| Tweet |

More Than a House: The Emotional Benefits of Homeownership

More Than a House: The Emotional Benefits of Homeownership

With all the headlines and talk about housing affordability, it can be tempting to get lost in the financial side of buying a home. That’s only natural as you think about the dollars and cents of it all.

And while you ultimately need to be able to afford a home you buy, don’t lose sight of why homeownership was so important to you in the first place. That’s because buying a home is so much more than just a financial transaction. As the National Association of Realtors (NAR) says:

“The benefits of purchasing and owning your place of residence are both financial and emotional – pride in homeownership and the feeling of security are huge intangible benefits.”

Here’s a look at just a few of those more emotional or lifestyle perks, to help anchor you to why homeownership is one of your goals.

A Sense of Satisfaction

Owning a home is often associated with better mental health and well-being. That’s probably because buying a home is a big milestone. And the sense of satisfaction and pride that comes with achieving that goal just feels good. A recent article from the Mortgage Reports says:

“By and large, homeownership brings more satisfaction than renting. . . Surveyees scored the overall happiness level of homeowners at 88% compared to 67% for renters.”

More Stability for Your Family

Another thing that may make homeowners feel more satisfied is that they’re finally able to put down roots. Think about it. If you’re used to moving each time your lease renews and your rent climbs, staying put for a while would be nice not just for you, but for any loved ones that live with you.

A home can provide more predictability and the chance to make long-term friends. That should reduce everyone’s stress too. As NAR explains:

“Families also benefit from homeownership, with studies proving that parents are able to spend less time in a stressed state, therefore spending more time with their children. The ability for parents to feel stable has a huge impact on children’s behavioral issues, educational success, and future economic success.”

A Stronger Feeling of Community

And if you’re also looking for a sense of belonging for yourself, homeownership can help with that too. As FinHabits says:

“Homeowners tend to be more involved in their local communities, leading to a stronger sense of belonging . . .”

It makes sense. Your home connects you to your neighborhood and, by extension, your broader community. That’s because owning a home gives you a stake in that community’s future. So, becoming more involved and wanting to do what you can to help improve the area while making long-term relationships with neighbors is only natural.

The Ability To Make the Space Your Own

And don’t forget, your home is a place that’s all yours. Unless you’ve got specific homeowner’s association requirements, you’re free to customize it however you see fit.

So, if renting has been cramping your style, it’s time to express yourself and jump on the latest trends (if you want to). Whether that’s small home improvements or full-on renovations, your house can be exactly what you want and need it to be. And as your tastes and lifestyle change, so can your home. Picture coming home each day to a place that feels like you. That’s a feeling like no other.

Bottom Line

If you want to enjoy a sense of accomplishment and pride in where you’re living, let’s have a conversation to go over what you need to do now to make this future happen for you.

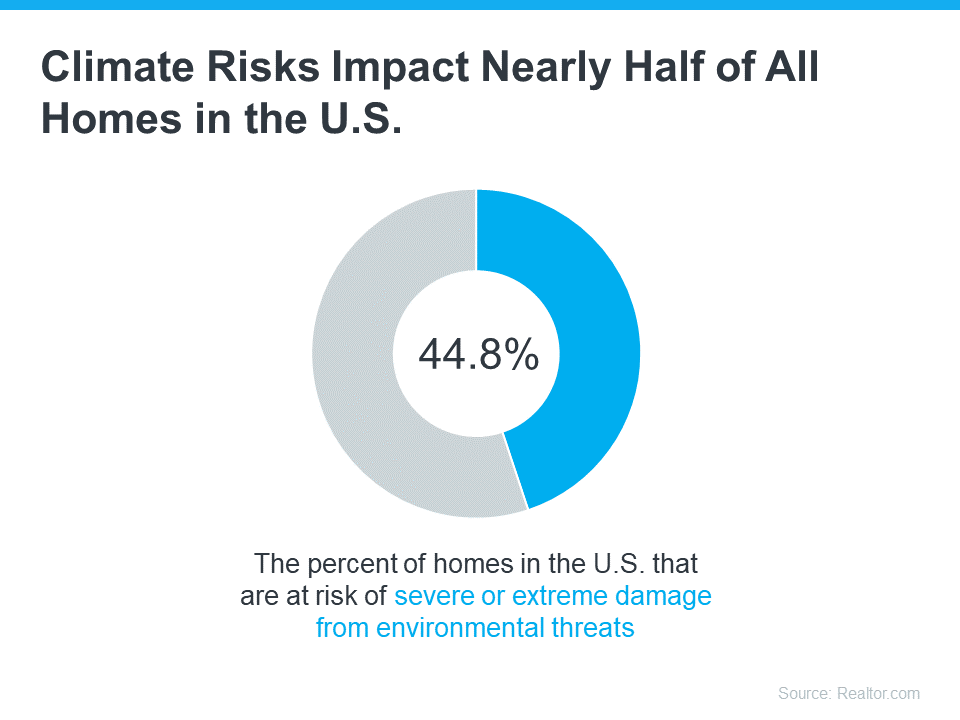

How Do Climate Risks Affect Your Next Home?

How Do Climate Risks Affect Your Next Home?

Climate change is impacting where people buy homes. As the experts at the National Association of Realtors (NAR) explain:

“Sixty-three percent of people who have moved since the pandemic began say they believe climate change is—or will be—an issue in the place they currently live.”

If you’re planning to move, climate change is something you might want to consider, no matter where you are. A recent study from Realtor.com helps put the growing impact climate change is having on real estate into perspective (see below):

So, how can you be sure your investment is safe from the elements?

For starters, work with a local real estate agent to understand the likelihood of your future home being exposed to hazards like wind, floods, and wildfires. Your agent will know the area and be able to tell you about the risks you’ll most likely face.

Beyond that, there are two important factors to think about: the quality of the home you want to buy and the insurance you’ll need to protect it.

A Home Built to Last

If you’re planning to be in your home for many years, you want to know it’s going to last. One way to think ahead is to work with your real estate agent to ensure the home you buy can withstand environmental hazards. They’re up to date on the most common building and remodeling techniques—like a secondary water barrier on the roof or noncombustible, fire-resistant exterior walls—used to protect homes from the effects of climate change.

And if the home you’re interested in doesn’t have the features you’re looking for, they can help you determine what you may be able to negotiate in the contract or what work it might require in the future.

Insurance To Protect It

Once you’re confident the home you’re looking at is well built, the next step is finding out what it’s going to take to insure it. As Selma Hepp, Chief Economist at CoreLogic, says:

“. . . homeowners are going to become increasingly more aware of risks of living in some areas as it becomes prohibitively expensive or very difficult to obtain hazard insurance.”

In areas where climate risks are having a bigger impact, the right home insurance can make a big difference. And the price of that insurance is an important factor when thinking about your budget and the true cost of buying and protecting your home. Get an insurance quote early in the process because you may want to compare multiple quotes and it can take several weeks to get them.

While this may feel like a lot to consider, don’t worry. An agent can help. Your real estate agent will be your go-to resource on the homebuying process, what to look for and consider, and how climate change may affect your next home. With the right planning and an agent’s expert advice, you can make this happen. Homeownership is worth it. And with a great agent by your side, you can make sure the home you find is the right fit.

Bottom Line

Climate change is an important factor to think about when buying a home. After all, your home is a huge investment, and you want to be ready for anything that might affect it. Let’s chat so you can find the perfect home.

How VA Loans Can Help You Buy a Home

How VA Loans Can Help You Buy a Home

For over 80 years, Veterans Affairs (VA) home loans have helped millions of veterans buy their own homes. If you or someone you know has served in the military, it’s important to learn about this program and its benefits.

Here are some key things to know about VA loans before buying a home.

Top Benefits of VA Home Loans

VA home loans make it easier for veterans to buy a home, and they’re a great perk for those who qualify. According to the Department of Veteran Affairs, some benefits include:

- Options for No Down Payment: Qualified borrowers can often purchase a home with no down payment. That’s a huge weight lifted when you’re trying to save for a home. The Associated Press says:

“. . . about 90% of VA loans are used to purchase a home with no money down.”

- Don’t Require Private Mortgage Insurance (PMI): Many other loans with down payments under 20% require PMI. VA loans do not, which means veterans can save on their monthly housing costs.

- Limited Closing Costs: There are limits on the types of closing costs you pay when you qualify for a VA home loan. So, more money stays in your pocket when it’s time to seal the deal.

An article from Veterans United sums up how remarkable this loan can be:

“For the vast majority of military borrowers, VA loans represent the most powerful lending program on the market. These flexible, $0-down payment mortgages have helped more than 24 million service members become homeowners since 1944.”

Bottom Line

Owning a home is the American Dream. Veterans give a lot to protect our country, and one way to honor them is by making sure they know about VA home loans.

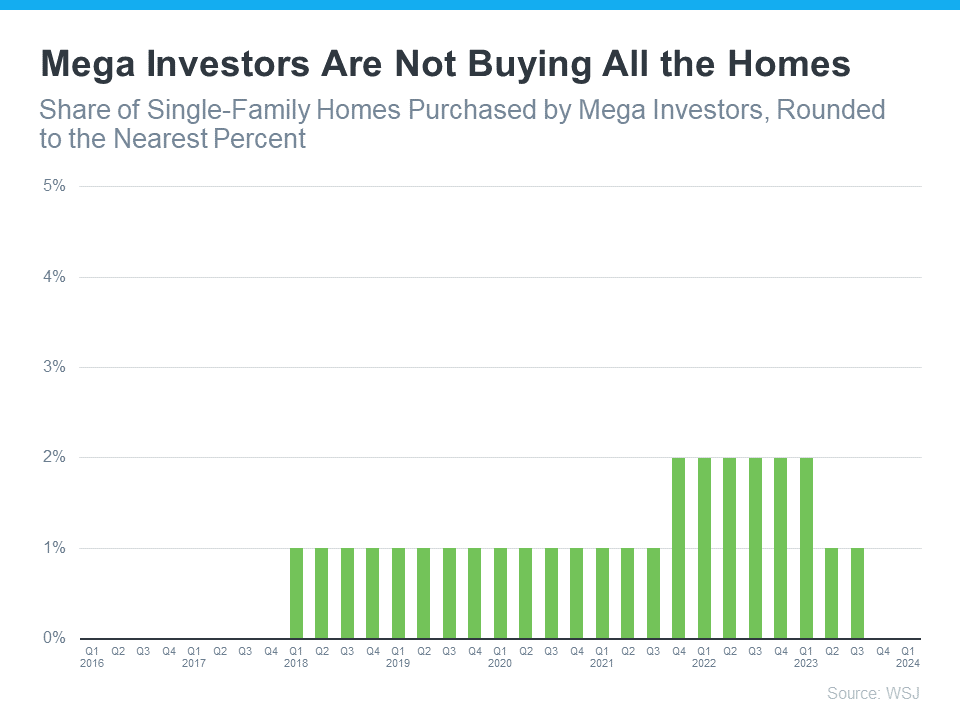

How Many Homes Are Investors Actually Buying?

How Many Homes Are Investors Actually Buying?

Are big investors really buying up all the homes today?

If you’re trying to find a house to buy, this may be something you’re wondering about. Maybe you’ve read about it or seen reels on social media saying investors buying all the homes is making it even harder to find what the average buyer is looking for. But spoiler alert – there’s a lot of misinformation out there. To clear things up, here’s the scoop on what’s really happening. A lot of the big investor activity is actually in the rearview mirror already.

The Wall Street Journal (WSJ) explains:

“Investors of all sizes spent billions of dollars buying homes during the pandemic. At the 2022 peak, they bought more than one in every four single-family homes sold, though more recently their activity has slowed as interest rates rose and supply became tighter.”

The key here is investor activity has slowed significantly, and even during the peak of investor buying, 3 out of every 4 single-family homes purchased were by regular, everyday buyers – not investors. And of the investors who bought over the past few years, most weren’t the big investors you may be hearing about. The vast majority were small mom-and-pop investors – people like your neighbors who own only a couple of homes, maybe even just their main residence and a vacation home.

But let’s focus on the giant, mega-investor firms since that’s what is being talked about so frequently on social media right now. Mega investors are those who own 1,000+ properties. You may be surprised to see that, according to the Wall Street Journal, they don’t buy all that many homes (see graph below):

This graph tells us two things. First, institutional investors were never buying a large percentage of available homes. During the peak in 2022, they bought about 2% of available single-family homes. Second, that percentage has gotten even smaller recently (so small the number rounds down to 0%).

In an effort to understand why that percentage is trending down, private lender RCN Capital asked investors about the challenges they’re facing. Here’s what Jeffrey Tesch, CEO of RCN Capital, found out:

“Investors are already facing many challenges in today’s housing market – rising prices, limited inventory, and higher financing costs.”

Understanding these challenges is important because they show big, mega investors aren’t taking over the housing market.

So, don’t fall for everything you hear. They aren’t snatching up all the homes and making it impossible for regular people to buy.

Bottom Line

Big investors aren’t buying all the homes out there. If you’ve got questions about what you’re hearing about the housing market, let’s chat. I can help you understand what’s really going on.

The Biggest Mistakes Buyers Are Making Today

The Biggest Mistakes Buyers Are Making Today

Buyers face challenges in any market – and today’s is no different. With higher mortgage rates and rising prices, plus the limited supply of homes for sale, there’s a lot to consider.

But, there’s one way to avoid getting tripped up – and that’s leaning on a real estate agent for the best possible advice. An expert’s insights will help you avoid some of the most common mistakes homebuyers are making right now.

Putting Off Pre-approval

As part of the homebuying process, a lender will look at your finances to figure out what they’re willing to loan you for your mortgage. This gives you a good idea of what you can borrow so you can really wrap your head around the financial side of things before you start looking at homes. While house hunting can be a lot more fun than talking about finances, you don’t want to do this out of order. Make sure you get your pre-approval first. As CNET explains:

“If you wait to get preapproved until the last minute, you might be scrambling to contact a lender and miss the opportunity to put a bid on a home.”

Holding Out for Perfection

While you may have a long list of must-haves and nice-to-haves, you need to be realistic about your home search. Even though your ideal state is you find a home that checks every box, you may need to be willing to compromise – especially since inventory is still low. Plus, a home that has everything you want may be too pricey. As Investopedia puts it:

“When you expect to find the perfect home, you could prolong the homebuying process by holding out for something better. Or you could end up paying more for a home just because it meets all your needs.”

Instead, look for something that has most of your must-haves and good bones where you can add anything else you may need down the line.

