crucial guide through this challenging market, but not all agents are created equal. A true expert can carefully walk you through the whole real estate process, look out for your unique needs, and advise you on the best ways to achieve success.

Finding an expert real estate advisor – not just any agent – should be your top priority if you want to buy or sell a home. As Bankrate says:

“Real estate is very localized, and you want someone who’s extremely knowledgeable about the market in your specific area. You should also look for someone with a successful track record of negotiating and closing deals, preferably for homes similar to the kind you want to buy.”

What’s the Key To Choosing the Right Expert?

Like any relationship, it starts with trust. You’ll want to know you can depend on that person to always put you and your best interests first. That means hiring a true professional. As Business Insider explains:

“As long as you’ve properly vetted the agents you’re considering and ensured they have the necessary expertise, it’s ok to go with your gut when making your final decision on which real estate agent you want to work with. You’re going to be working closely with this person, so it’s important to choose an agent you’re comfortable with.”

Bottom Line

It’s critical to have an expert on your side who’s well-versed in navigating today’s housing market dynamics. If you’re planning to buy or sell a home this year, let’s connect so you have a real estate professional to give you the best advice and guide you along the way.

The Price of Perfection: Don’t Wait for the Perfect Home

The Price of Perfection: Don’t Wait for the Perfect Home

In life, patience is a virtue – but in the world of homebuying, waiting too long in hopes of finding the perfect home actually isn’t wise. That’s because the pursuit of perfection comes at a cost. And in this case, that cost may be delaying your dream of homeownership. As Bankrate explains:

“One of the most common first-time homebuyer mistakes is looking for a home that checks each of your boxes. Looking for perfection can narrow your choices and lead you to pass over good, suitable options for starter homes in the hopes that something better will come along.”

The Cost of Holding Out for Perfection

Nothing in life is ever perfect – and that’s true when you search for a home too. Unless you’re building a brand-new home from the ground up, chances are there are going to be some features or finishes you wouldn’t have picked yourself. It may be as simple as paint colors, a light fixture, or the tile in the bathrooms or kitchen. Or even that the backyard isn’t fenced in. It could also be that the home itself is great, but it’s not the ideal location you were hoping for.

But here’s the trade-off you’d be making without even realizing it. In all that time you’d spend searching for the perfect place, you’d overlook a lot of homes that would’ve worked for you. U.S. News explains:

“. . . you may miss opportunities if you enter the process with blinders on and aren’t open-minded . . . Countless potential buyers never buy because of this, and thus miss great investments or never move on to the next chapter of their lives.”

It’s Time To Redefine Perfection

Especially with affordability and inventory where they are today, buying a home that needs some updates, is a few neighborhoods away from your ideal location, or doesn’t have all your desired features can be a smart move. Here’s why.

For starters, these homes are usually more affordable, which is important at a time when some buyers are struggling to find options in their budget.

And they give you a chance to make the space your own or discover a whole new area of town. You may find out you actually love that neighborhood. Or, swapping out a feature here or there after move-in isn’t such a big deal. So, look past the green shag carpet and see the bones of the house. With a little vision and creativity, you can turn a good house into a fantastic home.

How an Agent Helps You Explore Your Options

If you’re open to a home that needs a little elbow grease or is a bit further out, let your agent know. They’ll be happy to show you how this can really open up your pool of homes to pick from. They’ll also help coach you through this process by:

1. Prioritizing Your Must-Haves: Your agent will want to revisit your wish list and separate your non-negotiables from your nice-to-haves. From there, they’ll focus on what’s really most important to you as they come up with a bigger list of options for you to choose from.

2. Coaching You To See the Potential: As you tour these added options, your agent will help you look beyond cosmetic flaws and imagine what the home could be with a little work. Simple updates like a fresh coat of paint or new flooring can make a big difference.

3. Connecting You with Local Pros: And an agent’s support goes one step further. If they know what you’re hoping to change after you move in, they can connect you with local pros who can get the job done. That way it’s less work for you, and you don’t have to worry about tracking down contractors.

Bottom Line

Remember, there is no perfect home. But with expert help and an open mind, we can find you the right home – even in today’s market. Let’s connect to see what’s out there.

