Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

How to Prepare for Moving Day After Your Home Closes: The Ultimate Guide

🏡 How to Prepare for Moving Day After Your Home Closes: The Ultimate Guide

Congratulations! 🎉 You’ve closed on your new home — a major milestone in your real estate journey. But before you pop the champagne and settle in, there’s one more hurdle to cross: moving day. Whether you’re relocating across town or across the country, preparing for moving day can be overwhelming without a solid plan.

In this comprehensive guide, we’ll walk you through everything you need to know to make your move smooth, stress-free, and even enjoyable. From organizing your packing strategy to setting up utilities and updating your address, we’ve got you covered.

📝 Step 1: Create a Moving Timeline

The key to a successful move is planning ahead. As soon as your home closes, start building a moving timeline. This should include:

- 8 Weeks Before Moving Day: Research moving companies, declutter, and start gathering packing supplies.

- 6 Weeks Before: Begin packing non-essentials, notify schools and employers, and schedule time off work.

- 4 Weeks Before: Confirm your moving company, start changing your address, and arrange utility transfers.

- 2 Weeks Before: Pack most of your belongings, confirm travel plans, and prepare an essentials box.

- Moving Week: Finalize packing, clean your old home, and do a final walkthrough.

A timeline keeps you on track and reduces last-minute stress.

📦 Step 2: Declutter Before You Pack

Moving is the perfect opportunity to declutter your life. Go room by room and sort items into four categories:

- Keep

- Donate

- Sell

- Trash

Ask yourself: Have I used this in the last year? Does it bring me joy? If not, it’s time to let it go. Hosting a garage sale or listing items online can even help offset moving costs.

🛠️ Step 3: Gather Packing Supplies

You’ll need more than just boxes. Stock up on:

- Sturdy moving boxes (various sizes)

- Packing tape and dispensers

- Bubble wrap and packing paper

- Permanent markers for labeling

- Stretch wrap for furniture

- Mattress covers and moving blankets

Pro tip: Check with local stores or online marketplaces for free boxes.

🧳 Step 4: Pack Smart and Label Everything

Start with items you use the least and work your way to daily essentials. Use these tips for efficient packing:

- Label each box with the room and contents.

- Color-code boxes by room using tape or stickers.

- Wrap fragile items in bubble wrap or towels.

- Use suitcases for heavy items like books.

- Don’t overpack boxes — keep them under 50 lbs.

Packing room by room helps you stay organized and makes unpacking easier.

🏷️ Step 5: Change Your Address and Notify Important Parties

Don’t let important mail get lost in the shuffle. Update your address with:

- USPS (you can do this online)

- Banks and credit card companies

- Insurance providers

- Employers and payroll

- Subscription services

- Friends and family

Also, update your driver’s license and vehicle registration if you’re moving to a new state.

🔌 Step 6: Transfer Utilities and Services

Avoid moving into a dark or cold home by scheduling utility transfers ahead of time. Contact:

- Electric and gas companies

- Water and sewer services

- Internet and cable providers

- Trash and recycling services

- Home security companies

Schedule disconnections at your old home for the day after your move and connections at your new home for the day before.

🧹 Step 7: Clean Your Old Home

Whether you’re selling or renting, leave your old home in good condition. Clean:

- Floors and carpets

- Bathrooms and kitchens

- Inside cabinets and appliances

- Windows and baseboards

Consider hiring a professional cleaning service if you’re short on time.

🧰 Step 8: Prepare an Essentials Box

Pack a box (or suitcase) with everything you’ll need for the first 24–48 hours in your new home:

- Toiletries and medications

- Chargers and electronics

- Snacks and bottled water

- A few changes of clothes

- Bedding and towels

- Important documents

This box should travel with you, not the movers.

🚚 Step 9: Hire the Right Moving Company

If you’re not doing it yourself, research and hire a reputable moving company. Look for:

- Positive online reviews

- Transparent pricing

- Proper licensing and insurance

- Experience with your type of move

Get at least three quotes and ask about additional fees for stairs, long carries, or bulky items.

🐶 Step 10: Make a Plan for Kids and Pets

Moving day can be chaotic for little ones and furry friends. Arrange for:

- A babysitter or family member to watch children

- A pet sitter or boarding facility for pets

- A quiet, safe space for them during the move

This keeps them safe and reduces stress for everyone.

🧾 Step 11: Do a Final Walkthrough

Before leaving your old home, do a final walkthrough to:

- Check closets, cabinets, and drawers

- Turn off lights and appliances

- Lock all doors and windows

- Take photos for your records

Leave behind keys, garage openers, and any manuals for the new owners.

🛋️ Step 12: Unpack Strategically

Once you arrive, resist the urge to unpack everything at once. Start with:

- Essentials box

- Kitchen

- Bedrooms

- Bathrooms

- Living areas

Take your time and enjoy setting up your new space. This is your fresh start!

🧠 Bonus Tips for a Smooth Move

- Take photos of electronics before unplugging them.

- Use clear bins for items you’ll need right away.

- Label cords and remotes with masking tape.

- Keep important documents like closing papers and IDs in a safe place.

- Stay hydrated and take breaks on moving day.

🏁 Conclusion: Moving Day Doesn’t Have to Be Stressful

With the right preparation, moving day can be a celebration — not a headache. By following this guide, you’ll stay organized, reduce stress, and start your new chapter on the right foot. Remember, it’s not just about moving your stuff — it’s about moving your life. Make it count! 💪🏡

📣 Ready to Make Your Move?

If you’re looking for expert guidance, local insights, or help finding your next dream home, I’m here to help! Reach out today and let’s make your next move your best one yet. 📞📬

🔖 Top Real Estate Hashtags:

#MovingDay, #HomeClosing, #RealEstateTips, #NewHome, #MovingChecklist, #HomeBuyers, #Relocation, #PackingTips, #RealEstateAdvice, #HomeSweetHome, #MovingMadeEasy, #FirstTimeHomeBuyer, #HouseGoals, #RealEstateLife, #DreamHome

Top Home Improvements That Add Value Before Selling

🏡 Top Home Improvements That Add Value Before Selling

Thinking about selling your home? 🏠 Before you list it, making the right home improvements can significantly increase your property’s value—and help it sell faster. In today’s competitive real estate market, buyers are looking for move-in-ready homes with modern features, energy efficiency, and curb appeal.

In this comprehensive guide, we’ll explore the top home upgrades in 2025 that offer the best return on investment (ROI), from budget-friendly fixes to major renovations. Whether you’re a homeowner preparing to sell or a real estate professional advising clients, these insights will help you make smart, profitable decisions.

🔧 Why Home Improvements Matter Before Selling

According to Zillow, 65% of sellers who sold their homes in the past two years made at least two home improvements before listing.