Buying More House Than You Can Afford

With today’s mortgage rates and home prices, there’s no arguing it’s expensive to buy a home. And while it may be tempting to stretch your finances a bit further than you’re comfortable with to make sure you get the house, you want to avoid overextending your budget. Make sure you talk to your agent about how changing mortgage rates impact your monthly payment. Bankrate offers this advice:

“Focus on what monthly payment you can afford rather than fixating on the maximum loan amount you qualify for. Just because you can qualify for a $300,000 loan doesn’t mean you can comfortably handle the monthly payments that come with it along with your other financial obligations. Every borrower’s case is different, so factor in your whole financial profile when determining how much house you can afford.”

Not Working with a Local Real Estate Agent

This last one may be the most important of all. Buying a home is a process that involves a lot of steps, paperwork, negotiation, and more. Rather than take all of this on yourself, it’s a good idea to have a pro working with you. The right agent will reduce your stress and help the process go smoothly. As CNET explains:

“Attempting to buy a home without a real estate agent makes the process more arduous than it needs to be. A real estate agent can give you professional legal guidance, market expertise and support, which will save you time, money and stress. They can also increase your chances of finding the right home so you don’t have to spend hours scouring the internet for listings.”

Bottom Line

Mistakes can cost you time, frustration, and money. If you want to buy a home in today’s market, let’s connect so you have a pro on your side who can help you avoid these missteps.

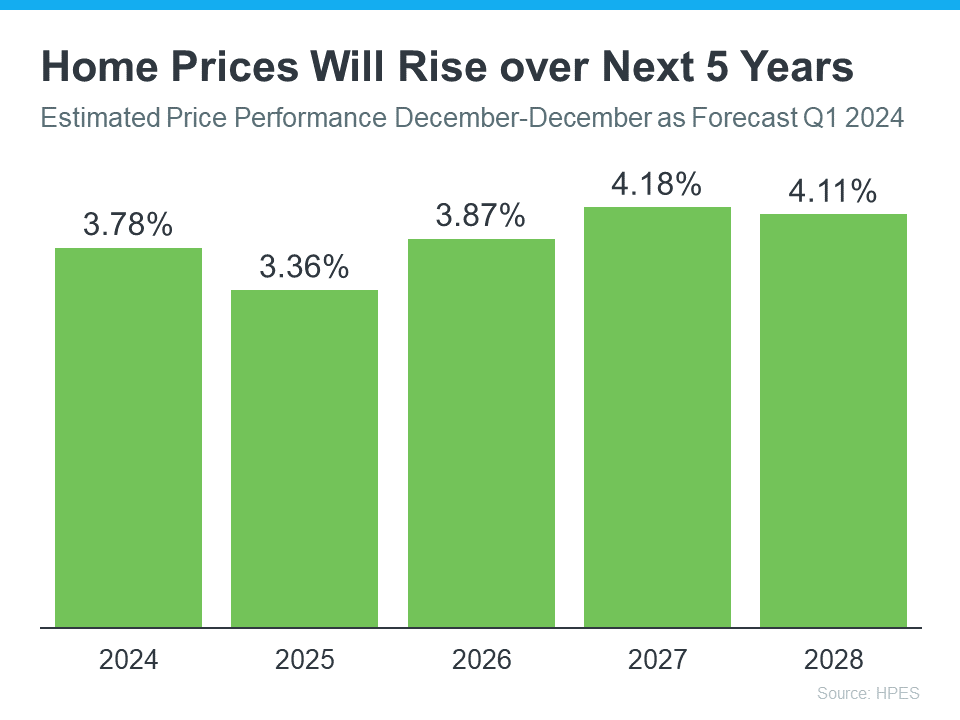

What’s Next for Home Prices and Mortgage Rates?

What’s Next for Home Prices and Mortgage Rates?

If you’re thinking of making a move this year, there are two housing market factors that are probably on your mind: home prices and mortgage rates. You’re wondering what’s going to happen next. And if it’s worth it to move now, or better to wait it out.

The only thing you can really do is make the best decision you can based on the latest information available. So, here’s what experts are saying about both prices and rates.

1. What’s Next for Home Prices?

One reliable place you can turn to for information on home price forecasts is the Home Price Expectations Survey from Fannie Mae – a survey of over one hundred economists, real estate experts, and investment and market strategists.

According to the most recent release, experts are projecting home prices will continue to rise at least through 2028 (see the graph below):

While the percent of appreciation varies year-to-year, this survey says we’ll see prices rise (not fall) for at least the next 5 years, and at a much more normal pace.

What does that mean for your move? If you buy now, your home will likely grow in value and you should gain equity in the years ahead. But, based on these forecasts, if you wait and prices continue to climb, the price of a home will only be higher later on.

2. When Will Mortgage Rates Come Down?

This is the million-dollar question in the industry. And there’s no easy way to answer it. That’s because there are a number of factors that are contributing to the volatile mortgage rate environment we’re in. Odeta Kushi, Deputy Chief Economist at First American, explains:

“Every month brings a new set of inflation and labor data that can influence the direction of mortgage rates. Ongoing inflation deceleration, a slowing economy and even geopolitical uncertainty can contribute to lower mortgage rates. On the other hand, data that signals upside risk to inflation may result in higher rates.”

What happens next will depend on where each of those factors goes from here. Experts are optimistic rates should still come down later this year, but acknowledge changing economic indicators will continue to have an impact. As a CNET article says:

“Though mortgage rates could still go down later in the year, housing market predictions change regularly in response to economic data, geopolitical events and more.”

So, if you’re ready, willing, and able to afford a home right now, partner with a trusted real estate advisor to weigh your options and decide what’s right for you.

Bottom Line

Let’s connect to make sure you have the latest information available on home prices and mortgage rate expectations. Together we’ll go over what the experts are saying so you can make an informed decision on your move.

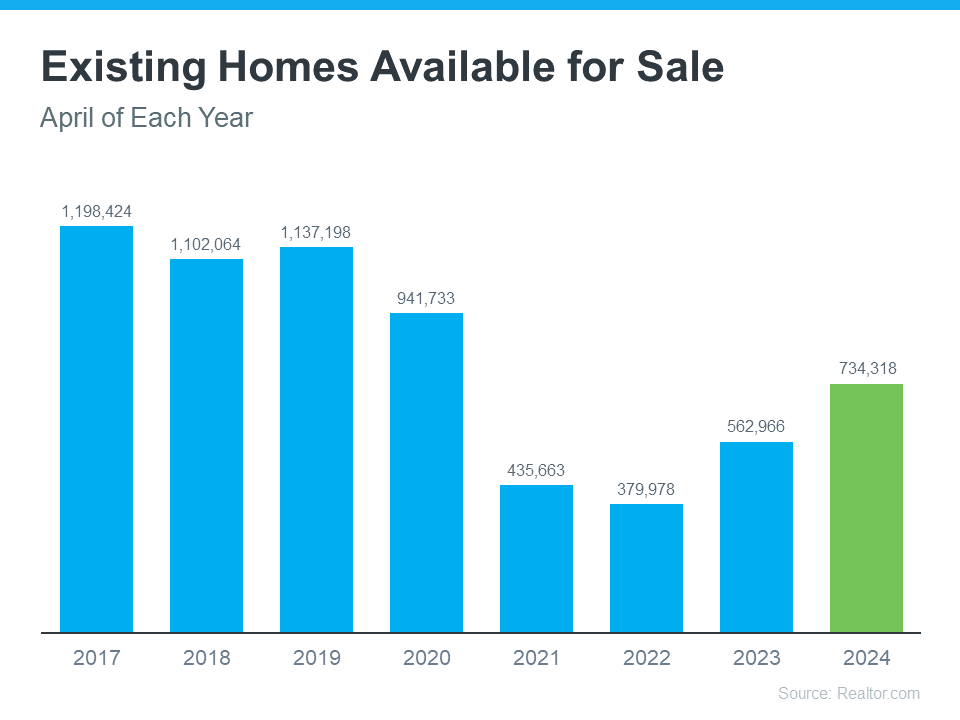

The Number of Homes for Sale Is Increasing

The Number of Homes for Sale Is Increasing

There’s no denying the last couple of years have been tough for anyone trying to buy a home because there haven’t been enough houses to go around. But things are starting to look up.

There are more homes up for grabs this year. The graph below uses the latest data from Realtor.com to show in April 2024 there were more homes for sale than there were over the last few years (2021-2023):

As Realtor.com explains:

“There were 30.4% more homes actively for sale on a typical day in April compared with the same time in 2023, marking the sixth consecutive month of annual inventory growth.”

But does this growing inventory make house hunting easier? Yes and no.

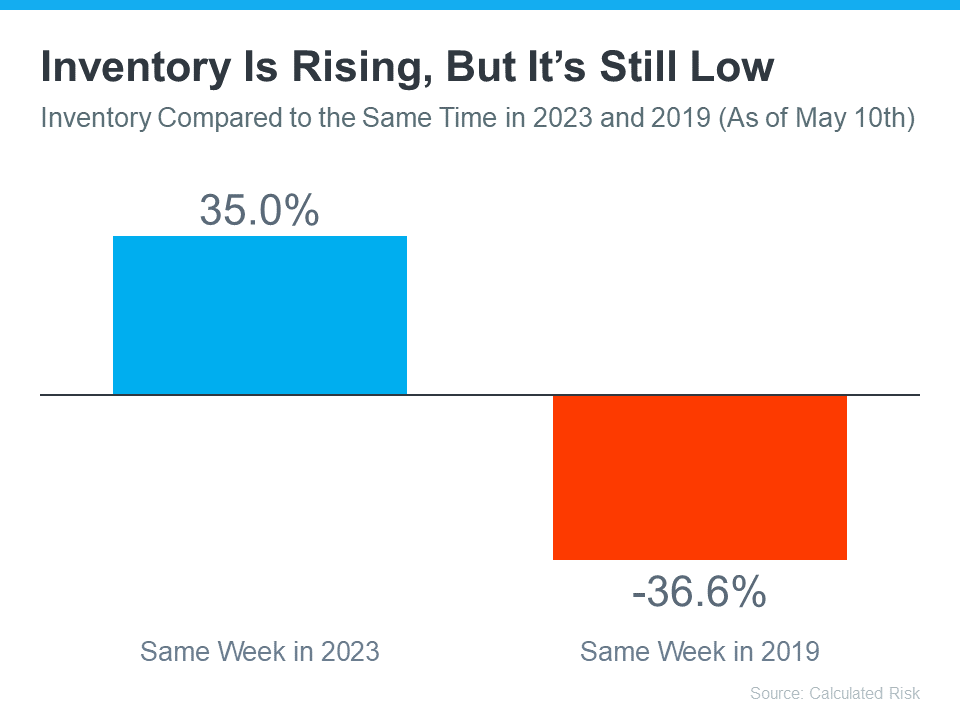

Using the latest weekly data from Calculated Risk, the graph below shows, that even with the growth lately, there are still way fewer homes for sale than there were in the last normal year in the housing market:

What Does This Mean for You?

If you’ve been looking to buy but put your plans on hold because you just couldn’t find what you were searching for, you might see more options now than you did over the past few years – but don’t expect a huge selection.

To check out your growing options, it’s a good idea to work with a local real estate agent you trust. Real estate is all about location. And an agent can help you get the scoop on the homes available in the area you’re interested in. Bankrate explains:

“In today’s homebuying market, it’s more important than ever to find a real estate agent who really knows your local area — down to your specific neighborhood — and can help you successfully navigate its unique quirks.”

Bottom Line

Let’s team up so you have someone who can keep you in the loop on everything that might impact your move, like how many homes are up for sale right now.

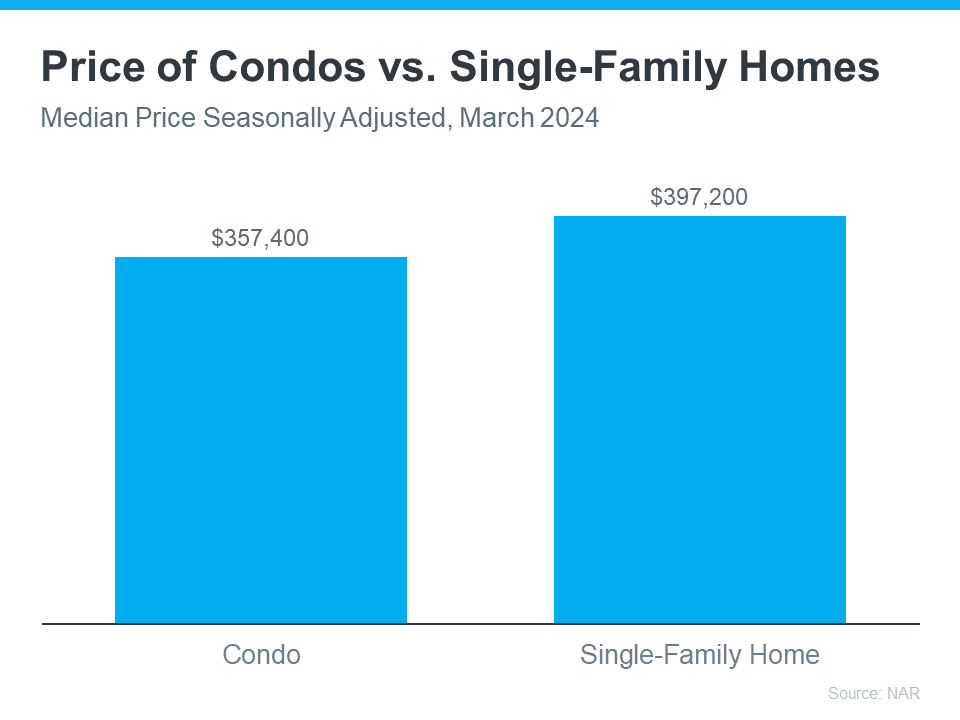

Why a Condo May Be a Great Option for Your First Home

Why a Condo May Be a Great Option for Your First Home

Having a hard time finding a first home that’s right for you and your wallet? Well, here’s a tip – think about condominiums, or condos for short.

They’re usually smaller than single-family homes, but that’s exactly why they can be easier on your budget. According to the latest data from the National Association of Realtors (NAR), condos are typically less expensive than single-family homes (see graph below):

So, if you’re comfortable with a smaller space and want to buy your first home this year, adding condos to your search might be easier on your wallet.

Besides giving you more options for your home search and maybe fitting your budget better, living in a condo has a bunch of other perks, too. According to Rocket Mortgage:

“From community living to walkable urban areas, condos are great options for first-time home buyers and people looking to enjoy homeownership without extensive upkeep.”

Let’s dive into a few of the draws of condos for first-time buyers from Bankrate:

- They require less maintenance. Condos are great if you want to own your place but don’t want to mow the lawn, shovel snow, or fix the roof. Your real estate agent can help explain any associated fees and details for the condos you’re interested in.