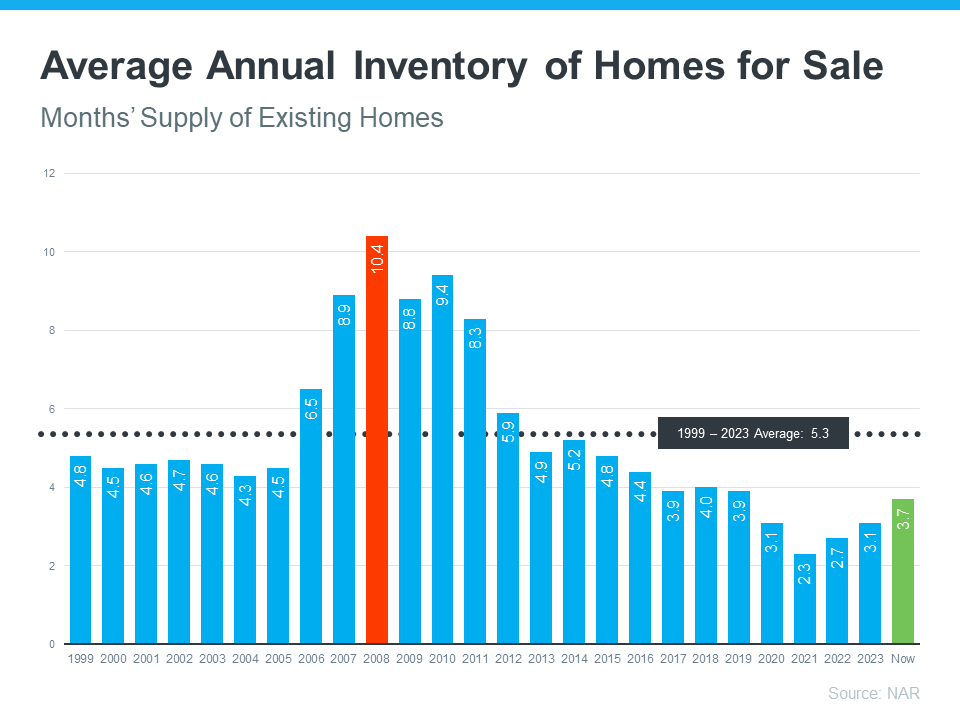

Not a Crash: 3 Graphs That Show How Today’s Inventory Differs from 2008

Not a Crash: 3 Graphs That Show How Today’s Inventory Differs from 2008

Even if you didn’t own a home at the time, you probably remember the housing crisis in 2008. That crash impacted the lives of countless people, and many now live with the worry that something like that could happen again. But rest easy, because things are different than they were back then. As Business Insider says:

“Though many Americans believe the housing market is at risk of crashing, the economists who study housing market conditions overwhelmingly do not expect a crash in 2024 or beyond.”

Here’s why experts are so confident. For the market (and home prices) to crash, there would have to be too many houses for sale, but the data doesn’t show that’s happening. Right now, there’s an undersupply, not an oversupply like the last time – and that’s true even with the inventory growth we’ve seen this year. You see, the housing supply comes from three main sources:

- Homeowners deciding to sell their houses (existing homes)

- New home construction (newly built homes)

- Distressed properties (foreclosures or short sales)

And if we look at those three main sources of inventory, you’ll see it’s clear this isn’t like 2008.

Homeowners Deciding To Sell Their Houses

Although the supply of existing (previously owned) homes is up compared to this time last year, it’s still low overall. And while this varies by local market, nationally, the current months’ supply is well below the norm, and even further below what we saw during the crash. The graph below shows this more clearly.

If you look at the latest data (shown in green), compared to 2008 (shown in red), we only have about a third of that available inventory today.

So, what does this mean? There just aren’t enough homes available to make values drop. To have a repeat of 2008, there’d need to be a lot more people selling their houses with very few buyers, and that’s not the case right now.