The right improvements can:

- Increase your home’s market value 💰

- Attract more buyers 👀

- Shorten time on the market ⏳

- Improve appraisal outcomes 📈

But not all upgrades are created equal. Let’s dive into the ones that truly pay off.

🥇 Top 10 High-ROI Home Improvements in 2025

Based on the latest data from Remodeling Magazine and HomeLight, here are the top home improvements that offer the best bang for your buck:

1. 🚪 Garage Door Replacement

- Cost: $4,302

- Resale Value: $4,418

- ROI: 102.7%

A new garage door instantly boosts curb appeal and offers a full return on investment. Choose a modern, insulated model with smart features for added appeal.

2. 🪨 Manufactured Stone Veneer

- Cost: $10,925

- Resale Value: $11,177

- ROI: 102.3%

Adding stone veneer to your home’s exterior creates a luxurious, high-end look that buyers love.

3. 🚪 Steel Entry Door Replacement

- Cost: $2,214

- Resale Value: $2,235

- ROI: 100.9%

A sleek, secure steel door makes a strong first impression and improves energy efficiency.

4. 🧱 Vinyl Siding Replacement

- Cost: $16,348

- Resale Value: $15,485

- ROI: 94.7%

New siding refreshes your home’s exterior and protects it from the elements—key for buyers concerned with maintenance.

5. 🏠 Fiber-Cement Siding

- Cost: $19,361

- Resale Value: $17,129

- ROI: 88.5%

Fiber-cement siding is durable, fire-resistant, and attractive—ideal for long-term value.

6. 🍽️ Minor Kitchen Remodel (Midrange)

- Cost: $26,790

- Resale Value: $22,963

- ROI: 85.7%

Update cabinets, countertops, and appliances without a full gut job. A refreshed kitchen is a major selling point.

7. 🪟 Vinyl Window Replacement

- Cost: $20,091

- Resale Value: $13,766

- ROI: 68.5%

Energy-efficient windows reduce utility bills and improve comfort—two big wins for buyers.

8. 🛁 Midrange Bathroom Remodel

- Cost: $24,606

- Resale Value: $16,413

- ROI: 66.7%

Modern fixtures, new tile, and better lighting can transform a dated bathroom into a spa-like retreat.

9. 🪟 Wood Window Replacement

- Cost: $24,376

- Resale Value: $14,912

- ROI: 61.2%

Wood windows offer a classic look but require more maintenance. Still, they appeal to buyers in historic or upscale neighborhoods.

10. 🏠 Roof Replacement (Asphalt Shingles)

- Cost: $29,136

- Resale Value: $17,807

- ROI: 61.1%

A new roof reassures buyers and can be a deal-maker in competitive markets.

💡 Bonus: Low-Cost Improvements That Make a Big Impact

You don’t need a massive budget to make your home more appealing. Here are affordable upgrades that can still boost value:

1. 🎨 Fresh Paint

Neutral tones like greige, soft white, and light taupe make spaces feel clean and spacious.

2. 💡 Updated Lighting

Swap outdated fixtures for modern, energy-efficient LED lighting.

3. 🧼 Deep Cleaning & Decluttering

A spotless, clutter-free home feels larger and more inviting.

4. 🌿 Landscaping

Trim bushes, plant flowers, and add mulch for instant curb appeal.

5. 🚿 Bathroom Touch-Ups

New faucets, mirrors, and towel bars can modernize a bathroom for under $500.

6. 🪑 Staging

Professional or DIY staging helps buyers visualize living in the space.

🏡 Trending in 2025: Modern Must-Haves for Buyers

Today’s buyers are looking for more than just square footage. Here are features that are hot in 2025:

1. 🖥️ Home Office Space

With remote work here to stay, a dedicated office—or even two—is a major selling point.

2. 🌞 Outdoor Living Areas

Decks, patios, and outdoor kitchens are in high demand for entertaining and relaxation.

3. 🌱 Energy Efficiency

Smart thermostats, solar panels, and heat pumps are attractive for eco-conscious buyers.

4. 🧺 Laundry Room Upgrades

A clean, functional laundry space with storage is a small but mighty value booster.

5. 🧱 Finished Basements

Extra living space for guests, hobbies, or rental income is a huge plus.

📊 How to Prioritize Your Home Improvements

Not sure where to start? Here’s a simple framework:

- Fix what’s broken – Leaky faucets, cracked tiles, and damaged drywall should be addressed first.

- Focus on curb appeal – First impressions matter.

- Update kitchens and baths – These rooms sell homes.

- Add usable space – Finished basements, attics, or ADUs add square footage.

- Think energy efficiency – Lower utility bills = higher buyer interest.

🧠 Pro Tip: Know Your Market

The best improvements vary by location. For example:

- In Cincinnati, buyers may prioritize energy efficiency and finished basements due to seasonal weather.

- In urban areas, smart home features and modern kitchens may carry more weight.

Work with a local real estate expert (like me!) to tailor your upgrades to what buyers in your area want most.

✅ Conclusion: Invest Smart, Sell Smart

Making the right home improvements before selling can lead to a faster sale and a higher price. Focus on projects with high ROI, enhance curb appeal, and don’t overlook affordable upgrades that make a big impact.

Whether you’re planning to sell in six months or six years, these improvements will not only increase your home’s value—they’ll make it a more enjoyable place to live in the meantime.

📣 Ready to Sell? Let’s Talk!

Hi, I’m Mike McEntush, your local real estate expert in Cincinnati, OH. If you’re thinking about selling your home and want personalized advice on which upgrades will give you the best return, I’m here to help!

📞 Contact me today for a free home evaluation and improvement consultation. Let’s get your home market-ready—and sold for top dollar! 💼

#HomeImprovement, #RealEstateTips, #SellYourHome, #HomeValue, #CurbAppeal, #KitchenRemodel, #BathroomRemodel, #HomeStaging, #RealEstate2025, #SmartHome, #EnergyEfficient, #CincinnatiRealEstate, #MikeMcEntushRealtor, #HomeSellingTips, #ROIUpgrades

Your Step-by-Step Guide to Buying Your First Home

🏡 Your Step-by-Step Guide to Buying Your First Home in 2025

1. Is Homeownership Right for You? 🧐

Before diving into listings, ask yourself:

- Are you financially stable?

- Do you plan to stay in one place for at least 3–5 years?

- Are you ready for the responsibilities of homeownership?

If you answered yes, you’re on the right track!

2. Check Your Financial Health 💰

✅ Review Your Credit Score

Aim for a score of 620+ for conventional loans. FHA loans may accept lower scores, but higher scores = better rates.

✅ Calculate Your Debt-to-Income Ratio (DTI)

Lenders prefer a DTI under 43%. Use this formula:

DTI = (Monthly Debt Payments / Gross Monthly Income) × 100

✅ Save for a Down Payment

Typical down payments range from 3% to 20%. Don’t forget closing costs (2–5% of the home price).