- They allow you to start building equity. When you buy a condo, you build equity and your net worth as you make your mortgage payments and as your condo’s value goes up over time.

- They often come with added amenities. Your condo might come with access to amenities like a pool, dog park, or parking. And the best part? You don’t have to take care of any of them.

- They provide you with a sense of community. Buying a condo means you’ll be living close to other people, which is nice if you enjoy having neighbors around and making friends. Many condo communities hold fun events like barbecues and parties during holidays for everyone to enjoy.

Remember, your first home doesn’t have to be the one you stay in forever. The important thing is to get your foot in the door as a homeowner so you can start to gain home equity. Later on, that equity can help you buy another place if you need something different.

Ultimately, owning and living in a condo is a lifestyle choice. And if it’s one that appeals to you, they could provide the added options you need in today’s market.

Bottom Line

It might be a good idea to think about condos in your home search. If you’re ready to see what’s out there, let’s get in touch today.

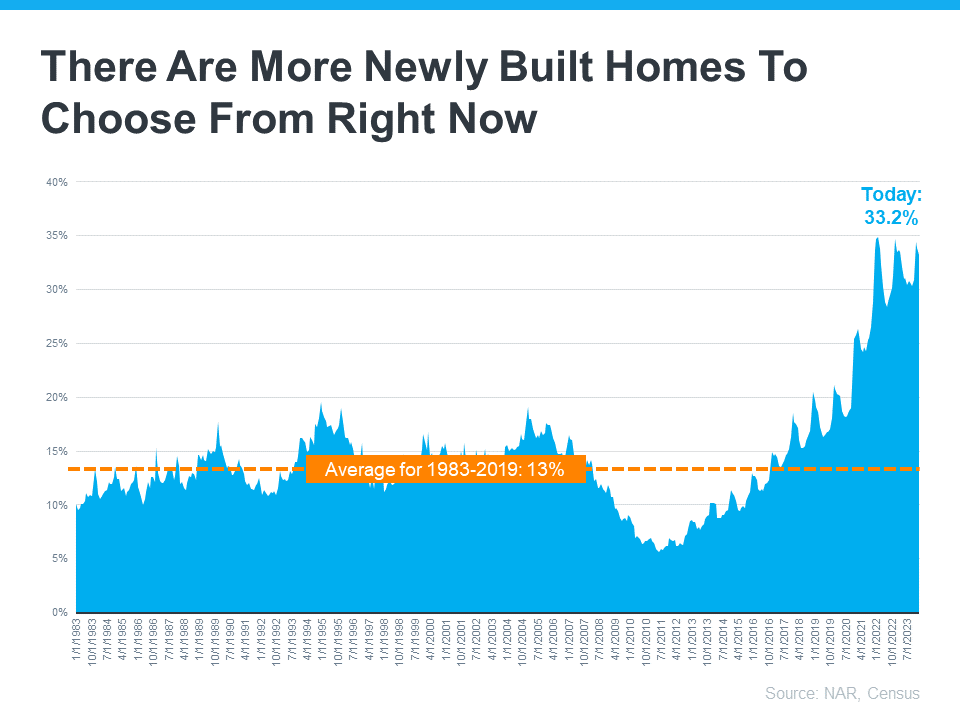

The Top 2 Reasons To Consider a Newly Built Home

The Top 2 Reasons To Consider a Newly Built Home

When you’re planning a move, it’s normal to wonder where you’ll end up and what your future home is going to look like. Maybe you’ve got a specific picture of that house in your mind. But unless you came into this process knowing you want to buy a newly built home, you may not have pictured new home construction.

A trusted real estate agent can help walk you through these two reasons you may want to reconsider that.

1. Adding Newly Built Homes Could Give You More Options

There are two types of homes on the market: new and existing. A newly built home refers to a house that was just built or is under construction. An existing home is one a previous homeowner has already lived in. Right now, the inventory of existing homes is tight. But there may be options for you on the new home side of things.

Data from the Census and the National Association of Realtors (NAR) shows that newly built homes are a bigger part of today’s housing inventory than the norm (see graph below):

From 1983 to 2019 (the last normal year in the market), newly built homes made up only 13% of the total inventory of homes for sale. But today that number has climbed to over 33%.

Rest assured, after over a decade of underbuilding, builders aren’t overdoing it today. Even with an increase in new construction today, there’s still a significant housing shortage overall. But for you, the uptick in new builds can be a game changer because it gives you more options for your search.

2. Newly Built Homes May Be More Affordable Than You’d Think

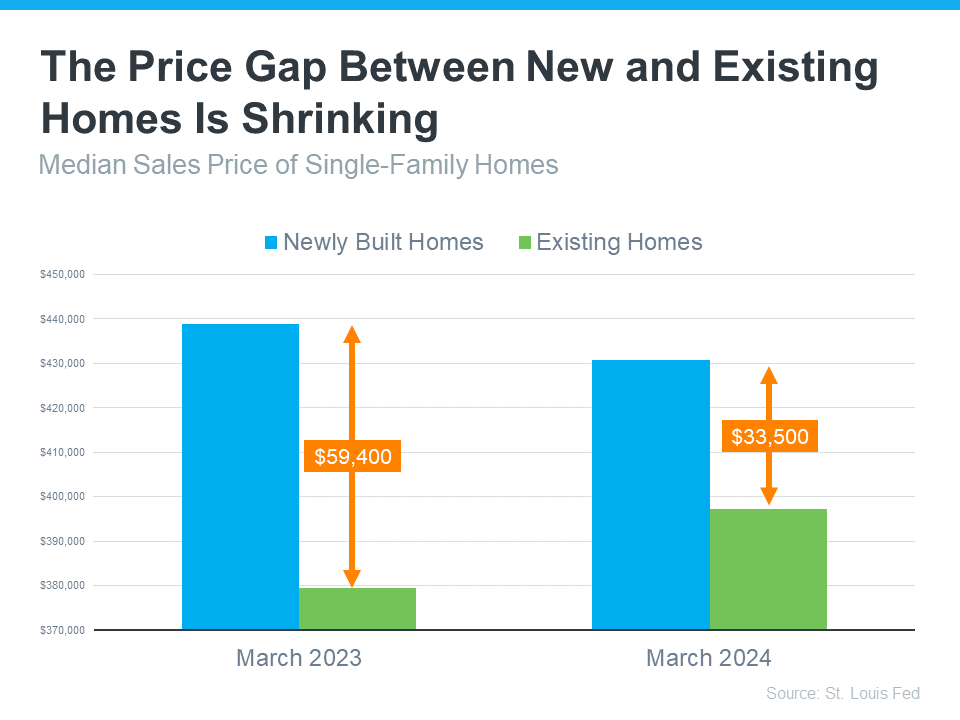

You may still be wondering if a new build could really be an option for you. If you’ve previously written them off because you thought they would be out of your budget, consider this. The price gap between a newly built home and an existing house is shrinking. Here’s why.

Builders are going to build what’s in demand. And they know people need more options right now, especially ones that are smaller and potentially more affordable. So, they’re focusing on building smaller homes at lower price points. The graph below shows the price difference between new and existing homes is shrinking as that happens:

As LendingTree explains:

“In the past, newly built homes have been much more expensive than existing homes — but that gap has been getting smaller recently. In some places today, you may find that the cost to build versus buy is roughly the same.”

And an article from CNBC says:

“While new builds are still sold for slightly more than existing homes, the price gap has significantly narrowed . . .”

Not to mention, some builders are even offering price cuts and mortgage rate buy-downs right now to sweeten the deal. Today there are many reasons new builds may be worth considering. Other buyers sure seem to think so. As Freddie Mac says:

“As the supply of existing homes for sale remains low and home prices continue to rise, more buyers are choosing to purchase new homes than in previous years.”

Just know that buying a newly built home isn’t the same as buying an existing one. Builder contracts have different fine print. So, partner with a local agent who knows the market, builder reputations, and what to look for in those contracts so you have an expert on your side to help you explore this option.

Bottom Line

If you want to find out what builders are doing in our area, let’s connect and check it out together. And if you’re willing to cast a wider net to open up your options even more, we can talk about broadening your search to include other towns nearby.

How Buying or Selling a Home Benefits Your Community

How Buying or Selling a Home Benefits Your Community

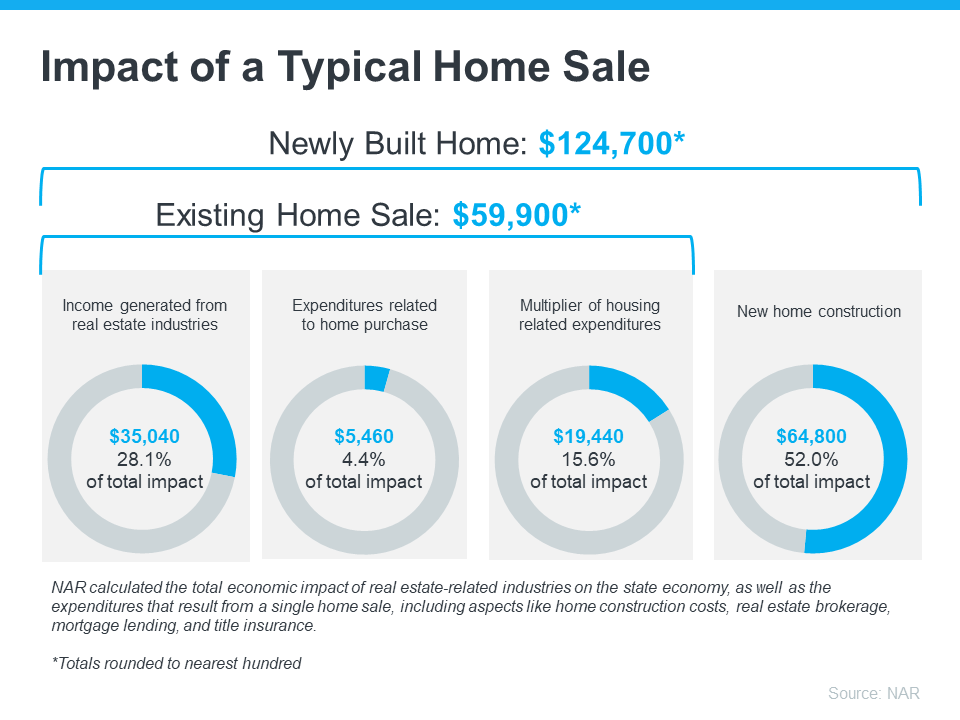

If you’re thinking of buying or selling a house, it’s important to know it doesn’t just impact you—it helps out the local economy and your community, too.

Every year, the National Association of Realtors (NAR) puts out a report that breaks down the financial impact that comes from people buying and selling homes (see visual below):

When a house is sold, it really boosts the local economy. That’s because of all the people needed to build, fix up, and sell homes. Robert Dietz, Chief Economist at the National Association of Home Builders (NAHB), explains how the housing industry adds jobs to a community:

“. . . housing is a significant job creator. In fact, for every single-family home built, enough economic activity is generated to sustain three full-time jobs for a year . . .”

It makes sense that housing creates a lot of jobs because so many different kinds of work are involved in the industry.

Think about all the people involved with selling a house—city officials, contractors, lawyers, real estate agents, specialists, etc. Everyone has a job to do to make your deal go through. So, each transaction is a big help to those who work and live in your community.

Put simply, when you buy or sell a home, you’re helping out your neighbors. So, when you decide to move, you’re not just meeting your own needs—you’re also doing something good for your community. Just knowing your move helps so many people around you can give you a sense of empowerment as you make your decision this year.

Bottom Line

Every time a home is sold, it really helps out the local economy. If you’re ready to move, let’s get in touch. It won’t just change your life—it’ll also do a lot of good for the whole community.

Tips for Younger Homebuyers: How To Make Your Dream a Reality

Tips for Younger Homebuyers: How To Make Your Dream a Reality

If you’re a member of a younger generation, like Gen Z, you may be asking the question: will I ever be able to buy a home? And chances are, you’re worried that’s not going to be in the cards with inflation, rising home prices, mortgage rates, and more seemingly stacked against you.

While there’s no arguing this housing market is challenging for first-time homebuyers, it is still achievable, especially if you have professionals on your side.

Here are some helpful tips you may get from a pro.

1. Explore Your Options for a Down Payment

If a down payment is your #1 hurdle, you may have options to give your savings a boost. There are over 2,000 down payment assistance programs designed to make homeownership more achievable. And, that’s not the only place you may be able to get a helping hand. While it may not be an option for everyone, 49% of Gen Z homebuyers got money from loved ones that they used toward a down payment, according to LendingTree.

And chances are you won’t need to put 20% down (unless specified by your loan type or lender). So be sure to work with a trusted mortgage professional to explore your options, find out how much you’ll really need, and learn about any guidelines on getting a gift from loved ones.

2. Live with Loved Ones To Boost Your Savings

Another thing a number of Gen Z buyers are doing is ditching their rental and moving back in with friends or family. This can help cut down your housing costs so you can build your savings a whole lot faster. As Bankrate explains:

“. . . many have opted to stop renting and live with family in order to boost their savings. Thirty percent of Gen Z homebuyers move directly from their family member’s home to a home of their own, according to NAR.”

3. Cast a Broad Net for Your Search

When you’ve saved up enough, here’s how a pro will help you approach your search. Since the supply of homes for sale is still low and affordability is tight, they’ll give you strategies and avenues you may not have considered to open up your pool of options.

For example, it’s usually more affordable if you consider a rural or suburban area versus an urban one. So, while the city may be livelier and more energetic, the cost of living may be reason enough to look at something further out. And if you consider smaller homes and condos or townhouses, you’ll give yourself even more ways to break into the market. As Colby Stout, Research Analyst at Bright MLS, explains:

“Being flexible on the types of home (e.g., a condo or townhome versus a single-family home) and exploring more affordable neighborhoods is important for first-time buyers.”

4. Take a Close Look at Your Wants and Needs

And lastly, an agent can help you really think about your must-have’s and nice-to-have’s. Remember, your first home doesn’t have to be your forever home. You just need to get your foot in the door to start building equity. If you want to buy, you may find making some compromises is worth it. As Chase says:

“An open-minded approach to house-hunting may be one way for Gen Z homebuyers to maintain some edge. This could mean buying in areas that are less expensive. Differentiating needs vs. wants may help in this area as well.”

An agent will help you prioritize your list of home features and find houses that can deliver on the top ones. And they’ll be able to explain how equity can benefit you in the long run and make it possible to move into that dream home down the line.

Bottom Line

Real estate professionals have expertise on what’s working for other buyers like you. Lean on them for tips and advice along the way. As Directors Mortgage says, with that support you can make it happen:

“The path to homeownership may not be a straightforward one for Gen Z, but it’s undoubtedly within reach. By adopting the right strategies, like exploring down payment assistance programs and sharing living costs with relatives, you can bring your dream of owning a home closer to reality.”