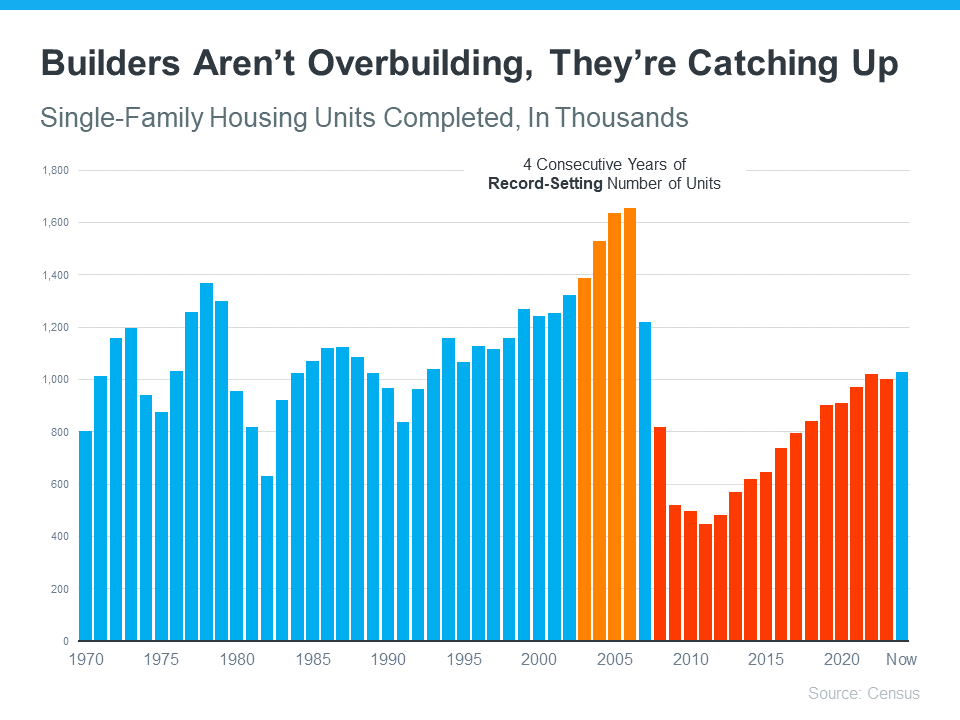

New Home Construction

People are also talking a lot about what’s going on with newly built houses these days, and that might make you wonder if homebuilders are overdoing it. Even though new homes make up a larger percentage of the total inventory than the norm, there’s no need for alarm. Here’s why.

The graph below uses data from the Census to show the number of new houses built over the last 52 years. The orange on the graph shows the overbuilding that happened in the lead-up to the crash. And, if you look at the red in the graph, you’ll see that builders have been underbuilding pretty consistently since then:

There’s just too much of a gap to make up. Builders aren’t overbuilding today, they’re catching up. A recent article from Bankrate says:

“What’s more, builders remember the Great Recession all too well, and they’ve been cautious about their pace of construction. The result is an ongoing shortage of homes for sale.”