3. Understand Your Mortgage Options 🏦

🏠 Fixed-Rate Mortgage

- Interest rate stays the same

- Predictable monthly payments

🏠 Adjustable-Rate Mortgage (ARM)

- Lower initial rate

- Can increase over time

🏠 Government-Backed Loans

- FHA: Low down payment, flexible credit

- VA: For veterans, no down payment

- USDA: For rural areas, low-income buyers

4. Get Pre-Approved 📄

A pre-approval letter shows sellers you’re serious. It also helps you:

- Set a realistic budget

- Speed up the buying process

5. Find the Right Real Estate Agent 🧑💼

Look for an agent who:

- Specializes in first-time buyers

- Knows your local market

- Communicates clearly and often

Ask for referrals or check online reviews.

6. Start House Hunting 🔍

🗺️ Consider:

- Commute times

- School districts

- Safety and amenities

🏘️ Tour Homes

Take notes, photos, and videos. Don’t rush—this is a big decision!

7. Make an Offer ✍️

Your agent will help you:

- Determine a fair price

- Include contingencies (inspection, financing, etc.)

- Negotiate with the seller

Once accepted, you’ll enter escrow—a holding period before closing.

8. Schedule a Home Inspection 🔎

A licensed inspector checks for:

- Structural issues

- Plumbing/electrical problems

- Roof and HVAC condition

If issues arise, you can renegotiate or walk away.

9. Secure Financing 💳

Submit your loan application with:

- Pay stubs

- Tax returns

- Bank statements

Your lender will order an appraisal to ensure the home’s value matches the loan amount.

10. Close the Deal 🖊️

🧾 Final Steps:

- Review the Closing Disclosure

- Do a final walkthrough

- Sign the paperwork

You’ll pay closing costs and receive the keys—congrats, homeowner! 🎉

11. Move In and Celebrate! 🎈

Change your address, set up utilities, and start making your house a home. Don’t forget to:

- Create a maintenance schedule

- Build an emergency fund

- Enjoy your new space!

12. Conclusion 🏁

Buying your first home is a journey filled with excitement, learning, and big decisions. By following this step-by-step guide, you’ll be equipped to make informed choices and avoid common pitfalls. The 2025 housing market offers plenty of opportunities for first-time buyers, and with the right preparation, you can turn your dream of homeownership into reality. 🏡💪

Remember, every step you take brings you closer to the front door of your future home. Stay patient, stay informed, and don’t hesitate to ask for help when you need it.

Ready to take the first step toward homeownership?

Let’s chat about your goals and how I can help you find the perfect place to call home. Whether you’re just starting or ready to tour homes, I’m here to guide you every step of the way.

Let’s make your dream home a reality! 🏡✨

#FirstTimeHomeBuyer, #HomeBuyingTips, #RealEstate2025, #MortgageAdvice, #HouseHunting, #HomeSweetHome, #RealEstateGoals, #BuyAHome, #CincinnatiRealEstate, #DreamHome, #HomeOwnership, #RealEstateExpert, #NewHomeJourney

Selling an Inherited Property: What You Need to Know

🏡 Selling an Inherited Property: What You Need to Know

Inheriting property can be both a blessing and a challenge. Whether it’s a cherished family home or a piece of land, selling inherited real estate involves legal, financial, and emotional considerations. This guide will walk you through everything you need to know to make informed decisions and maximize your outcome.

🧾 Step 1: Understand the Legal Process

What is Probate?

Probate is the legal process of validating a will and distributing the deceased’s assets. If the property was solely owned by the deceased, it likely must go through probate unless it was held in a trust or jointly owned.

Key Documents You’ll Need:

- Death certificate

- Will or trust documents

- Letters testamentary (court authorization)

- Property deed

Tip: Consult a probate attorney to ensure compliance with Ohio state laws.

💰 Step 2: Know the Tax Implications

Capital Gains Tax

Inherited property benefits from a stepped-up basis, meaning the property’s value is adjusted to its fair market value at the time of the decedent’s death. This significantly reduces capital gains tax when you sell.

Example:

- Original purchase price: $200,000

- Value at inheritance: $500,000

- Sale price: $550,000

- Taxable gain: $50,000 (not $350,000)

Other Taxes to Consider

- Estate Tax: Only applies to estates over $13.61 million (2024 threshold).

- Inheritance Tax: Rare, but applicable in six states (not Ohio).

- Net Investment Income Tax: May apply to high-income earners.

Tip: Keep records of appraisals, improvements, and selling expenses to reduce taxable gains.

🛠️ Step 3: Prepare the Property for Sale

Assess the Condition

Inherited homes may need repairs or updates. Consider:

- Cleaning and decluttering

- Minor renovations (paint, flooring)

- Landscaping for curb appeal

Get an Appraisal

An appraisal helps determine the fair market value and supports your tax documentation.

Decide to Sell As-Is or Renovate

Selling “as-is” can be faster but may yield a lower price. Renovating can increase value but requires time and investment.

👨👩👧👦 Step 4: Navigate Family Dynamics

Selling inherited property often involves multiple heirs. Clear communication is key.

Tips for Managing Family Involvement:

- Hold a family meeting

- Agree on a sales strategy

- Use a neutral third party (e.g., attorney or mediator)

📈 Step 5: Market and Sell the Property

Work with a Real Estate Agent

Choose an agent experienced in inherited properties. They can:

- Price the home accurately

- Market effectively

- Handle negotiations

Selling Options

- Traditional Sale: Best for maximizing value

- Cash Buyer: Fast but may offer less

- Auction: Useful for unique or hard-to-value properties

📋 Step 6: Finalize the Sale

Closing Process

At closing, ensure:

- All heirs sign necessary documents

- Title is clear

- Funds are distributed properly

Reporting to the IRS

Use Schedule D of Form 1040 to report the sale. Include:

- Sale price

- Adjusted basis

- Selling expenses

🧠 Pro Tips for a Smooth Sale

- Consult Professionals: Attorney, CPA, and real estate agent

- Document Everything: Keep receipts, appraisals, and legal paperwork

- Plan Ahead: Consider timing for tax purposes and market conditions

✅ Conclusion

Selling an inherited property doesn’t have to be overwhelming. With the right knowledge, professional support, and a clear plan, you can turn a complex situation into a successful transaction. Whether you’re dealing with probate, navigating family dynamics, or optimizing your tax position, taking thoughtful steps will help you protect your interests and honor your loved one’s legacy.

Need help selling an inherited property in Cincinnati or beyond? Contact Mike McEntush today for personalized advice and expert support. 📞

👉 Schedule your consultation now and make your next move with confidence!