Let’s connect to get you set up for long-term success.

What Is Going on with Mortgage Rates?

What Is Going on with Mortgage Rates?

You may have heard mortgage rates are going to stay a bit higher for longer than originally expected. And if you’re wondering why, the answer lies in the latest economic data. Here’s a quick overview of what’s happening with mortgage rates and what experts say is ahead.

Economic Factors That Impact Mortgage Rates

When it comes to mortgage rates, things like the job market, the pace of inflation, consumer spending, geopolitical uncertainty, and more all have an impact. Another factor at play is the Federal Reserve (the Fed) and its decisions on monetary policy. And that’s what you may be hearing a lot about right now. Here’s why.

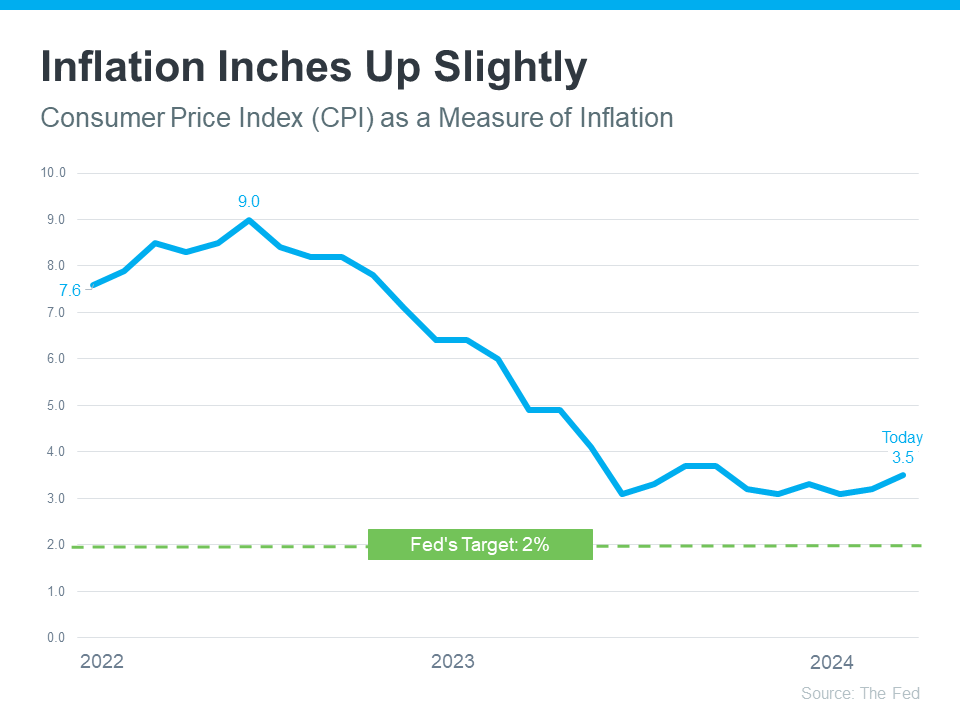

The Fed decided to start raising the Federal Funds Rate to try to slow down the economy (and inflation) in early 2022. That rate impacts how much it costs banks to borrow money from each other. It doesn’t determine mortgage rates, but mortgage rates do respond when this happens. And that’s when mortgage rates started to really climb.

And while there’s been a ton of headway seeing inflation come down since then, it still isn’t back to where the Fed wants it to be (2%). The graph below shows inflation since the spike in early 2022, and where we are now compared to their target rate:

As the graph shows, we’re much closer to their goal of 2% inflation than we were in 2022 – but we’re not there yet. It’s even inched up a hair over the last 3 months – and that’s having an impact on the Fed’s plans. As Sam Khater, Chief Economist at Freddie Mac, explains:

“Strong incoming economic and inflation data has caused the market to re-evaluate the path of monetary policy, leading to higher mortgage rates.”

Basically, long story short, inflation and its impact on the broader economy are going to be key moving forward. As Greg McBride, Chief Financial Analyst at Bankrate, says:

“It’s the longer-term outlook for economic growth and inflation that have the greatest bearing on the level and direction of mortgage rates. Inflation, inflation, inflation — that’s really the hub on the wheel.”

When Will Mortgage Rates Come Down?

Based on current market data, experts think inflation will be more under control and we still may see the Fed lower the Federal Funds Rate this year. It’ll just be later than originally expected. As Mike Fratantoni, Chief Economist at the Mortgage Bankers Association (MBA), said in response to the Federal Open Market Committee (FOMC) decision yesterday:

“The FOMC did not change the federal funds target at its May meeting, as incoming data regarding the strength of the economy and stubbornly high inflation have resulted in a shift in the timing of a first rate cut. We expect mortgage rates to drop later this year, but not as far or as fast as we previously had predicted.”

In the simplest sense, what this says is that mortgage rates should still come down later this year. But timing can shift as new employment and economic data come in, geopolitical uncertainty remains, and more. This is one of the reasons it’s usually not a good strategy to try to time the market. An article in Bankrate gives buyers this advice:

“ . . . trying to time the market is generally a bad idea. If buying a house is the right move for you now, don’t stress about trends or economic outlooks.”

Bottom Line

If you have questions about what’s happening in the housing market and what that means for you, let’s connect.

The Perks of Buying over Renting

The Perks of Buying over Renting

Thinking about buying a home? While today’s mortgage rates might seem a bit intimidating, here are two solid reasons why, if you’re ready and able, it could still be a smart move to get your own place.

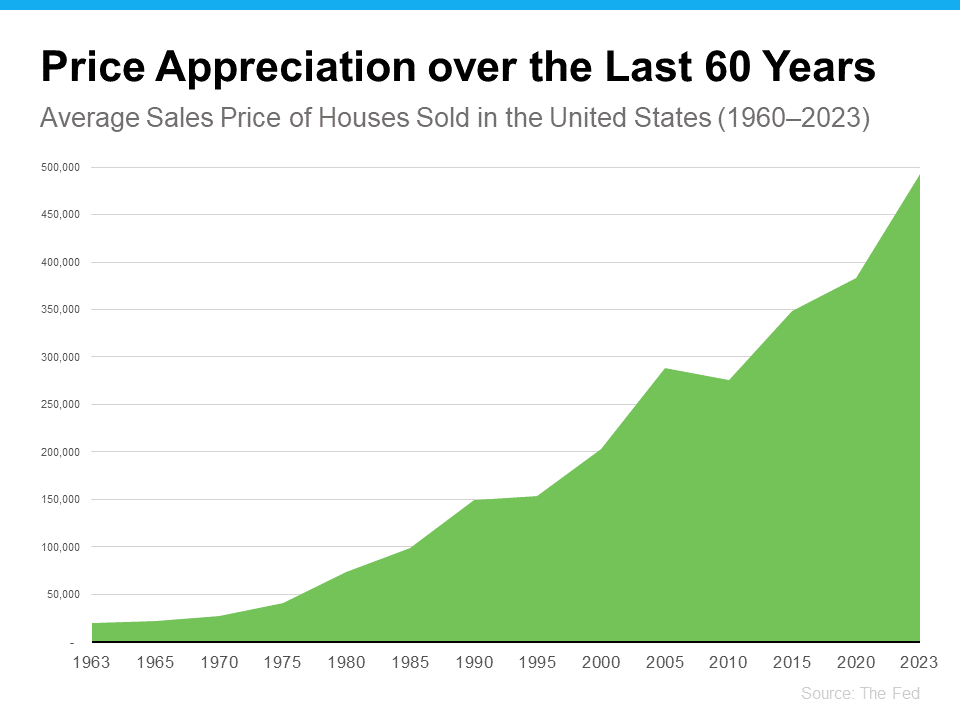

1. Home Values Typically Go Up Over Time

There’s been some confusion over the past year or so about which way home prices are headed. Make no mistake, nationally they’re still going up. In fact, over the long-term, home prices almost always go up (see graph below):

Using data from the Federal Reserve (the Fed), you can see the overall trend is home prices have climbed steadily for the past 60 years. There was an exception during the 2008 housing crash when prices didn’t follow the normal pattern, but generally, home values kept rising.

This is a big reason why buying a home can be better than renting. As prices go up and you pay down your mortgage, you build equity. Over time, this growing equity can really increase your net worth. The Urban Institute says:

“Homeownership is critical for wealth building and financial stability.”

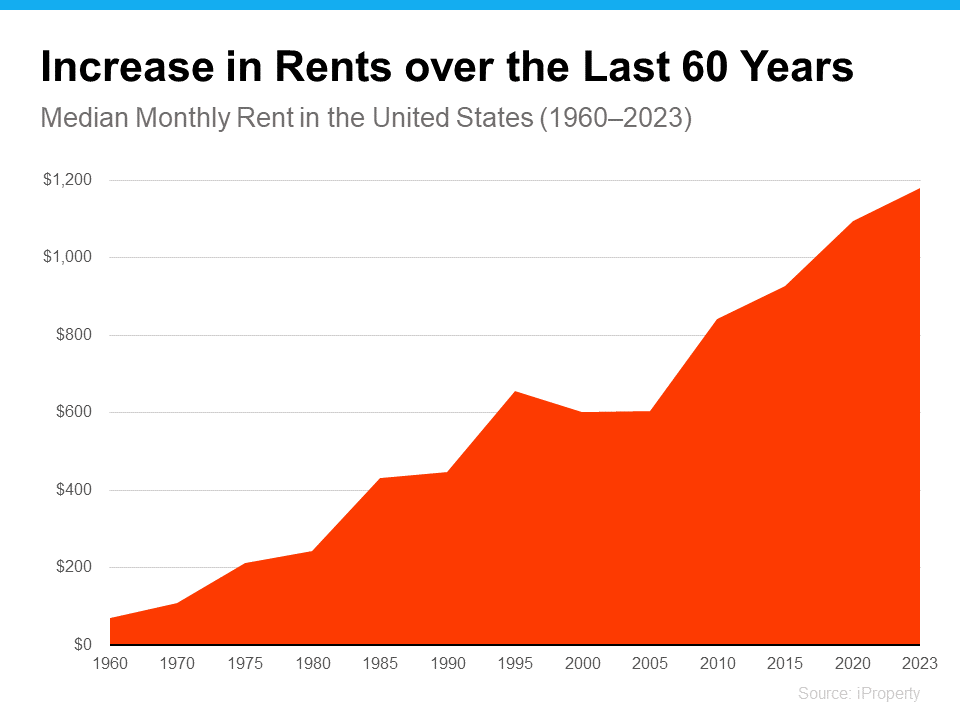

2. Rent Keeps Rising in the Long Run

Here’s another reason you may want to think about buying a home instead of renting – rent just keeps going up over the years. Sure, it might be cheaper to rent right now in some areas, but every time you renew your lease or sign a new one, you’re likely to feel the squeeze of your rent getting higher. According to data from iProperty Management, rent has been going up pretty consistently for the last 60 years, too (see graph below):

So how do you escape the cycle of rising rents? Buying a home with a fixed-rate mortgage helps you stabilize your housing costs and say goodbye to those annoying rent increases. That kind of stability is a big deal.

Your housing payments are like an investment, and you’ve got a decision to make. Do you want to invest in yourself or keep paying your landlord?

When you own your home, you’re investing in your own future. And even when renting is cheaper, that money you pay every month is gone for good.

As Dr. Jessica Lautz, Deputy Chief Economist and VP of Research at the National Association of Realtors (NAR), says:

“If a homebuyer is financially stable, able to manage monthly mortgage costs and can handle the associated household maintenance expenses, then it makes sense to purchase a home.”

Bottom Line

If you’re tired of your rent going up and want to explore the many benefits of homeownership, let’s talk to explore your options.

Is a Multi-Generational Home Right for You?

Is a Multi-Generational Home Right for You?

Ever thought about living in the same house with your grandparents, parents, or other loved ones? You’re not alone. A lot of people are choosing to buy multi-generational homes where everyone can live together. Let’s check out why they think it’s a good idea to see if it might be a good fit for you, too.

Why People Are Choosing Multi-Generational Living

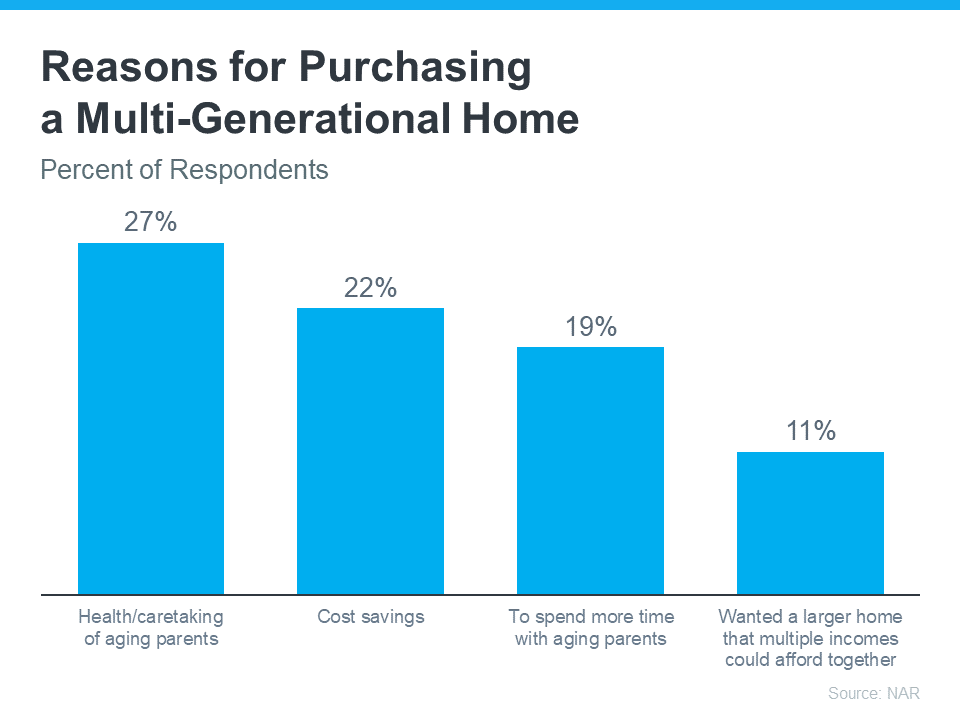

According to the National Association of Realtors (NAR), here are just a few key reasons buyers opted for multi-generational homes over the past year (see graph below):

Two of the top reasons had to do with aging parents. 27% of buyers chose multi-generational homes so they could take care of their parents more easily. And 19% did it to spend more time with them. A lot of older adults want to age in place, and living in a home with loved ones can help them do just that. If your parents are hoping to do the same, but need a bit of help, a multi-generational home may be worth considering.