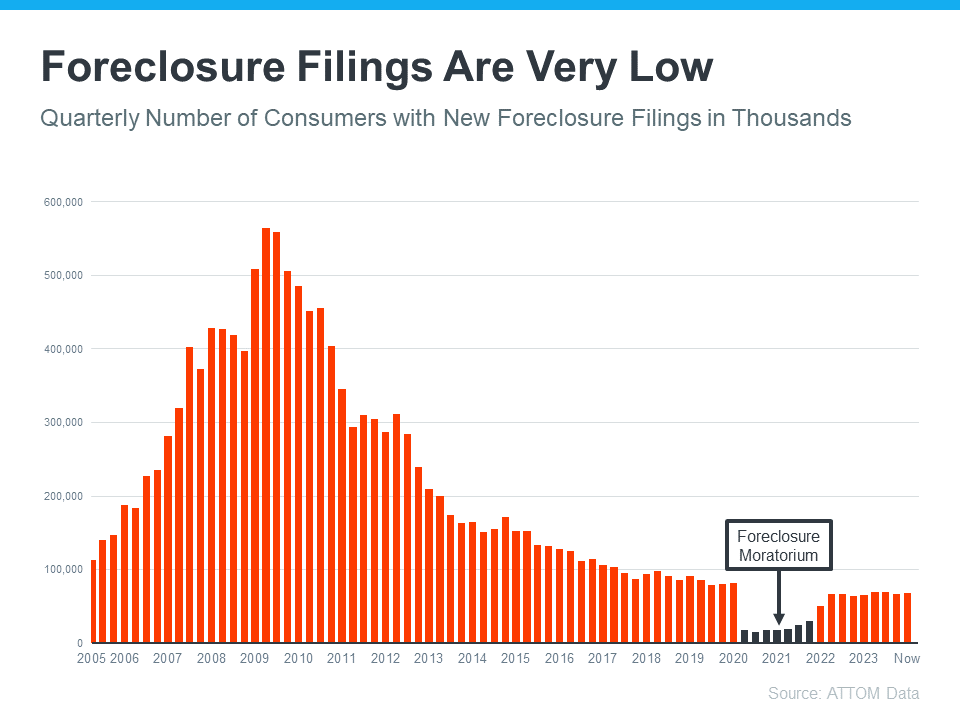

Distressed Properties (Foreclosures and Short Sales)

The last place inventory can come from is distressed properties, including short sales and foreclosures. During the housing crisis, there was a flood of foreclosures due to lending standards that allowed many people to get a home loan they couldn’t truly afford.

Today, lending standards are much tighter, resulting in more qualified buyers and far fewer foreclosures. The graph below uses data from ATTOM to show how things have changed since the housing crash:

This graph makes it clear that as lending standards got tighter and buyers became more qualified, the number of foreclosures started to go down. And in 2020 and 2021, the combination of a moratorium on foreclosures (shown in black) and the forbearance program helped prevent a repeat of the wave of foreclosures we saw when the market crashed.

While you may see headlines that foreclosure volume is ticking up – remember, that’s only compared to recent years when very few foreclosures happened. We’re still below the normal level we’d see in a typical year.

What This Means for You

Inventory levels aren’t anywhere near where they’d need to be for prices to drop significantly and the housing market to crash. As Forbes explains:

“As already-high home prices continue trending upward, you may be concerned that we’re in a bubble ready to pop. However, the likelihood of a housing market crash—a rapid drop in unsustainably high home prices due to waning demand—remains low for 2024.”

Mark Fleming, Chief Economist at First American, points to the laws of supply and demand as a reason why we aren’t headed for a crash:

“There’s just generally not enough supply. There are more people than housing inventory. It’s Econ 101.”

And Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), says:

“We will not have a repeat of the 2008–2012 housing market crash. There are no risky subprime mortgages that could implode, nor the combination of a massive oversupply and overproduction of homes.”

Bottom Line

The market doesn’t have enough available homes for a repeat of the 2008 housing crisis – and there’s nothing that suggests that will change anytime soon. That’s why housing experts and inventory data tell us there isn’t a crash on the horizon.