#realestate, #inheritance, #propertysale, #probate, #capitalgains, #homeforsale, #realestatetips, #sellingahome, #estateplanning, #realestateagent, #propertymarket, #homevalue, #realestateguide, #taxplanning, #realestateinvesting

Buying a Home as a Single Parent: Your Empowering Guide to Homeownership

🏡 Buying a Home as a Single Parent: Your Empowering Guide to Homeownership 💪

Being a single parent is a journey filled with love, resilience, and determination. 🧡 When it comes to buying a home, the process can feel overwhelming—but guess what? You’ve got this! 🎯 Whether you’re dreaming of a cozy condo or a spacious house with a backyard for the kids, homeownership is absolutely within reach.

💡 Why Homeownership Matters for Single Parents

Owning a home provides stability, financial growth, and a sense of pride. For single parents, it’s more than just a roof over your head—it’s a legacy for your children. 🏠✨

Benefits Include:

- Stability for your family 🛏️

- Building equity over time 📈

- Freedom to customize your space 🎨

- Potential tax benefits 💰

📝 Tips for Buying a Home as a Single Parent

1. Know Your Budget

Start by reviewing your income, expenses, and credit score. Use online mortgage calculators to estimate what you can afford. 💳📊

2. Explore Assistance Programs

Many states offer down payment assistance, grants, and special loan programs for single parents. 🏦 Check with local housing authorities or nonprofit organizations.

3. Get Pre-Approved

A mortgage pre-approval gives you a clear idea of your buying power and shows sellers you’re serious. ✅

4. Work with a Trusted Realtor

Find a real estate agent who understands your unique needs and can guide you through the process with empathy and expertise. 🤝

5. Think Long-Term

Choose a home that fits your current lifestyle and future goals. Consider school districts, commute times, and neighborhood safety. 🏫🚗

6. Build a Support Team

From realtors to mortgage brokers to family and friends—don’t hesitate to ask for help. You don’t have to do this alone. 🧑🤝🧑

7. Consider Future Expenses

Factor in property taxes, maintenance, utilities, and insurance. Planning ahead helps avoid surprises. 🧾🔧

8. Look for Kid-Friendly Features

Think about fenced yards, nearby parks, and safe streets. Your kids’ comfort and safety matter. 🛝👶

9. Stay Organized

Keep all your documents—pay stubs, tax returns, bank statements—in one place. It’ll make the mortgage process smoother. 📂🖇️

10. Don’t Rush

Take your time to find the right home. It’s okay to wait for the one that truly fits your family’s needs. ⏳❤️

🛠️ Common Challenges & How to Overcome Them

- Limited Time? Use virtual tours and weekend open houses.

- Tight Budget? Look into FHA loans or USDA rural housing programs.

- Feeling Overwhelmed? Lean on your support network and professionals.

🎉 Conclusion: You’re Not Alone in This Journey

Buying a home as a single parent may come with unique challenges, but it’s also an incredibly empowering experience. With the right resources, mindset, and support, you can create a safe and loving space for your family to thrive. 🌟

📣 Ready to Take the First Step?

Let’s make your dream of homeownership a reality! Contact a local real estate expert today or explore assistance programs in your area. Your future home is waiting! 🏡💼

#HomeBuyingTips, #SingleParentLife, #RealEstateAdvice, #FirstTimeHomeBuyer, #HomeGoals, #HouseHunting, #MortgageHelp, #RealEstateSupport, #FamilyHome, #HomeOwnershipJourney

How to Downsize Without the Stress (or the Meltdowns)

How to Downsize Without the Stress (or the Meltdowns): A 2025 Guide to Simplifying Your Space and Sanity

So, you’ve decided to downsize. Maybe the kids have flown the coop, or maybe you’re just tired of dusting 14 decorative vases you don’t even like. Whatever your reason, welcome to the wonderful world of less stuff, more life.

But let’s be honest—downsizing can feel like trying to solve a Rubik’s Cube blindfolded… while riding a unicycle… during a windstorm. 😅

Fear not! This guide will walk you through how to downsize without losing your mind (or your favorite coffee mug). Let’s declutter your space and your stress.

🧭 Step 1: Define Your “Why” (Before You Touch a Single Box)

Before you start tossing things into donation bins like a game show contestant, take a moment to ask yourself: Why am I downsizing?

- Are you looking to save money?

- Want to simplify your lifestyle?

- Moving closer to family?

- Tired of vacuuming rooms you never use?

Knowing your “why” gives you clarity and motivation when the going gets tough (like when you’re deciding whether to keep that fondue set from 1987).

🧠 Pro Tip: Write your “why” on a sticky note and slap it on the fridge. You’ll need the reminder when you’re knee-deep in old tax returns and mystery cables.

📏 Step 2: Measure Twice, Move Once

Before you even think about what to keep, know your new space. Measure every room, closet, and cabinet. Then measure your furniture. Then measure it again.

You don’t want to arrive at your new condo only to discover your beloved sectional sofa is now a wall-to-wall obstacle course.

🎯 Reality Check: If your new living room is the size of your old walk-in closet, it’s time to say goodbye to the 12-piece entertainment center.

🧹 Step 3: Declutter Like a Ninja (With a Sense of Humor)

Decluttering is the heart of downsizing. But it doesn’t have to be a soul-crushing slog. Here’s how to make it manageable—and maybe even fun:

🗂️ Use the 3-Box Method:

- Keep – You love it, use it, or it sparks joy (thanks, Marie Kondo).

- Donate/Sell – It’s useful, but not to you.

- Trash/Recycle – It’s broken, expired, or just plain weird.

🧦 Bonus Round: If you find socks without partners, congratulate them on their independence and let them go.

🧸 Step 4: Handle Sentimental Items With Care (and a Timer)

Ah yes, the emotional landmines: baby clothes, wedding invites, your kid’s macaroni art from 1998. These items are the hardest to part with.

🕰️ Try the “Memory Box” Rule:

Limit yourself to one box per person for sentimental items. If it doesn’t fit, it doesn’t stay.

😢 Tough Love Tip: You’re not throwing away the memory—you’re just making space for new ones.

📦 Step 5: Start Early, Start Small

Downsizing is not a weekend project. It’s a journey. Start at least 6–12 months before your move if possible.

🧩 Begin with:

- The garage (aka the land of forgotten tools)

- The guest room (aka the junk room)

- The linen closet (do you really need 27 towels?)

🐢 Slow and Steady: One drawer a day keeps the panic away.

💻 Step 6: Digitize Everything You Can

Paper takes up space. And let’s be honest, you haven’t looked at that 2003 electric bill since… 2003.

📲 Scan and store:

- Tax documents

- Medical records

- Warranties

- Old photos (bonus: you can share them with family!)

📁 Digital Zen: Your filing cabinet just became a flash drive.