But buying a multi-generational home isn’t just about being close or taking care of the people you love—it can save you money, too. 22% of buyers say they picked a multi-generational home to cut down on costs, and 11% needed a bigger house multiple incomes could afford together.

Sharing costs like the mortgage and utilities can make owning a home more affordable. This is especially helpful for first-time homebuyers who might find it challenging to buy a place on their own in today’s market.

As Axios explains:

“Financial concerns and caregiving needs are two of the major reasons people live with their parents (and parents’ parents).”

How an Agent Is Key in Finding the Right Home for You

Looking for the perfect multi-generational home is a bit trickier than finding a regular house. You’ve got more people, which means more opinions and needs to think about. It’s kind of like putting together a puzzle where all the pieces need to fit perfectly.

If you’re into the idea of living with loved ones and want all the benefits that come with it, team up with a local real estate agent who can help you out.

Bottom Line

Whether you’re looking to save money or want to take care of your loved ones, buying a multi-generational home might be a good idea for you. If you want to find out more, let’s talk.

3 Keys To Hitting Your Homeownership Goals in 2024

3 Keys To Hitting Your Homeownership Goals in 2024

If buying or selling a home is your goal for 2024, it’s important to understand today’s housing market, know your why, and work with industry experts to bring your homeownership vision for the new year into focus.

Over the last year, the economy had a big impact on the housing market, and likely on your wallet too. That’s why it’s critical to have a clear picture of not just the market today, but also on what you want out of it when you buy or sell a home. Danielle Hale, Chief Economist at Realtor.com, explains:

“The key to making a good decision in this challenging housing market is to be laser focused on what you need now and in the years ahead, so that you can stay in your home long enough that buying is a sound financial decision.”

Here are a few things to think through as you define your goals for 2024.

1. Know Your Why

You’re dreaming about making a move for a reason – what is it? No matter what’s happening in the market, there are still many compelling reasons to buy a home today. Your needs may have changed in a way your current house can’t address, or you could be ready to step into homeownership for the first time. Use your why and your motivation as a guidepost in partnership with an expert advisor to make sure your move gives you a lasting sense of accomplishment.

2. Figure Out What Your Next Home Needs To Look Like

You know you want to move, but how would you describe your dream home? The number of homes for sale has grown recently, and that could mean more options to choose from when you buy. But overall housing supply is still lower than more normal years in the market, so you’ll have to work closely with a pro to find what you’re looking for. Just be sure to keep your budget in mind as you balance your wants and needs. The better you understand what’s essential and where you can be flexible, the easier it will be to find a home that’s right for you.

3. Determine if You’re Ready To Buy

Getting clear on your budget and available savings is essential before you get too far into the process. Partnering with a local agent and a lender early is the best way to make sure you’re in a good position to buy. This could include planning how much to save for a down payment, getting pre-approved for a home loan, and assessing your current home equity if you’re selling your existing house.

A Professional Will Guide You Through Every Step of the Process

Buying or selling a home takes expertise to navigate. If that feels a bit overwhelming, that’s normal. Don’t let uncertainty hold you back from your goals this year. A trusted expert will help you bridge that gap and give you the facts and advice you need about today’s housing market.

Bottom Line

Let’s connect to plan how to make your homeownership dreams a reality in 2024.

What You Really Need To Know About Home Prices

What You Really Need To Know About Home Prices

According to recent data from Fannie Mae, almost 1 in 4 people still think home prices are going to come down. If you’re one of the people worried about that, here’s what you need to know.

A lot of that fear is probably coming from what you’re hearing in the media or reading online. But here’s the thing to remember. Negative news sells. That means, you may not be getting the full picture. You may only be getting the clickbait version. As Jay Thompson, a Real Estate Industry Consultant, explains:

“Housing market headlines are everywhere. Many are quite sensational, ending with exclamation points or predicting impending doom for the industry. Clickbait, the sensationalizing of headlines and content, has been an issue since the dawn of the internet, and housing news is not immune to it.”

Here’s a look at the data to set the record straight.

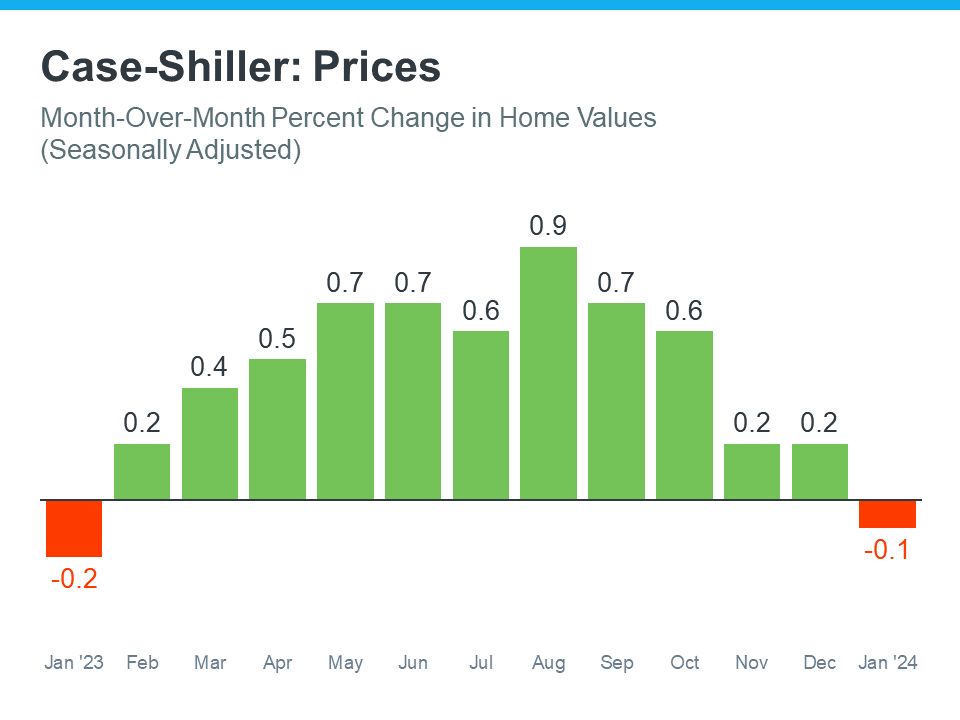

Home Prices Rose the Majority of the Past Year

Case-Shiller releases a report each month on the percent of monthly home price changes. If you look at their data from January 2023 through the latest numbers available, here’s what you’d see:

What do you notice when you look at this graph? It depends on what color you’re more drawn to. If you look at the green, you’ll see home prices rose for the majority of the past year.

But, if you’re drawn to the red, you may only focus on the two slight declines. This is what a lot of media coverage does. Since negative news sells, drawing attention to these slight dips happens often. But that loses sight of the bigger picture.

Here’s what this data really says. There’s a lot more green in that graph than red. And even for the two red bars, they’re so slight, they’re practically flat. If you look at the year as a whole, home prices still rose overall.

It’s perfectly normal in the housing market for home price growth to slow down in the winter. That’s because fewer people move during the holidays and at the start of the year, so there’s not as much upward pressure on home prices during that time. That’s why, even the green bars toward the end of the year show smaller price gains.

The overarching story is that prices went up last year, not down.

To sum all that up, the source for that data in the graph above, Case Shiller, explains it like this:

“Month-over-month numbers were relatively flat, . . . However, the annual growth was more significant for both indices, rising 7.4 percent and 6.6 percent, respectively.”

If one of the expert organizations tracking home price trends says the very slight dips are nothing to worry about, why be concerned? Even Case-Shiller is drawing your attention to how those were virtually flat and how home prices actually grew over the year.

Bottom Line

The data shows that, as a whole, home prices rose over the past year. If you have questions about what’s happening with home prices in our area, let’s chat.

Is It Getting More Affordable To Buy a Home?

Is It Getting More Affordable To Buy a Home?

Over the past year or so, a lot of people have been talking about how tough it is to buy a home. And while there’s no arguing affordability is still tight, there are signs it’s starting to get a bit better and may improve even more throughout the year. Elijah de la Campa, Senior Economist at Redfin, says:

“We’re slowly climbing our way out of an affordability hole, but we have a long way to go. Rates have come down from their peak and are expected to fall again by the end of the year, which should make homebuying a little more affordable and incentivize buyers to come off the sidelines.”

Here’s a look at the latest data for the three biggest factors that affect home affordability: mortgage rates, home prices, and wages.

1. Mortgage Rates

Mortgage rates have been volatile this year – bouncing around in the upper 6% to low 7% range. That’s still quite a bit higher than where they were a couple of years ago. But there is a sliver of good news.

Despite the recent volatility, rates are still lower than they were last fall when they reached nearly 8%. On top of that, most experts still think they’ll come down some over the course of the year. A recent article from Bright MLS explains:

“Expect rates to come down in the second half of 2024 but remain above 6% this year. Even a modest drop in rates will bring both more buyers and more sellers into the market.”

Any drop in rates can make a difference for you. When rates go down, you can afford the home you really want more easily because your monthly payment would be lower.

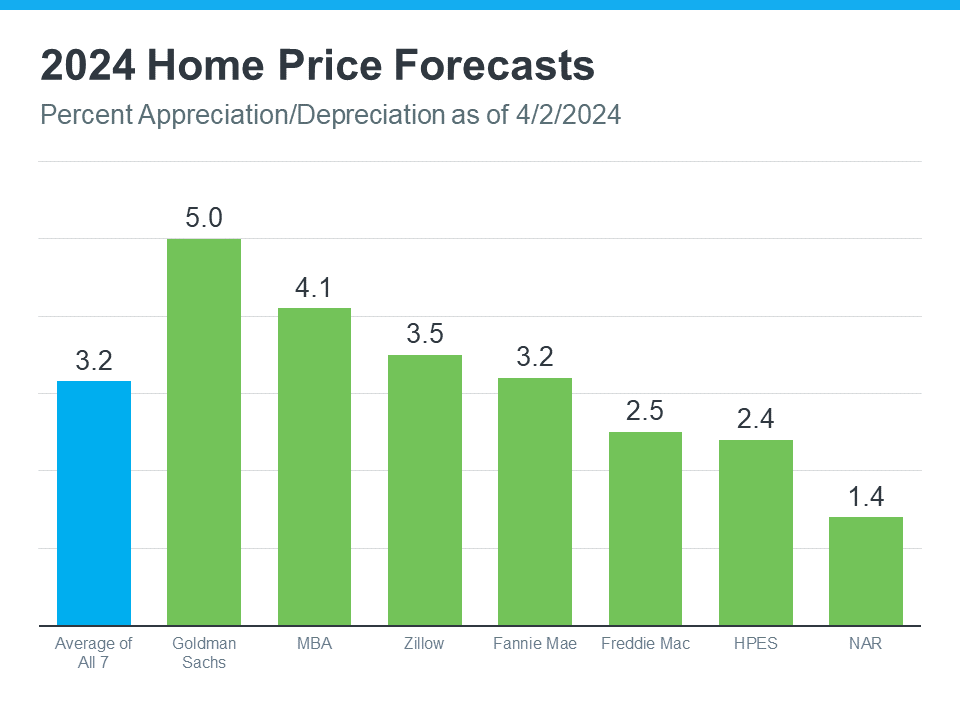

2. Home Prices

The second big factor to think about is home prices. Most experts project they’ll keep going up this year, but at a more normal pace. That’s because there are more homes on the market this year, but still not enough for everyone who wants to buy one. The graph below shows the latest 2024 home price forecasts from seven different organizations:

These forecasts are actually good news for you because it means the prices aren’t likely to shoot up sky high like they did during the pandemic. That doesn’t mean they’re going to fall – they’ll just rise at a slower pace.

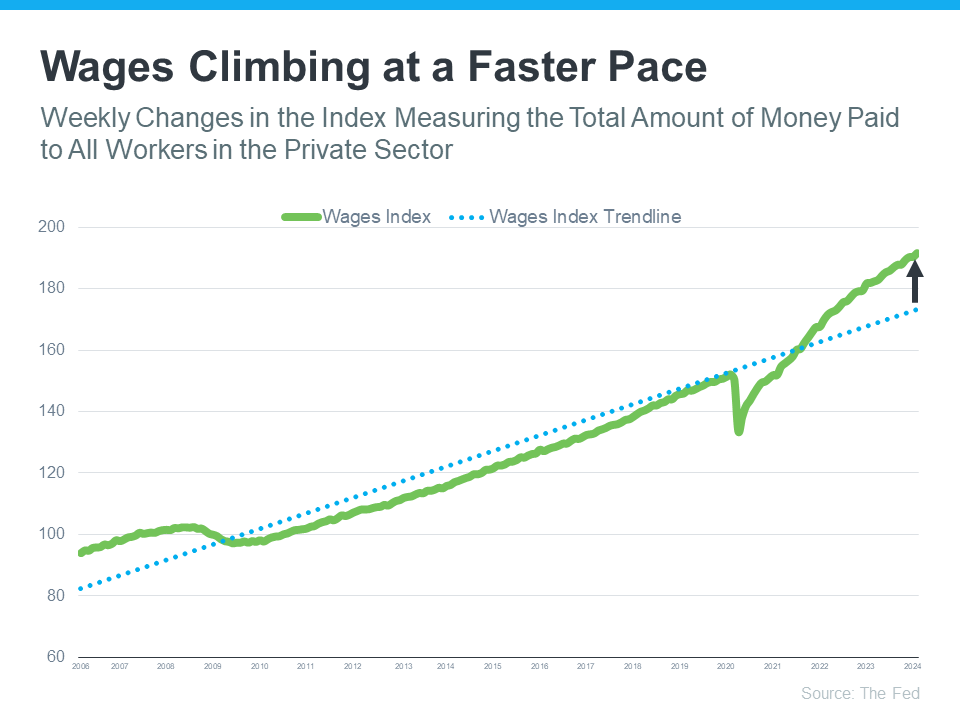

3. Wages

One factor helping affordability right now is the fact that wages are rising. The graph below uses data from the Federal Reserve to show how wages have been growing over time:

Check out the blue dotted line. That shows how wages typically rise. If you look at the right side of the graph, you’ll see wages are climbing even faster than normal right now.

Here’s how this helps you. If your income has increased, it’s easier to afford a home because you don’t have to spend as big of a percentage of your paycheck on your monthly mortgage payment.

Bottom Line

If you stack these factors up, you’ll see mortgage rates are still projected to come down a bit later this year, home prices are going up at a more moderate pace, and wages are growing quicker than normal. Those trends are a good sign for your ability to afford a home.

Is It Better To Rent Than Buy a Home Right Now?

Is It Better To Rent Than Buy a Home Right Now?