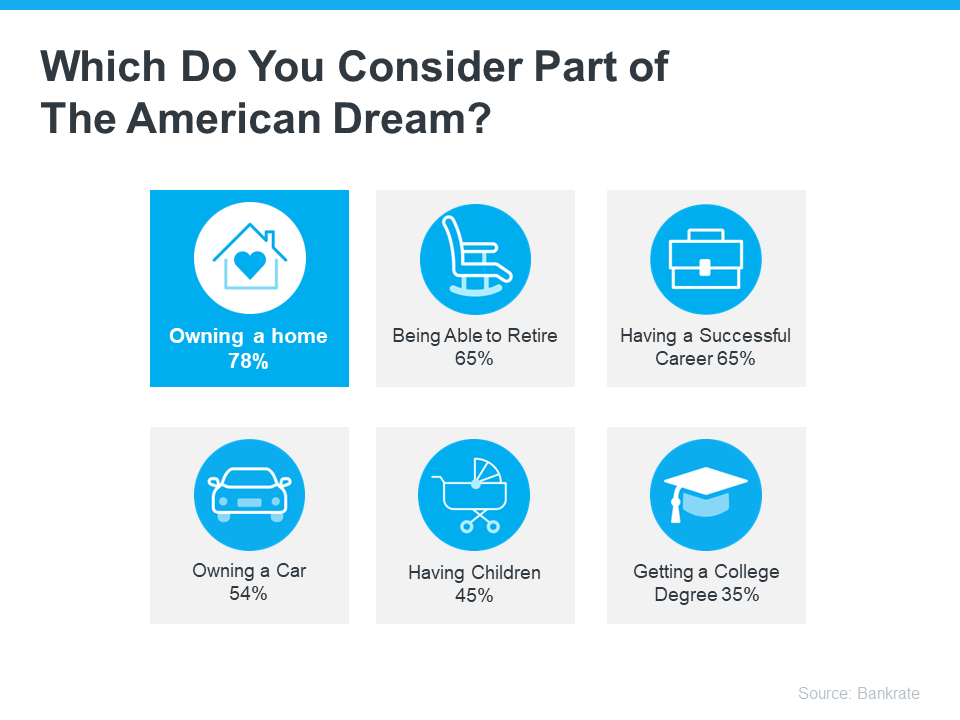

Homeownership: The Heart of the American Dream

Homeownership: The Heart of the American Dream

Everyone’s vision for the future is personal and unique. But for many, common goals include success, freedom, and prosperity — values closely tied to having your own home and the iconic feeling of achieving the American Dream.

A recent survey by Bankrate reveals exactly that: homeownership is still a part of the American Dream. The results show, at 78%, that owning a home tops the list, surpassing other significant milestones such as retirement, having a successful career, and more (see below):

So, why is buying a home important to so many today? One reason is the financial and physical security it provides. Many people see homeownership as a way to reduce stress because owning a home with a fixed-rate mortgage stabilizes what is likely their largest monthly expense.

Another factor is the potential for building wealth. That’s because, over time, homeowners gain equity as they pay down their mortgage and as home prices appreciate, leading to longer-term financial stability.

But what about the responsibilities that come with owning and maintaining a home? According to a survey by Entrata, only 23% of renters feel homeownership is too much work, indicating the majority are open to the commitments and obligations that come with being a homeowner.

What Does This Mean for You?

While buying a home today might seem daunting due to higher mortgage rates and rising home prices, the long-term benefits can make it worthwhile. If you’re considering homeownership, remember that it’s more than just a financial investment — it’s a step toward securing your future.

Bottom Line

Owning a home is a significant and powerful decision that represents a big part of the American Dream. If you’re ready to take this step, let’s connect so you have someone who can guide you through the process and help you make your homeownership goals a reality.

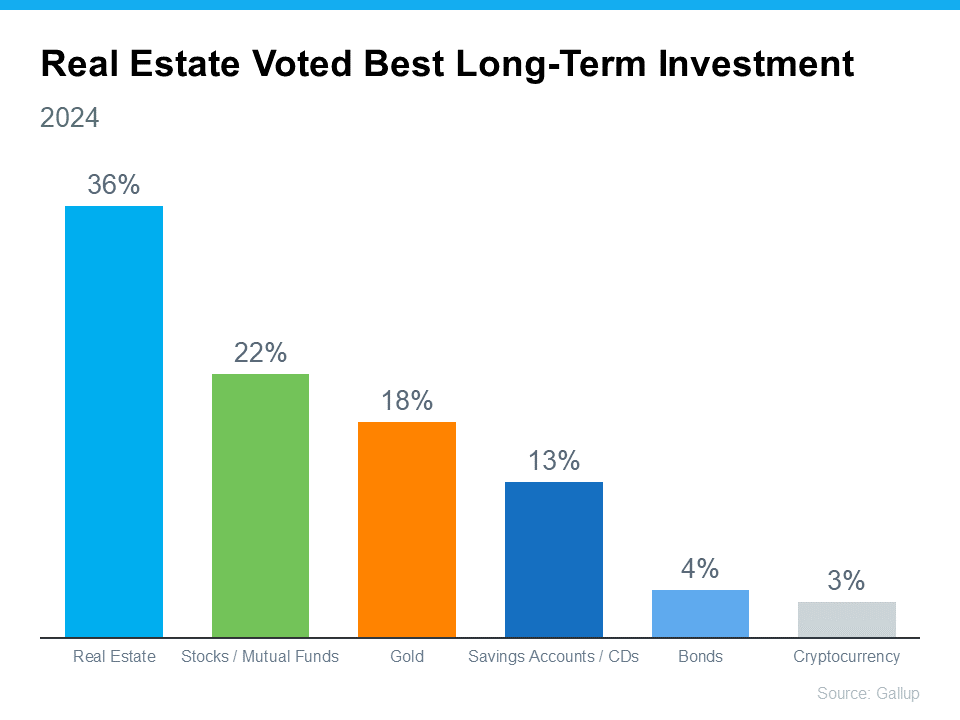

Real Estate Still Holds the Title of Best Long-Term Investment

Real Estate Still Holds the Title of Best Long-Term Investment

With all the headlines circulating about home prices and mortgage rates, you may be asking yourself if it still makes sense to buy a home right now, or if it’s better to keep renting. Here’s some information that could help put your mind at ease by showing that investing in a home is still a powerful decision.