🛋️ Step 7: Sell, Donate, or Gift (But Don’t Hoard)

Once you’ve sorted your stuff, it’s time to let it go (cue Elsa 🎶).

💸 Sell:

- Furniture

- Electronics

- Collectibles

❤️ Donate:

- Clothes

- Kitchenware

- Books

🎁 Gift:

- Family heirlooms

- Sentimental items to loved ones

🧙♂️ Magic Trick: If you haven’t used it in a year, it’s probably not essential.

🚚 Step 8: Hire Help (Because You’re Not a Superhero)

You don’t have to do this alone. Consider hiring:

- Professional organizers

- Downsizing specialists

- Movers who also pack

- Therapists (kidding… kind of)

💪 Outsource the Overwhelm: Your back—and your sanity—will thank you.

🧘 Step 9: Embrace the Emotional Rollercoaster

Downsizing isn’t just physical—it’s emotional. You’re saying goodbye to a chapter of your life.

😢 Expect:

- Nostalgia

- Guilt

- Relief

- Excitement

🧡 Feel it all. Then remind yourself: you’re not losing space—you’re gaining freedom.

🏡 Step 10: Celebrate Your New Chapter

Once you’re in your new space, take a moment to breathe. Light a candle. Order takeout. Dance in your clutter-free living room.

You did it. You downsized without losing your mind (or your cat). 🎉

🧭 Less Stuff, More Life

Downsizing isn’t about giving things up—it’s about making room for what matters most. Whether that’s travel, family, hobbies, or just not tripping over a rogue ottoman, you’re creating a life that fits you better.

So go ahead—let go of the waffle maker you haven’t used since 2011. Your future self (and your countertops) will thank you.

Ready to Downsize Without the Drama?

If you’re thinking about downsizing and want a real estate expert who gets it, I’m here to help! Whether you need help finding the perfect smaller home, selling your current one, or just want to vent about your Tupperware situation—I’ve got your back.

#Downsizing, #MinimalistLiving, #DeclutterYourLife, #RealEstateTips, #HomeSelling, #MovingTips, #SimplifyYourLife, #SeniorLiving, #EmptyNester, #HomeOrganization, #RealEstateHumor, #StressFreeMoving, #SmallSpaceLiving, #HomeGoals, #RealEstateExpert

🏡 How the Big Beautiful Bill Benefits Home Buyers and Sellers in 2025 and Beyond

🏡 How the Big Beautiful Bill Benefits Home Buyers and Sellers in 2025 and Beyond

1. 🏛️ Introduction: Why This Bill Matters

The Big Beautiful Bill is one of the most comprehensive housing-focused legislative packages in recent history. It addresses long-standing affordability issues, modernizes tax incentives, and encourages sustainable development. For anyone involved in real estate, this bill is more than just policy—it’s a roadmap to smarter, more profitable decisions.

2. 🏠 Key Benefits for Home Buyers

✅ $12,500 First-Time Homebuyer Tax Credit

One of the most exciting provisions is a refundable $12,500 tax credit for qualifying first-time homebuyers

✅ Increased FHA Loan Limits

FHA loan limits have been raised by approximately 10%, making it easier for middle-income buyers to qualify for homes in high-cost areas

✅ Lower Barriers to Entry

With expanded access to VA and USDA loans, more Americans—especially veterans and rural residents—can now enter the housing market with zero down payment options.

3. 💰 Major Wins for Home Sellers

✅ Higher Mortgage Interest Deduction Cap

The mortgage interest deduction cap has been raised from $750,000 to $1 million, making high-value homes more attractive to buyers and increasing demand in luxury markets

✅ SALT Deduction Cap Increased

The State and Local Tax (SALT) deduction cap has been lifted from $10,000 to $20,000 for joint filers, benefiting sellers in high-tax states by making their properties more appealing to buyers

✅ Capital Gains Exclusion Maintained

The bill preserves the $250k/$500k capital gains exclusion for primary residences, allowing sellers to keep more of their profits.

4. 📊 Tax Incentives and Credits Explained

✅ 100% Bonus Depreciation (Now Permanent)

Investors and homeowners can now deduct 100% of the cost of short-lived assets (like HVAC, lighting, and flooring) in the first year

✅ §179D Deduction Extended

This deduction, which rewards energy-efficient commercial construction, is now extended through 2026 with a higher cap of $5.81 per square foot

✅ §45L Residential Energy Credit

Homebuilders can earn up to $5,000 per unit for constructing energy-efficient homes that meet DOE Zero Energy Ready standards

5. 🌱 Energy Efficiency and Green Building Perks

The bill strongly encourages sustainable development:

- Builders and developers are incentivized to use green materials and energy-efficient designs.

- Homeowners who upgrade to solar panels, smart thermostats, or energy-efficient windows may qualify for additional tax credits.

- These upgrades not only reduce utility bills but also increase property value.

6. 📉 Mortgage and Lending Market Changes

✅ Stabilized Mortgage Rates

While the bill includes federal spending that may delay interest rate cuts, it also introduces rate stabilization mechanisms to prevent sharp increases

✅ Easier Refinancing

Homeowners can now refinance under streamlined FHA and VA programs, reducing monthly payments and freeing up cash for other investments.

7. 🌍 Regional and Equity Impacts

The bill includes provisions to:

- Expand housing supply in underserved urban and rural areas.

- Provide grants to local governments for zoning reform and infrastructure upgrades.

- Address racial and economic disparities in homeownership through targeted assistance programs.

8. 🏢 What This Means for Real Estate Investors

✅ New Depreciation Rules

While the bill tightens rules on 1031 exchanges, it also introduces Qualified Production Property (QPP) incentives for domestic manufacturing and industrial real estate

✅ More Predictable Tax Planning

With permanent bonus depreciation and extended credits, investors can now plan long-term with greater confidence.

9. 📝 Action Steps for Buyers and Sellers

For Buyers:

- Check eligibility for the $12,500 tax credit.

- Get pre-approved under the new FHA/VA limits.

- Explore energy-efficient homes for added tax benefits.

For Sellers:

- Highlight energy upgrades in your listings.

- Time your sale to maximize capital gains exclusions.

- Work with a tax advisor to leverage new deductions.

10. 🧠 Final Thoughts + CTA

The Big Beautiful Bill is more than just a legislative win—it’s a strategic opportunity for anyone involved in real estate. Whether you’re buying your first home, selling a long-held property, or investing in rental units, this bill gives you the tools to save money, build wealth, and make smarter decisions.

📣 Ready to Take Advantage of the Big Beautiful Bill?

Let’s talk about how you can maximize your benefits under the new law. Whether you’re buying, selling, or investing, I’m here to help you navigate the market with confidence.

👉 Contact me today to schedule a free consultation and start your real estate journey the smart way!