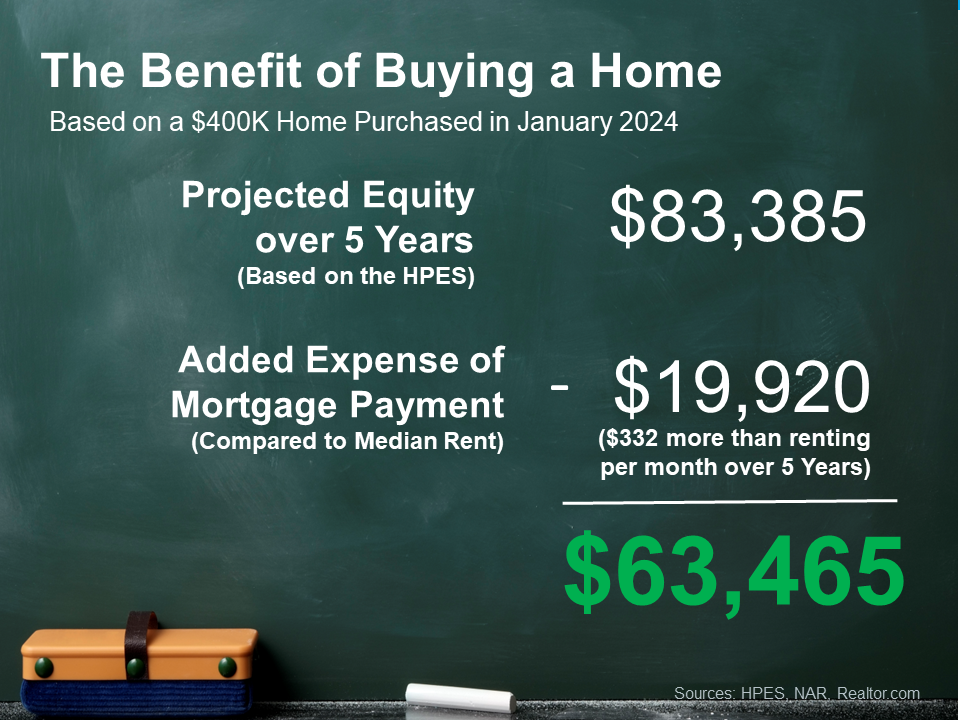

You may have seen reports in the news recently saying it’s more affordable to rent right now than it is to buy a home. And while that may be true in some markets if you just look at typical monthly payments, there’s one thing that the numbers aren’t factoring in: and that’s home equity. Here’s a look at how big of an impact equity can have and why it’s worth considering as you make your decision.

What the Headlines Are Based on

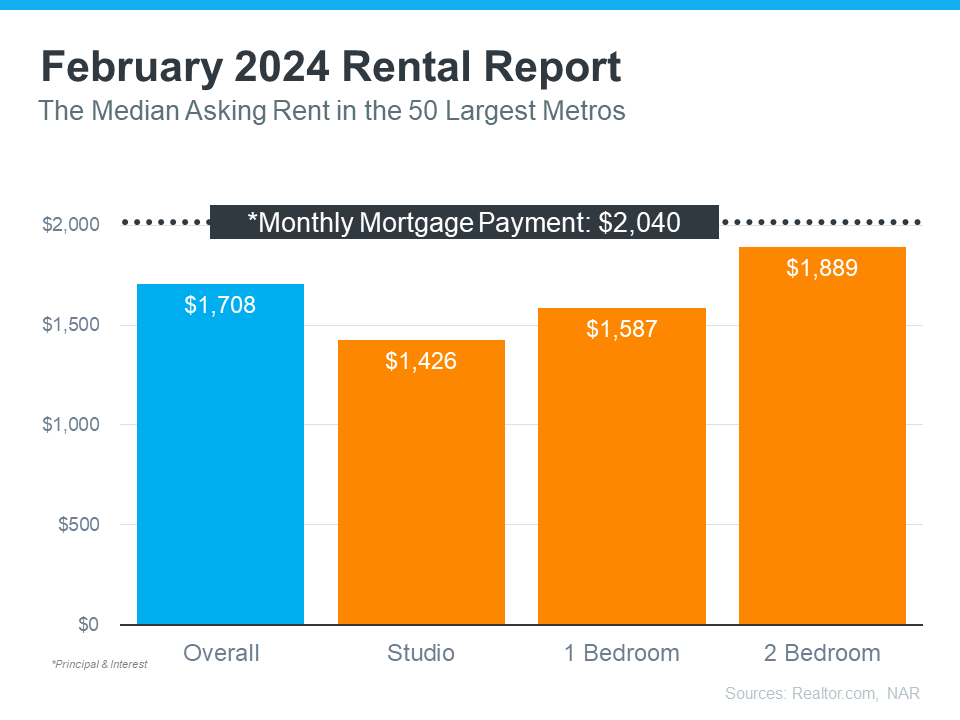

The graph below uses national data on the median rental payment from Realtor.com and median mortgage payment from the National Association of Realtors (NAR) to compare the two options. As the graph shows, especially if you’re not looking for a lot of space, it can be more affordable on a monthly basis to rent:

But if you’re looking for something with 2 bedrooms, the gap between the median rent and the median mortgage payment starts to shrink to a difference that may be more doable. The median monthly mortgage payment is $2,040. The median monthly rent for 2 bedrooms is $1,889. That’s a difference of about $151 a month. But here’s what happens when you factor in equity too.

How Equity Changes the Game

If you rent, your monthly rental payments only go toward covering your housing costs and your landlord’s expenses. So other than saving a bit more per month and maybe getting your rental deposit back when you move, the money you spent on housing each month is gone – forever.

When you buy, your monthly mortgage payment pays for your shelter, but it also acts as an investment. That investment grows in the form of equity as you make your mortgage payment each month and chip away at what you owe on your home loan. Your equity gets an extra boost as home values climb – which they typically do.

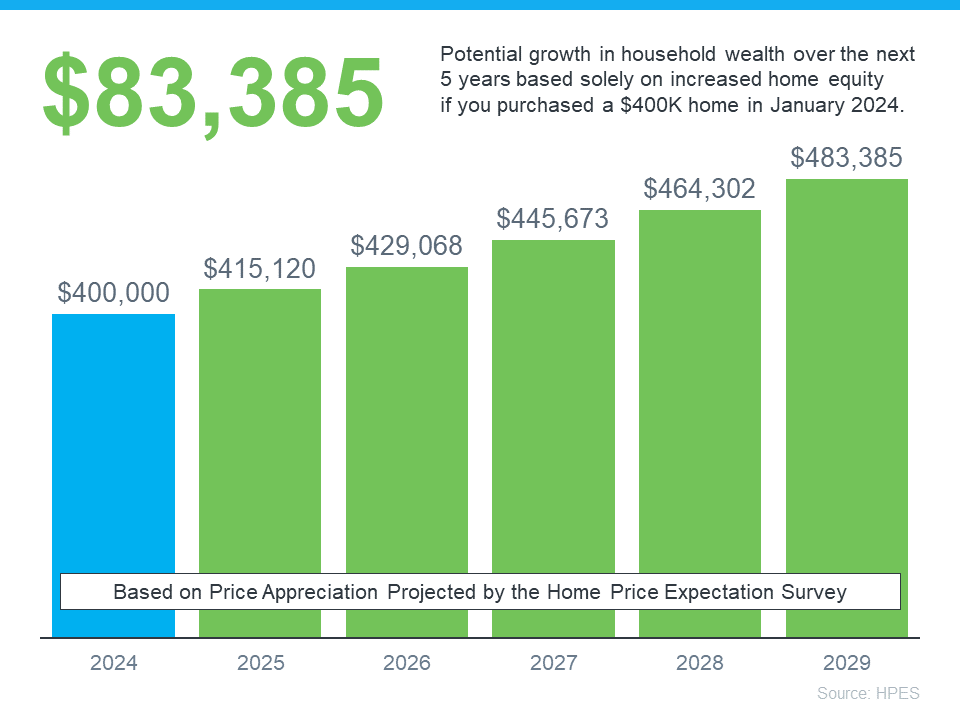

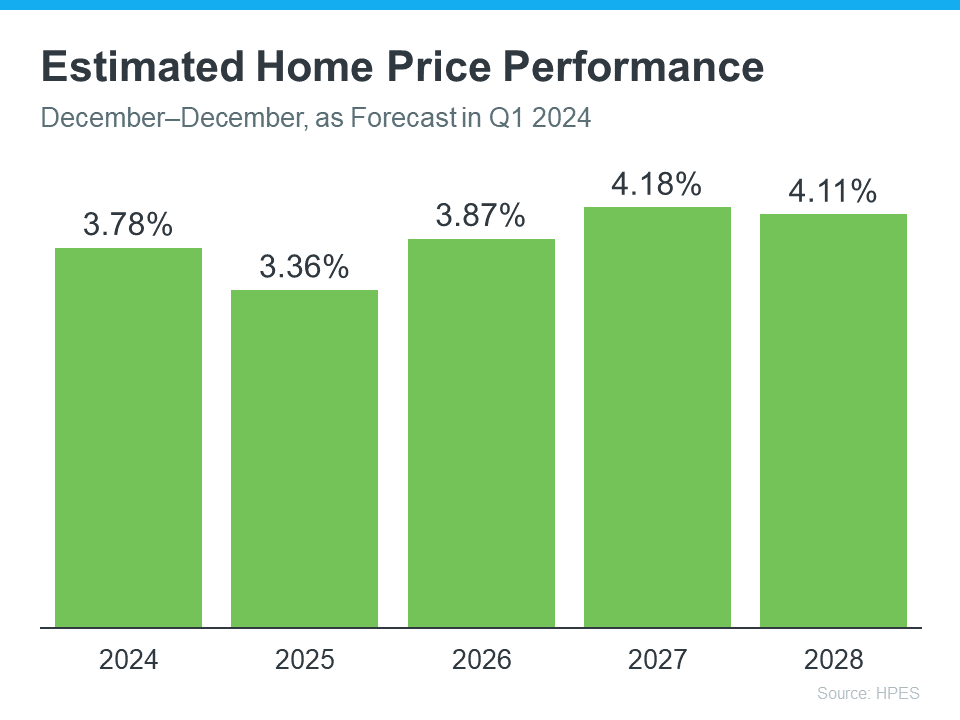

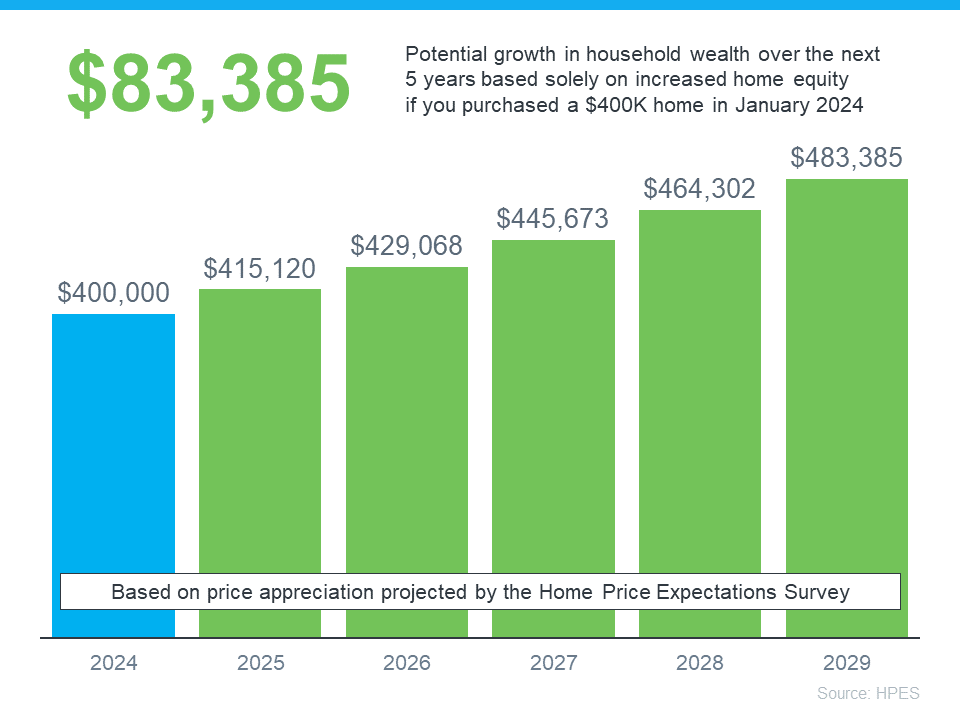

To give you a clearer idea of how equity can really stack up fast, here’s some data for you. Each quarter, Fannie Mae and Pulsenomics publish the results of the Home Price Expectations Survey (HPES). It asks more than 100 economists, real estate professionals, and investment and market strategists what they think will happen with home prices. In the latest release, those experts say home prices are going to keep going up over the next five years.

Here’s an example of how equity builds based on the projections from the HPES (see graph below):

Imagine you purchased a home for $400,000 at the start of this year. Chances are, since you bought, you plan to stay put for a while. Based on the HPES projections, if you live there for 5 years, you could end up gaining over $83,000 in household wealth as your home grows in value.

Here’s how that stacks up compared to renting, using the overall median rent from above:

While you may save a bit on your monthly payments if you rent right now, you’ll also miss out on gaining equity.

So, what’s the big takeaway? Whether it makes more sense to rent or buy is going to vary based on your personal finances. It’s not a good idea to buy if the numbers truly don’t work for you. But, if you’re ready and able, adding equity as the final puzzle piece may be enough to help you realize buying is a better move in the long run.

Bottom Line

When it comes down to it, buying a home gives you a benefit renting just can’t provide – and that’s the chance to gain equity. If you want to take advantage of long-term home price appreciation, let’s go over your options.

Should I Wait for Mortgage Rates To Come Down Before I Move?

Should I Wait for Mortgage Rates To Come Down Before I Move?