According to the experts at Gallup, real estate has been crowned the top long-term investment for a whopping 12 years in a row. It has consistently beat out other investment types like gold, stocks, and bonds. Just take a look at the graph below – it speaks volumes:

But why does real estate continue to reign supreme as a top-notch long-term investment? It’s because, even today, buying a home can be your golden ticket to building wealth over time.

Unlike other investments that can feel a bit like riding a rollercoaster with all the ups and downs and ongoing risk factors, real estate follows a more predictable and positive pattern.

History shows home values usually rise. And while prices may vary by market, that means as time goes by, your house is likely to appreciate in value. And that helps you grow your net worth in a big way. As an article from Realtor.com explains:

“Homeownership has long been tied to building wealth—and for good reason. Instead of throwing rent money out the window each month, owning a home allows you to build home equity. And over time, equity can turn your mortgage debt into a sizeable asset.”

So, if you’re on the fence about whether to rent or buy, remember that real estate was consistently voted the best long-term investment for a reason. And if you want to get in on that action, it may make sense to go ahead and buy (if you’re ready and able).

Bottom Line

When it comes to building wealth that stands the test of time, real estate is the name of the game. If you’re ready to start on your own journey toward homeownership, let’s connect today.

The Difference Between an Inspection and an Appraisal

The Difference Between an Inspection and an Appraisal

When you decide to buy your first home, you may come across a number of terms and conditions you’re not familiar with. While you may have a general idea of what an inspection is, maybe you’re not sure why you need one or how it’s different from an appraisal. To keep it simple, here’s an explainer of each one and what they mean for you as a homebuyer.

Home Inspection

Once you’re under contract on a home you’d like to buy, getting an inspection is a key part of the process. An inspection gives you a clear idea of the safety and overall condition of the home – which is important for such a big transaction. As a recent Realtor.com article explains:

“A home inspection is something that protects your financial interest in what will likely be the largest purchase you make in your life—one in which you need as much information as possible.”

If anything is questionable in the inspection process – like the age of the roof, the state of the HVAC system, or just about anything else – you have the option to discuss and negotiate any potential issues or repairs with the seller before the transaction is final. And don’t worry – you don’t have to go through that process alone. Your real estate agent will be your advocate and negotiate with the seller for you.

Home Appraisal

While the inspection tells you about the current state of the house, an appraisal gives you its value. Bankrate explains:

“When buying or selling a home, an appraisal verifies that the sale price of the home is in line with fair market value. This ensures the homebuyer doesn’t pay more than the home is worth, and the mortgage lender doesn’t lend more than it is worth.”

Regardless of what you’re willing to pay for a house, if you’ll be using a mortgage to fund your purchase, the appraisal protects you from overpaying and the bank from lending you more than the home is worth.

And if there’s ever any confusion or discrepancy between the appraisal and the agreed-upon price in your contract, your trusted real estate professional will help you navigate any additional negotiations to try to close the gap.

Bottom Line

The inspection and the appraisal are different but equally important steps when buying a home – and you don’t need to manage them by yourself. Let’s connect today so you have expert guidance from start to finish.