#BigBeautifulBill, #HomeBuying2025, #RealEstateTips, #FirstTimeHomeBuyer, #FHAloans, #TaxCredits, #HomeSellers, #RealEstateInvesting, #GreenHomes, #MortgageTips, #HousingMarket2025, #EnergyEfficientHomes, #RealEstateNews, #PropertyTaxSavings, #HomeownershipGoals

How to Buy a Fixer-Upper Without Regret (or Losing Your Mind)

🛠️ How to Buy a Fixer-Upper Without Regret (or Losing Your Mind) 🏚️➡️🏡

So, you’ve binge-watched Fixer Upper, Property Brothers, and Love It or List It, and now you’re convinced you can turn a crumbling shack into a Pinterest-worthy palace. First of all—bless your brave, optimistic heart. Second of all—let’s make sure you don’t end up crying into a pile of drywall dust.

Buying a fixer-upper can be a dream come true—or a nightmare with a mortgage. But don’t worry, I’ve got your back with this hilarious, helpful, and heartbreak-preventing guide to buying a fixer-upper without regret.

🧠 Step 1: Know Thyself (and Thy Budget)

Before you even look at a single listing, ask yourself:

- Do I have the patience of a saint?

- Can I handle unexpected expenses without sobbing?

- Do I know the difference between a stud and a joist? (No, not that kind of stud. 😏)

If you answered “no” to all of the above, that’s okay! You can still buy a fixer-upper—you just need to budget for professionals.

💸 Budgeting Tips:

- Purchase price: Keep it low enough to leave room for renovations.

- Renovation costs: Add 20–30% more than you think you’ll need. Trust me.

- Emergency fund: Because something will go wrong. It’s the law of fixer-uppers.

🏚️ Step 2: Find the Right Kind of Ugly

Not all fixer-uppers are created equal. Some are diamonds in the rough. Others are just…rough.

Look for:

✅ Solid foundation

✅ Good roof (or at least not a terrible one)

✅ Functional layout

✅ Homes in up-and-coming neighborhoods

Avoid:

❌ Foundation issues (unless you’re secretly a structural engineer)

❌ Mold, termites, or haunted basements

❌ Homes that smell like regret and raccoons

🕵️♀️ Step 3: Get a Home Inspection (Seriously, Don’t Skip This)

You wouldn’t buy a used car without popping the hood, right? Same goes for houses.

A licensed home inspector will check:

- Electrical systems ⚡

- Plumbing 🚿

- HVAC 🌀

- Roof and attic 🏠

- Foundation and structure 🧱

Pro tip: Attend the inspection and ask questions. Bring snacks. It’s a long day.

🧰 Step 4: Know What You Can DIY (and What You Shouldn’t)

Sure, you can paint a wall. Maybe even install a backsplash. But rewiring the house? That’s a hard no unless your name is Bob Vila.

DIY-Friendly:

- Painting 🎨

- Landscaping 🌿

- Installing shelves 🪜

Call a Pro For:

- Electrical work ⚠️

- Plumbing 🚽

- Structural changes 🏗️

Remember: YouTube tutorials are great, but they won’t save you from a flooded basement.

🏗️ Step 5: Create a Renovation Plan (and Stick to It…Mostly)

Renovating without a plan is like grocery shopping hungry—you’ll end up with a bunch of stuff you don’t need and no money left.

Your Plan Should Include:

- A prioritized list of projects

- A realistic timeline

- A detailed budget

- A backup plan for when things go sideways (because they will)

Bonus tip: Don’t renovate everything at once unless you enjoy chaos and living in a dust cloud.

🧾 Step 6: Financing Your Fixer-Upper

You’ve got options, my friend:

🏦 Loan Types:

- FHA 203(k) Loan: Great for first-time buyers. Covers purchase + reno.

- Fannie Mae HomeStyle Loan: More flexible, but stricter credit requirements.

- Personal Loan or HELOC: If you already own a home.

Talk to a mortgage broker who gets fixer-uppers. Not all lenders do.

🧱 Step 7: Expect the Unexpected (and Laugh Through It)

Your contractor will find knob-and-tube wiring. Your “quick” bathroom reno will take 3 months. Your dog will step in wet cement.

It’s all part of the journey.

Keep Your Sanity By:

- Taking before-and-after photos 📸

- Celebrating small wins (like finally having a working toilet 🚽)

- Keeping a sense of humor (and maybe a bottle of wine 🍷)

🛋️ Step 8: Don’t Over-Renovate

You’re not building the Taj Mahal. You’re fixing up a house to live in or flip—not to win a design award.

Avoid:

- Over-customizing (no one else wants a medieval dungeon-themed bathroom)

- Overspending for the neighborhood

- Adding features you won’t use (do you really need a wine cellar?)

🧠 Step 9: Learn From Others’ Mistakes

Here are some real-life horror stories (names changed to protect the embarrassed):

- “Tilegate”: Sarah ordered 300 sq ft of tile…in the wrong color. She cried. Then she sold it on Facebook Marketplace.

- “The Great Bathtub Debacle”: Mike installed a clawfoot tub upstairs. It fell through the floor. Insurance was…not amused.

- “Paintpocalypse”: Jenna painted her entire living room “Trendy Taupe.” It dried to “Sad Beige.” She repainted. Twice.

🏁 Step 10: Enjoy the Transformation

There’s nothing like seeing your vision come to life. That moment when the last cabinet is hung, the last lightbulb is screwed in, and you can finally sit on your couch without a layer of dust? Pure bliss.

Take a deep breath. You did it. You survived the fixer-upper journey—and you didn’t even cry (much).

🎯 Final Thoughts: Should You Buy a Fixer-Upper?

If you’re:

- Patient

- Budget-conscious

- Not afraid of a little chaos

- Willing to laugh through the madness

Then YES. A fixer-upper can be a smart investment and a rewarding experience.

If you’re:

- Easily stressed

- Short on time or money

- Hoping for instant gratification

Maybe stick to move-in ready. No shame in that game.

📣 Ready to Find Your Perfect Fixer-Upper?

Whether you’re dreaming of a cozy cottage or a bold bungalow, I can help you find a fixer-upper that won’t break your heart (or your bank account).

👉 Let’s chat! Contact me today and let’s turn your renovation dreams into reality. 🛠️🏡

#FixerUpper, #HomeRenovation, #RealEstateTips, #FirstTimeHomeBuyer, #HouseHunting, #RenovationJourney, #DIYHome, #PropertyInvestment, #RealEstateHumor, #HomeImprovement, #BeforeAndAfter, #DreamHome, #RealEstateLife, #HomeGoals, #CurbAppeal

🏡 What is the MLS and Why it Matters in Real Estate

🏡 What is the MLS and Why it Matters in Real Estate

Whether you’re buying your first home, selling a property, or just curious about how real estate works behind the scenes, you’ve likely heard the term MLS tossed around. But what exactly is the Multiple Listing Service, and why is it such a big deal in the real estate world?