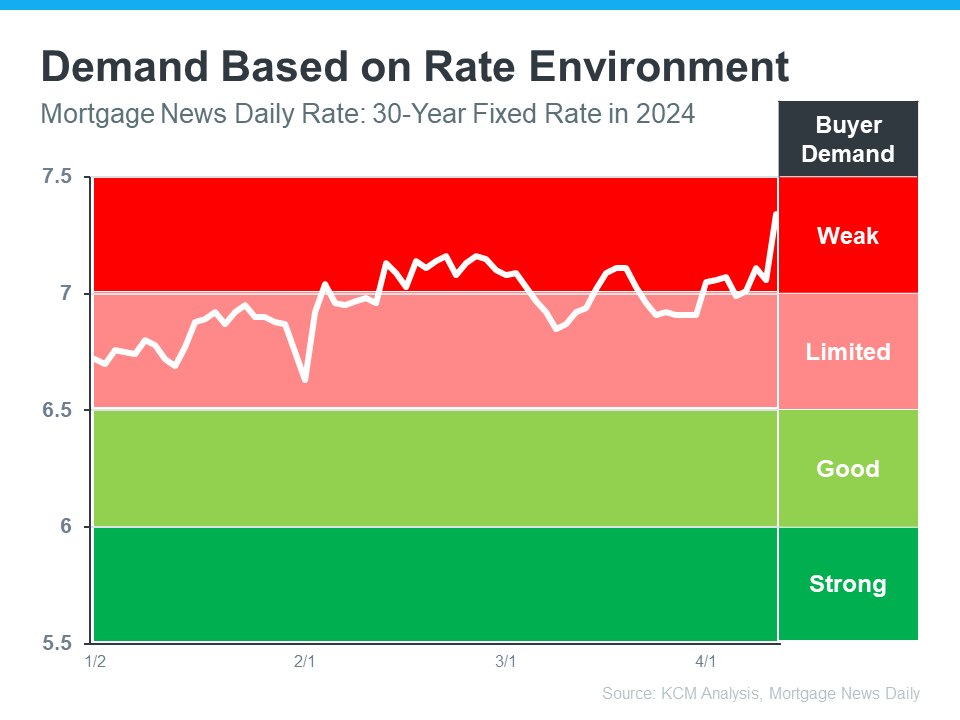

If you’ve got a move on your mind, you may be wondering whether you should wait to sell until mortgage rates come down before you spring into action. Here’s some information that could help answer that question for you.

In the housing market, there’s a longstanding relationship between mortgage rates and buyer demand. Typically, the higher rates are, you’ll see lower buyer demand. That’s because some people who want to move will be hesitant to take on a higher mortgage rate for their next home. So, they decide to wait it out and put their plans on hold.

But when rates start to come down, things change. It goes from limited or weak demand to good or strong demand. That’s because a big portion of the buyers who sat on the sidelines when rates were higher are going to jump back in and make their moves happen. The graph below helps give you a visual of how this relationship works and where we are today:

As Lisa Sturtevant, Chief Economist for Bright MLS, explains:

“The higher rates we’re seeing now [are likely] going to lead more prospective buyers to sit out the market and wait for rates to come down.”

Why You Might Not Want To Wait

If you’re asking yourself: what does this mean for my move? Here’s the golden nugget. According to experts, mortgage rates are still projected to come down this year, just a bit later than they originally thought.

When rates come down, more people are going to get back into the market. And that means you’ll have a lot more competition from other buyers when you go to purchase your next home. That may make your move more stressful if you wait because greater demand could lead to an increase in multiple offer scenarios and prices rising faster.

But if you’re ready and able to sell now, it may be worth it to get ahead of that. You have the chance to move before the competition increases.

Bottom Line

If you’re thinking about whether you should wait for rates to come down before you move, don’t forget to factor in buyer demand. Once rates decline, competition will go up even more. If you want to get ahead of that and sell now, let’s chat.

Ways To Use Your Tax Refund If You Want To Buy a Home

Ways To Use Your Tax Refund If You Want To Buy a Home

Have you been saving up to buy a home this year? If so, you know there are a number of expenses involved – from your down payment to closing costs. But did you also know your tax refund can help you pay for some of these expenses? As Credit Karma explains:

“If one of your goals is to stop renting and buy a home, you’ll need to save up for closing costs and a down payment on the mortgage. A tax refund can give you a start on the road to homeownership. If you’ve already started to save, your tax refund could move you down the road faster.”

While how much money you may get in a tax refund is going to vary, it can be encouraging to have a general idea of what’s possible. Here’s what CNET has to say about the average increase people are seeing this year:

“The average refund size is up by 6.1%, from $2,903 for 2023’s tax season through March 24, to $3,081 for this season through March 22.”

Sounds great, right? Remember, your number is going to be different. But if you do get a refund, here are a few examples of how you can use it when buying a home. According to Freddie Mac:

- Saving for a down payment – One of the biggest barriers to homeownership is setting aside enough money for a down payment. You could reach your savings goal even faster by using your tax refund to help.

- Paying for closing costs – Closing costs cover some of the payments you’ll make at closing. They’re generally between 2% and 5% of the total purchase price of the home. You could direct your tax refund toward these closing costs.

- Lowering your mortgage rate – Your lender might give you the option to buy down your mortgage rate. If affordability is tight for you at today’s rates and home prices, this option may be worth exploring. If you qualify for this option, you could pay upfront to have a lower rate on your mortgage.

The best way to get ready to buy a home is to work with a team of trusted real estate professionals who understand the process and what you’ll need to do to be ready to buy.

Bottom Line

Your tax refund can help you reach your savings goal for buying a home. Let’s talk about what you’re looking for, because your home may be more within reach than you think.

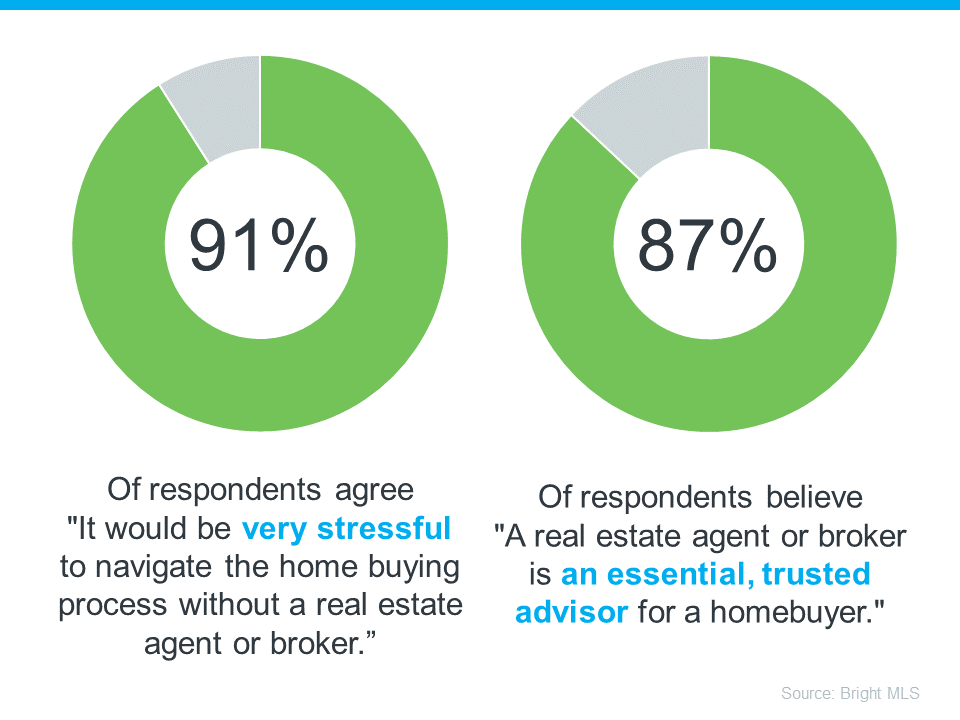

The Top 5 Reasons You Need a Real Estate Agent when Buying a Home

The Top 5 Reasons You Need a Real Estate Agent when Buying a Home

You may have heard headlines in the news lately about agents in the real estate industry and discussions about their commissions. And if you’re following along, it can be pretty confusing. But here’s the thing you really need to know – expert advice from a trusted real estate agent is priceless, now more than ever. And here’s why.

A real estate agent does a lot more than you may realize.

Your agent is the person who will guide you through every step when buying a home and look out for your best interests along the way. They smooth out a complex process and take away the bulk of the stress of what’s likely your largest purchase ever. And that’s exactly what you want and deserve.

This is at least a part of the reason why a recent survey from Bright MLS found an overwhelming majority of people agree an agent is a key part of the homebuying process (see visual below):

To give you a better idea of just a few of the top ways agents add value, check out this list.

1. Deliver Industry Experience

The right agent – the professional – will coach you through everything from start to finish. With professional training and expertise, agents know the ins and outs of the buying process. And in today’s complex market, the way real estate transactions are executed is constantly changing, so having the best advice on your side is essential.

2. Provide Expert Local Knowledge

In a world that’s powered by data, a great agent can clarify what it all means, separate fact from fiction, and help you understand how current market trends apply to your unique search. From how quickly homes are selling to the latest listings you don’t want to miss, they can explain what’s happening in your specific local market so you can make a confident decision.

3. Explain Pricing and Market Value

Agents help you understand the latest pricing trends in your area. What’s a home valued at in your market? What should you think about when you’re making an offer? Is this a house that might have issues you can’t see on the surface? No one wants to overpay, so having an expert who really gets true market value for individual neighborhoods is priceless. An offer that’s both fair and competitive in today’s housing market is essential, and a local expert knows how to help you hit the mark.

4. Review Contracts and Fine Print

In a fast-moving and heavily regulated process, agents help you make sense of the necessary disclosures and documents, so you know what you’re signing. Having a professional that’s trained to explain the details could make or break your transaction, and is certainly something you don’t want to try to figure out on your own.

5. Bring Negotiation Expertise

From offer to counteroffer and inspection to closing, there are a lot of stakeholders involved in a real estate transaction. Having someone on your side who knows you and the process makes a world of difference. An agent will advocate for you as they work with each party. It’s a big deal, and you need a partner at every turn to land the best possible outcome.

Bottom Line

Real estate agents are specialists, educators, and negotiators. They adjust to market changes and keep you informed. And keep in mind, every time you make a big decision in your life, especially a financial one, you need an expert on your side.

Expert advice from a trusted professional is priceless. Let’s connect today.

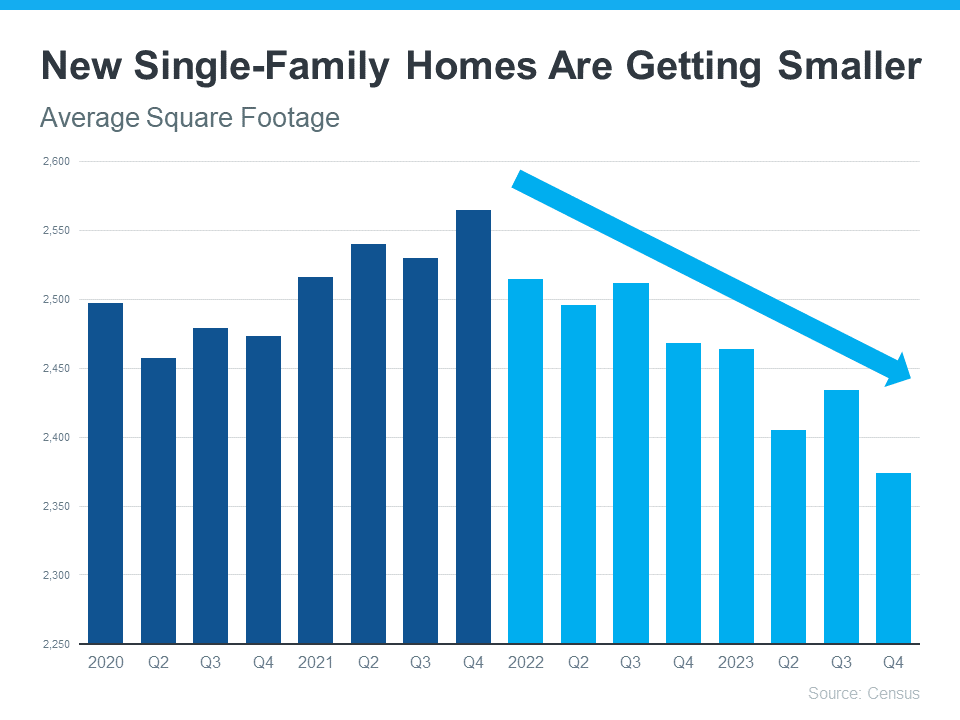

Builders Are Building Smaller Homes

Builders Are Building Smaller Homes

There’s no arguing it, affordability is still tight. And if you’re trying to buy a home, that may mean you need to look at smaller houses to find one that’s still in your budget. But there is a silver lining: builders are focused on building these smaller homes right now and they’re offering incentives. And that can help give you more options that fit the bill.

Newly Built Homes Are Trending Smaller

During the pandemic, homebuyers wanted (and could afford) larger homes – and builders delivered. They focused on homes that were bigger, so people had more space for things like working from home, having a home gym, bonus rooms for virtual school, and more.

But with the affordability challenges buyers are facing today, builders are increasingly shifting their attention to bringing smaller single-family homes to the market. The graph below uses data from the Census to show how this trend has evolved over the last few years:

So, why the shift to less square footage? It’s simple. Builders want to build what they know will sell. Basically, they focus on where the demand is strongest. And once mortgage rates started climbing and consumers felt the challenges of affordability creeping in, it became clear there was (and is) a very real need for smaller homes. As the National Association of Home Builders (NAHB) explains:

“After a brief increase during the post-covid building boom, home size is trending lower and will likely continue to do so as housing affordability remains constrained.”

A recent article in the Real Deal says this about how this helps buyers:

“Even a slightly smaller home can be thousands of dollars cheaper — for both builders and buyers. . . In response to affordability challenges, major homebuilders are shifting priorities away from the big ticket homes and towards the cheaper set.”

What This Means for You

If you’re having a hard time finding something in your budget, it may help to look at smaller homes. And, if you consider new builds specifically, you may find a few other fringe benefits that can help on the affordability front – like price reductions or mortgage rate buy-downs. As NAHB says:

“More than one-third of builders cut home prices in 2023. NAHB expects builders to continue offering smaller homes and more affordable designs as housing affordability remains a barrier to homeownership.”

As Charlie Bilello, Chief Market Strategist, at Creative Planning, explains:

“Homebuilders are adapting to the lowest affordability on record by building smaller homes and offering more incentives/price cuts. The median square footage of a new single-family home in the US has moved down to its lowest level since 2010.”

If you explore these options, you’ll also get brand new everything, enjoy a house with fewer maintenance needs, and some of the latest features available. That’s worth looking into, right?

Bottom Line

Builders building smaller homes can give you more affordable options at a time when you may really need it. If you’re hoping to buy a home soon, let’s connect to look at what’s available in our area.