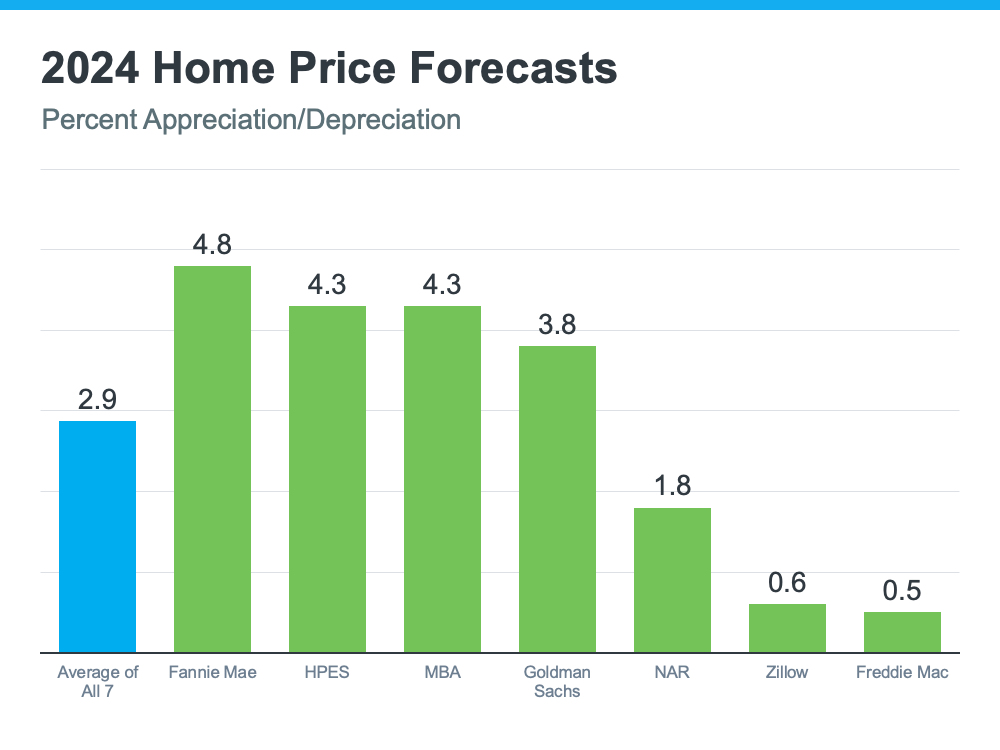

Housing Market Forecast: What’s Ahead for the 2nd Half of 2024

Housing Market Forecast: What’s Ahead for the 2nd Half of 2024

As we move into the second half of 2024, here’s what experts say you should expect for home prices, mortgage rates, and home sales.

Home Prices Are Expected To Climb Moderately

Home prices are forecasted to rise at a more normal pace. The graph below shows the latest forecasts from seven of the most trusted sources in the industry:

The reason for continued appreciation? The supply of homes for sale. Jessica Lautz, Deputy Chief Economist at the National Association of Realtors (NAR), explains:

“One thing that seems to be pretty solid is that home prices are going to continue to go up, and the reason is that we don’t have housing inventory.”

While inventory is up compared to the last couple of years, it’s still low overall. And because there still aren’t enough homes to go around, that’ll keep upward pressure on prices.

If you’re thinking of buying, the good news is you won’t have to deal with prices skyrocketing like they did during the pandemic. Just remember, prices aren’t expected to drop. They’ll continue climbing, just at a slower pace.

So, getting into the market sooner rather than later could still save you money in the long run. Plus, you can feel confident experts say your home will grow in value after you buy it.