In this in-depth guide, we’ll break down what the MLS is, how it works, why it matters to buyers and sellers, and how it shapes the modern real estate market. Let’s dive in! 🏊♂️

📌 What is the MLS?

The Multiple Listing Service (MLS) is a cooperative database used by real estate brokers to share information about properties for sale. It’s not a single national system, but rather a network of regional databases—as of 2025, there are over 500 MLSs in the U.S. alone

Each MLS is a private platform accessible only to licensed real estate professionals who are members. These professionals use the MLS to:

- List homes for sale

- Share detailed property information

- Offer compensation to other agents

- Facilitate cooperation between buyer and seller agents

The MLS is the backbone of real estate transactions, ensuring transparency, accuracy, and efficiency in the marketplace.

🧠 A Brief History of the MLS

The concept of the MLS dates back to the late 1800s, when real estate brokers would gather in person to exchange information about properties they were trying to sell. They agreed to cooperate and compensate each other for helping close deals—a principle that still underpins the MLS today

Over time, this informal system evolved into a digital network of databases, governed by local real estate associations and powered by standardized data formats like the RESO Data Dictionary

🧩 How the MLS Works

Here’s a simplified breakdown of how the MLS functions:

- Listing a Property: A seller hires a real estate agent, who enters the property details into the local MLS.

- Data Sharing: The listing becomes visible to all other agents in that MLS, who can then share it with their buyer clients.

- Cooperation & Compensation: The listing agent offers a commission to any buyer’s agent who brings a successful offer.

- Search & Match: Buyer’s agents use the MLS to search for homes that match their clients’ criteria.

- Transaction: Once a match is made, the agents work together to close the deal.

This system ensures maximum exposure for sellers and comprehensive access for buyers.

🔍 What’s Included in an MLS Listing?

MLS listings are far more detailed than what you’ll find on public real estate websites. A typical MLS entry includes:

- High-resolution photos 📸

- Property description 🏠

- Square footage and lot size 📏

- Year built 🛠️

- Number of bedrooms and bathrooms 🛏️🛁

- School district info 🎓

- HOA fees and restrictions 💰

- Showing instructions 📅

- Agent remarks (not visible to the public) 🗒️

This rich dataset helps agents and their clients make informed decisions.

🧭 Why the MLS Matters for Buyers

If you’re buying a home, the MLS is your secret weapon—even if you don’t access it directly.

✅ Comprehensive Listings

The MLS includes nearly every home for sale in a given area, including those that may not appear on public sites like Zillow or Realtor.com.

✅ Real-Time Updates

Unlike third-party platforms, MLS data is updated in real time, so you’re less likely to fall in love with a home that’s already under contract.

✅ Professional Guidance

Your agent uses the MLS to filter listings, schedule showings, and compare properties—saving you time and stress.

💰 Why the MLS Matters for Sellers

If you’re selling your home, the MLS is your most powerful marketing tool.

✅ Maximum Exposure

Your listing is instantly shared with hundreds or thousands of agents, each with their own pool of buyers.

✅ Faster Sales

Homes listed on the MLS tend to sell faster and for more money, thanks to increased visibility and competition.

✅ Professional Presentation

MLS listings follow strict formatting and photo guidelines, ensuring your home is presented in the best possible light.

🤝 Why the MLS Matters for Agents

For real estate professionals, the MLS is mission-critical.

- It’s the primary source of inventory

- It facilitates cooperation and compensation

- It provides market data and analytics

- It ensures compliance with local rules and ethics

Agents who are members of an MLS are held to higher standards, which benefits everyone involved.

🌐 MLS vs. Zillow, Redfin, and Realtor.com

You might be wondering: “Why do I need the MLS when I can just browse homes online?”

Here’s the difference:

| Feature | MLS | Zillow/Redfin/Realtor |

|---|---|---|

| Accuracy | ✅ High | ❌ Often outdated |

| Listing Source | Direct from agents | Aggregated from MLS |

| Update Frequency | Real-time | Delayed |

| Full Details | ✅ Yes | ❌ Limited |

| Agent Tools | ✅ Yes | ❌ No |

🛠️ MLS Technology and Innovation

Modern MLS systems are powered by cutting-edge tech, including:

- RESO Web API for seamless data sharing

- AI-powered search tools for smarter matching

- Mobile apps for on-the-go access

- Virtual tours and 3D walkthroughs

These innovations make the MLS more accessible and user-friendly than ever before.

🌍 The Future of the MLS

The MLS landscape is evolving rapidly:

- Consolidation: Smaller MLSs are merging into larger regional platforms for better efficiency.

- Global Expansion: MLSs are emerging in Mexico, Europe, and Asia

.

- Consumer Access: Some MLSs are experimenting with direct-to-consumer portals.

- Data Transparency: New rules are making MLS data more open and standardized.

The goal? A more connected, transparent, and equitable real estate market.

🧠 Common Myths About the MLS

Let’s bust a few misconceptions:

- ❌ “Only agents can benefit from the MLS.”

✅ Buyers and sellers benefit the most—agents are just the facilitators. - ❌ “The MLS is just a website.”

✅ It’s a cooperative network with strict rules and standards. - ❌ “All MLSs are the same.”

✅ Each MLS has its own rules, coverage area, and technology.

📣 Final Thoughts: Why the MLS Still Matters

In an age of apps and algorithms, the MLS remains the most trusted, accurate, and powerful tool in real estate. It’s the engine that drives the market, connecting buyers, sellers, and agents in a system built on cooperation and transparency.

Whether you’re buying, selling, or just exploring, understanding the MLS gives you a competitive edge.

🚀 Ready to Buy or Sell? Let’s Talk!

If you’re thinking about making a move, I’d love to help you navigate the process with confidence. As a licensed real estate professional with full MLS access, I can:

✅ Find hidden gems before they hit public sites

✅ Market your home to thousands of agents and buyers

✅ Guide you through every step of the transaction

Let’s make your real estate dreams a reality! 🏡✨

#realestate, #realtor, #homesforsale, #househunting, #dreamhome, #realestatelife, #justlisted, #openhouse, #realestateagent, #homebuying, #homesweethome, #propertyforsale, #mls, #realestatetips, #firsttimehomebuyer

What to Expect During a Home Appraisal in 2025: A Complete Guide

🏡 What to Expect During a Home Appraisal in 2025: A Complete Guide

Buying or selling a home is one of the most significant financial decisions you’ll ever make. One crucial step in this process is the home appraisal—a professional evaluation of a property’s market value. Whether you’re a first-time buyer, a seasoned investor, or a homeowner looking to refinance, understanding what to expect during a home appraisal can help you prepare and avoid surprises.