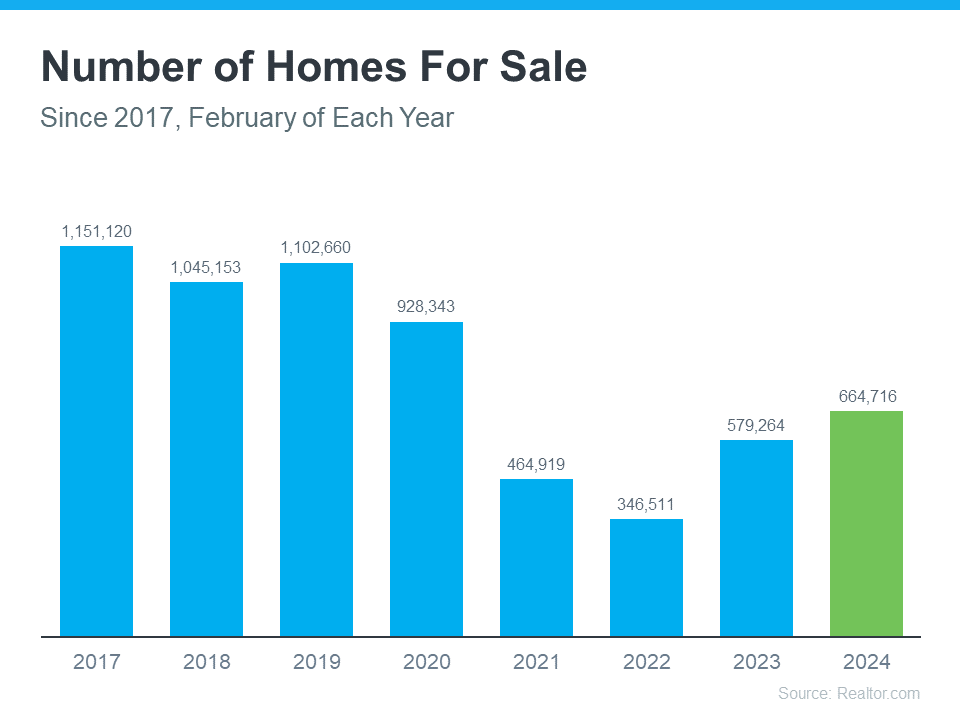

Is It Easier To Find a Home To Buy Now?

Is It Easier To Find a Home To Buy Now?

One of the biggest hurdles buyers have faced over the past few years has been a lack of homes available for sale. But that’s starting to change.

The graph below uses the latest data from Realtor.com to show there are more homes on the market in 2024 than there have been in any of the past several years (2021-2023):

Does That Mean Finding a Home Is Easier?

The answer is yes, and no. As an article from Realtor.com says:

“There were nearly 15% more homes for sale in February than a year earlier . . . That alone could jolt the housing market a bit if more “For Sale” signs continue to appear. However, the nation is still suffering from a housing shortage even with all of that new inventory.”

Context is important. On the one hand, inventory is up over the past few years. That means you’ll likely have more options to choose from as you search for your next home.

But, at the same time, the graph above also shows there are still significantly fewer homes for sale than there would usually be in a more normal, pre-pandemic market. And that deficit isn’t going to be reversed overnight.

What Does This Mean for You?

You might find a few more choices now than in recent years, but you shouldn’t expect a ton of options.

To help you explore the growing list of choices you have now, team up with a local real estate agent you trust. They can really help you understand the inventory situation where you want to buy. That’s because real estate is local. An experienced agent can share some smart tips they’ve used to help other buyers in your area deal with ongoing low housing supply.

Bottom Line

If you’re thinking about buying a home, let’s team up. That way, you’ll be up to date on everything that could affect your move, including how many homes are for sale right now.

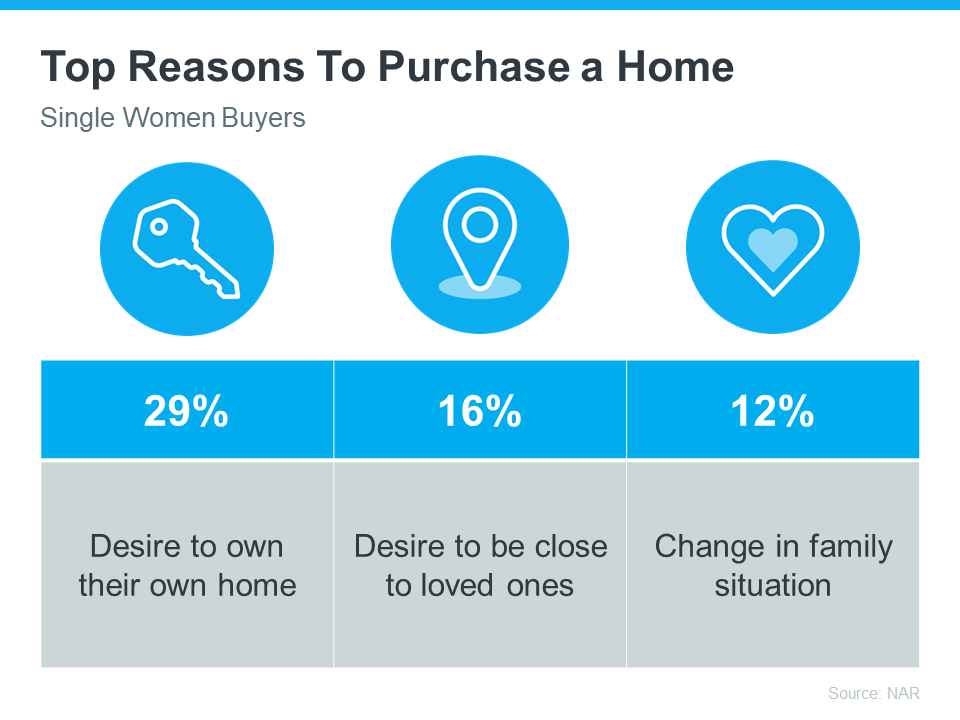

Single Women Are Embracing Homeownership

Single Women Are Embracing Homeownership

In today’s housing market, more and more single women are becoming homeowners. According to data from the National Association of Realtors (NAR), 19% of all homebuyers are single women, while only 10% are single men.

If you’re a single woman trying to buy your first home, this should be encouraging. It means other people are making their dreams a reality – so you can too.

Why Homeownership Matters to So Many Women

For many single women, buying a home isn’t just about having a place to live—it’s also a smart way to invest for the future. Homes usually increase in value over time, so they’re a great way to build equity and overall net worth. Ksenia Potapov, Economist at First American, says:

“. . . single women are increasingly pursuing homeownership and reaping its wealth creation benefits.”

The financial security and independence homeownership provides can be life-changing. And when you factor in the personal motivations behind buying a home, that impact becomes even clearer.

The same report from NAR shares the top reasons single women are buying a home right now, and the reality is, they’re not all financial (see chart below):

If any of these reasons resonate with you, maybe it’s time for you to buy too.

Work with a Trusted Real Estate Agent

If you’re a single woman looking to buy a home, it is possible, even in today’s housing market. You’ll just want to be sure you have a great real estate agent by your side.

Talk about what your goals are and why homeownership is so important to you. That way your agent can keep what’s critical for you up front as they guide you through the buying process. They’ll help you find the right home for your needs and advocate for you during negotiations. Together, you can make your dream of homeownership a reality.

Bottom Line

Homeownership is life-changing no matter who you are. Let’s connect today to talk about your goals in the housing market.

What’s the Latest with Mortgage Rates?

What’s the Latest with Mortgage Rates?

Recent headlines may leave you wondering what’s next for mortgage rates. Maybe you’d previously heard there were going to be cuts this year that would bring rates down. That refers to the Federal Reserve (the Fed) and what they do to their Fed Funds Rate. While cutting, or lowering, the Fed Funds Rate doesn’t directly determine mortgage rates, it does tend to impact them. But when the Fed met last week, a cut didn’t happen — at least, not yet.

There are a lot of factors the Fed considered in their recent decision and most of them are complex. But you don’t need to be bogged down by those finer details. What you really want is the answer to this question: does that mean mortgage rates aren’t going to fall? Here’s what you need to know.

Mortgage Rates Are Still Expected To Drop This Year

While it hasn’t happened yet, that doesn’t mean it won’t. Even Jerome Powell, the Chairman of the Fed, says they still plan to make cuts this year, assuming inflation cools:

“We believe that our policy rate is likely at its peak for this tightening cycle and that, if the economy evolves broadly as expected, it will likely be appropriate to begin dialing back policy restraint at some point this year.”

When this happens, history shows mortgage rates will likely follow. That means hope isn’t lost. As a recent article from Business Insider explains:

“As inflation comes down and the Fed is able to start lowering rates, mortgage rates should go down, too. . .”

What This Means for You

But you don’t necessarily want to wait for it to happen. Mortgage rates are notoriously hard to forecast. There are so many factors at play and any one of those can change the projections as the economy shifts. And it’s why the experts offer this advice. As Mark Fleming, Chief Economist at First American, says:

“Well, mortgage rate projections are just that, projections, not promises and don’t forget how hard it is to forecast them. . . So my advice is to never try to time the market . . . If one is financially prepared and buying a home aligns with your lifestyle goals, then it could be the right time to purchase. And there’s always the refinance option if mortgage rates are lower in the future.”

Basically, if you’re looking to move and trying to time the market, don’t. If you’re ready, willing, and able to move, it may still be worth it to do it now, especially if you can find the home you’ve been searching for.

Bottom Line

If you’re looking to buy a home, let’s connect so you have someone keeping you up-to-date on mortgage rates and helping you make the best decision possible.

Why Having Your Own Agent Matters When Buying a New Construction Home

Why Having Your Own Agent Matters When Buying a New Construction Home

Finding the right home is one of the biggest challenges for potential buyers today. Right now, the supply of homes for sale is still low. But there is a bright spot. Newly built homes make up a larger percent of the total homes available for sale than normal. That’s why, if you’re craving more options, it makes sense to see if a newly built home is right for you.

But it’s important to remember the process of working with a builder is different than buying from a homeowner. And, while builders typically have sales agents on-site, having your own agent helps make sure you have proper representation throughout your homebuying journey. As Realtor.com says:

“Keep in mind that the on-site agent you meet at a new-construction office works for the builder. So, as the homebuyer, it’s a smart idea to bring in your own agent, as well, to help you negotiate and stay protected in the transaction.”

Here’s how having your own agent is key when you build or buy a new construction home.

Agents Know the Local Area and Market

It’s important to consider how the neighborhood and surrounding area may evolve before making your home purchase. Your agent is well-versed in the upcoming communities and developments that could influence your decision. One way a real estate agent can help is by reviewing the builder’s site plan. For example, you’ll want to know if there are any plans to construct a highway or add a drainage ditch behind your prospective backyard.

Knowledge of Construction Quality and Builder Reputation

An agent also has expertise in the construction quality and reputation of different builders. They can give you insights into each one’s track record, customer satisfaction, and construction practices. Armed with this information, you can choose a builder known for consistently delivering top-notch homes.

Assistance with Customization and Upgrades

The most obvious benefit of opting for new home construction is the opportunity to customize your home. Your agent will guide you through that process and share advice on the upgrades that are most likely to add long-term value to your home. Their expertise helps make sure you focus your budget on areas that will give you the greatest return on your investment later.

Understanding Builder Negotiations and Contracts

When it comes to working with builders, having a skilled negotiator on your side can make all the difference. Builder contracts can be complex. Your agent can help you navigate these contracts to make sure you fully understand the terms and conditions. Plus, agents are skilled negotiators who can advocate for you, potentially securing better deals, upgrades, or incentives throughout the process. As Realtor.com says:

“A good buyer’s agent will be able to review any contracts before you sign on the dotted line, ensuring you aren’t unwittingly agreeing to terms that only benefit the builder.”

Bottom Line

If you are interested in buying or building a new construction home, having a trusted agent by your side can make a big difference. If you’d like to start that conversation, let’s connect.

Why So Many People Fall in Love with Homeownership

Why So Many People Fall in Love with Homeownership

Chances are at some point in your life you’ve heard the phrase, home is where the heart is. There’s a reason that’s said so often. Becoming a homeowner is emotional.

So, if you’re trying to decide if you want to keep on renting or if you’re ready to buy a home this year, here’s why it’s so easy to fall in love with homeownership.

Customizing to Your Heart’s Desire

Your house should be a space that’s uniquely you. And, if you’re a renter, that can be hard to achieve. When you rent, the paint colors are usually the standard shade of white, you don’t have much control over the upgrades, and you’ve got to be careful how many holes you put in the walls. But when you’re a homeowner, you have a lot more freedom. As the National Association of Realtors (NAR) says:

“The home is yours. You can decorate any way you want and choose the types of upgrades and new amenities that appeal to your lifestyle.”

Whether you want to paint the walls a cheery bright color or go for a dark moody tone, you can match your interior to your vibe. Imagine how it would feel to come home at the end of the day and walk into a space that feels like you.

Greater Stability for the Ones You Love Most

One of the hardest things about renting is the uncertainty of what happens at the end of your lease. Does your payment go up so much that you have to move? What if your landlord decides to sell the property? It’s like you’re always waiting for the other shoe to drop. Jeff Ostrowski, a business journalist covering real estate and the economy, explains how homeownership can give you more peace of mind in a Money Geek article:

“Homeownership means you are the boss and have the biggest say in your lifestyle and family decisions. Suppose your kids are in public school and you don’t want to risk having them change schools because your landlord doesn’t renew your lease. Owning a home would remove much of the risk of having to move.”

A Feeling of Belonging

You may also find you feel much more at home in the community once you own a house. That’s because, when you buy a home, you’re staking a claim and saying, I’m a part of this community. You’ll have neighbors, block parties, and more. And that’ll give you the feeling of being a part of something bigger. As the International Housing Association explains:

“. . . homeowning households are more socially involved in community affairs than their renting counterparts. This is due to both the fact that homeowners expect to remain in the community for a longer period of time and that homeowners have an ownership stake in the neighborhood.”

The Emotional High of Achieving Your Dream

Becoming a homeowner is a journey – and it may have been a long road to get to the point where you’re ready to take the plunge. If you’re seriously considering leaving behind your rental and making this commitment, you should know the emotions that come with this owning a home are powerful. You’ll be able to walk up to your front door every day and have that sense of accomplishment welcome you home.

Bottom Line

A home is a place that reflects who you are, a safe space for the ones you love the most, and a reflection of all you’ve accomplished. Let’s connect if you’re ready to break up with your rental and buy a home.

What Every Homebuyer Should Know About Closing Costs

What Every Homebuyer Should Know About Closing Costs

Before making the decision to buy a home, it’s important to plan for all the costs you’ll be responsible for. While you’re busy saving for the down payment, don’t forget you’ll want to prep for closing costs too.

Here’s some helpful information on what those costs are and how much you should budget for them.

What Are Closing Costs?

A recent article from Bankrate explains:

“Closing costs are the fees and expenses you must pay before becoming the legal owner of a house, condo or townhome . . . Closing costs vary depending on the purchase price of the home and how it’s being financed . . .”