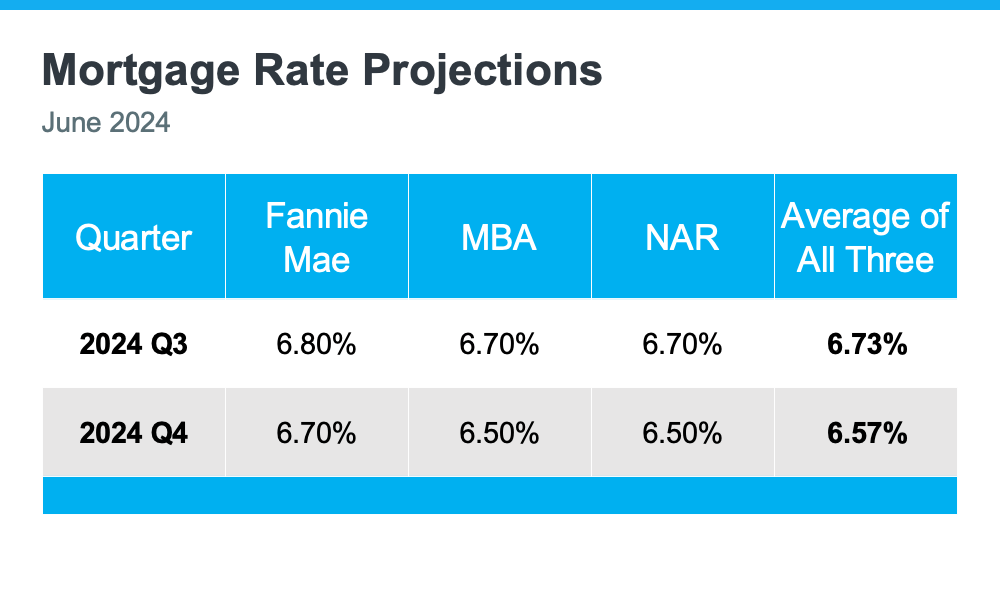

Mortgage Rates Are Forecast To Come Down Slightly

One of the best pieces of news for both buyers and sellers is that mortgage rates are expected to come down a bit, according to Fannie Mae, the Mortgage Bankers Association (MBA), and NAR (see chart below):

When you buy, even a small drop in mortgage rates can make a big difference in your monthly payments. For sellers, lower rates will bring more buyers back into the market, which can help you sell faster and potentially at a higher price. Plus, it may help you get off the fence, if you’ve been hesitant to sell due to today’s rates.

When you buy, even a small drop in mortgage rates can make a big difference in your monthly payments. For sellers, lower rates will bring more buyers back into the market, which can help you sell faster and potentially at a higher price. Plus, it may help you get off the fence, if you’ve been hesitant to sell due to today’s rates.

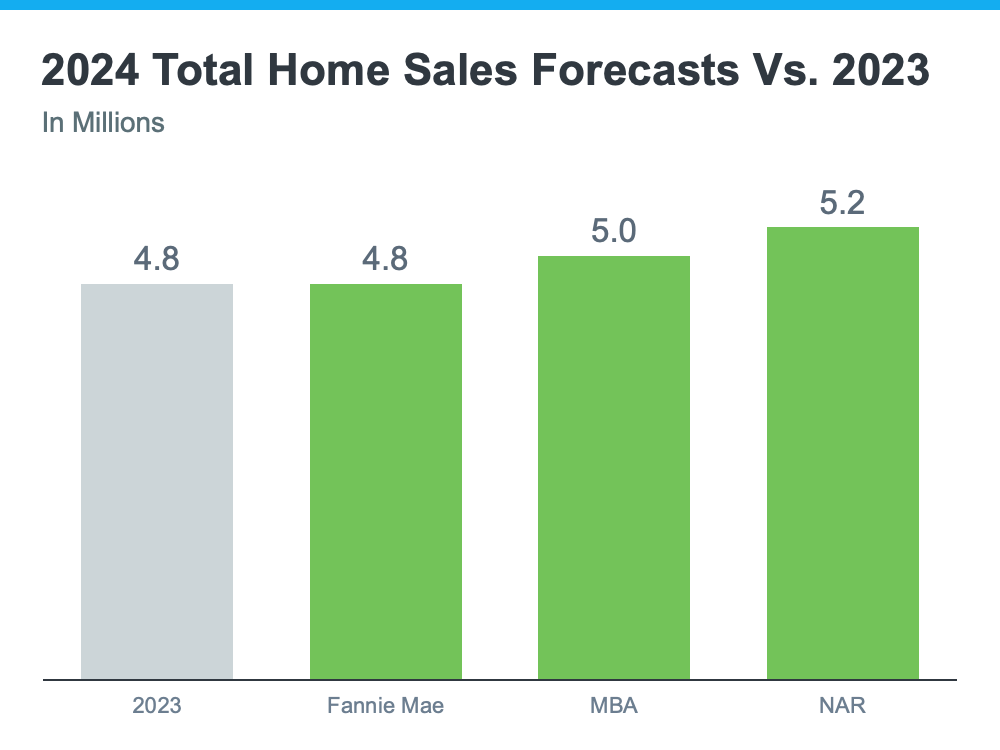

Home Sales Are Projected To Hold Steady

For 2024, the number of home sales will be about the same as last year and may even rise slightly. The graph below compares the 2024 home sales forecasts from Fannie Mae, MBA, and NAR to the 4.8 million homes that sold last year:

The average of the three forecasts is about 5 million sales in 2024 – a small increase from 2023. Lawrence Yun, Chief Economist at NAR, explains why:

“Job gains, steady mortgage rates and the release of inventory from pent-up home sellers will lead to more sales.”