In this guide, we’ll walk you through:

- What a home appraisal is

- Why it matters

- What appraisers look for

- How to prepare

- What happens after the appraisal

- 2025 updates to the appraisal process

- Common myths and FAQs

Let’s dive in! 🏊♂️

🧾 What Is a Home Appraisal?

A home appraisal is an unbiased estimate of a property’s fair market value, conducted by a licensed appraiser. Mortgage lenders require appraisals to ensure they’re not lending more than the home is worth. This protects both the lender and the buyer from overpaying.

🔍 When Do You Need an Appraisal?

- Buying a home (required by lenders)

- Refinancing a mortgage

- Selling a home (to set a competitive price)

- Home equity loans or lines of credit

🛠️ What Appraisers Look for During a Home Appraisal

Appraisers evaluate both the interior and exterior of the home, as well as comparable sales in the area. Here’s what they focus on:

1. 🏠 Property Size and Layout

- Square footage

- Number of bedrooms and bathrooms

- Functional layout

2. 🧱 Structural Integrity

- Foundation condition

- Roof age and quality

- Walls, ceilings, and floors

3. 🛋️ Interior Features

- Flooring, cabinetry, countertops

- Appliances and fixtures

- HVAC systems

4. 🧼 Cleanliness and Maintenance

- General upkeep

- Signs of neglect or damage

5. 🌳 Curb Appeal and Landscaping

- Exterior paint and siding

- Driveway and walkways

- Lawn and garden condition

6. 📍 Location and Neighborhood

- School district

- Proximity to amenities

- Crime rates and desirability

7. 📊 Comparable Sales (Comps)

- Recent sales of similar homes nearby

- Adjustments for differences in features

🧠 2025 Appraisal Updates You Should Know

The appraisal process has evolved significantly in 2025, thanks to technology and regulatory changes:

🔄 Dynamic UAD Reports

The Uniform Appraisal Dataset (UAD) has been overhauled. Reports are now dynamic and tailored to each property type, making them more accurate and easier to understand.

🤖 AI-Assisted Appraisals

Artificial Intelligence is now used to analyze market data and property features, helping appraisers make more informed decisions.

📱 Digital Tools in the Field

Appraisers now use tablets and mobile apps to collect data, improving speed and accuracy.

🧾 Expanded Comment Sections

Reports now include detailed, expandable comment sections, reducing the need for separate addendums.

🧹 How to Prepare for a Home Appraisal

Want to get the best possible valuation? Here’s how to prepare:

✅ 1. Clean and Declutter

A tidy home makes a great first impression.

🔧 2. Make Minor Repairs

Fix leaky faucets, squeaky doors, and chipped paint.

🌿 3. Boost Curb Appeal

Mow the lawn, trim bushes, and clean the exterior.

📄 4. Provide a List of Upgrades

Include dates and costs of renovations or improvements.

🐶 5. Secure Pets

Keep pets out of the way to avoid distractions.

⏱️ How Long Does a Home Appraisal Take?

- On-site inspection: 30 minutes to 2 hours

- Report delivery: 2 to 7 business days

Factors like property size, complexity, and appraiser workload can affect timing.

📉 What Happens After the Appraisal?

🟢 If the Appraisal Meets or Exceeds the Offer:

- The loan proceeds as planned.

🔴 If the Appraisal Comes in Low:

- Renegotiate the price

- Pay the difference out of pocket

- Request a second appraisal

🧾 Common Appraisal Myths—Busted!

❌ Myth 1: Appraisers Work for the Buyer

Truth: They work for the lender to ensure the loan is sound.

❌ Myth 2: A Clean House Increases Value

Truth: Cleanliness helps presentation but doesn’t directly affect value.

❌ Myth 3: Appraisals and Inspections Are the Same

Truth: Inspections look for problems; appraisals determine value.

💡 Pro Tips for Buyers and Sellers

For Buyers:

- Don’t waive the appraisal contingency unless you’re confident in the value.

- Review the report carefully and ask questions.

For Sellers:

- Price your home realistically based on comps.

- Be presentable and cooperative during the appraisal.

📈 Real Estate Trends Impacting Appraisals in 2025

- Rising interest rates: Affect buyer demand and home values.

- Remote work: Increases demand for suburban and rural properties.

- Green upgrades: Energy-efficient homes may appraise higher.

- Smart home tech: Can add value if properly documented.

📝 Summary

A home appraisal is a vital part of the real estate process. In 2025, it’s more data-driven, tech-enhanced, and transparent than ever before. Whether you’re buying, selling, or refinancing, knowing what to expect—and how to prepare—can make all the difference.

Thinking about buying or selling a home? 🏡 Don’t leave your appraisal to chance! Contact me today for expert guidance, personalized tips, and a smooth real estate experience from start to finish. Let’s make your next move a smart one! 📞📧

#realestate, #homeappraisal, #homebuyingtips, #homesellingtips, #realestatetips, #propertyvalue, #mortgagetips, #realestate2025, #homeinspection, #househunting, #realtorlife, #realestatemarket, #appraisalprocess, #homevalue, #firsttimehomebuyer

How to Make a Competitive Offer in a Hot Market

How to Make a Competitive Offer in a Hot Market

In today’s red-hot real estate market, making a competitive offer isn’t just a good idea—it’s essential. With limited inventory, rising prices, and multiple-offer scenarios becoming the norm, buyers need to be strategic, fast, and well-prepared to win their dream home.

Whether you’re a first-time buyer or a seasoned investor, this guide will walk you through everything you need to know to craft a winning offer in a competitive housing market.

1. Understand the Market You’re In

Before you even think about making an offer, you need to understand the dynamics of your local market. Is it a seller’s market with low inventory and high demand? Are homes selling above asking price? How long are listings staying active?

Tips:

- Use tools like Zillow, Redfin, or Realtor.com to track local trends.

- Look at recent sales data to understand pricing patterns.

- Talk to a local real estate agent who knows the area inside and out.

2. Get Pre-Approved, Not Just Pre-Qualified

A pre-approval letter from a reputable lender shows sellers that you’re serious and financially capable. It’s stronger than a pre-qualification and can give you a competitive edge.

Why it matters:

- It shows you’ve already gone through underwriting.

- It gives you a clear budget.

- It speeds up the closing process.

3. Work With a Skilled Real Estate Agent

In a hot market, having a savvy agent on your side is crucial. They can help you:

- Identify homes before they hit the market.

- Craft a compelling offer.

- Negotiate effectively with the seller’s agent.

Choose an agent who is responsive, experienced in competitive markets, and well-connected in the local area.

4. Act Fast—But Smart

Homes in hot markets can go under contract within days—or even hours. If you find a home you love, don’t wait.

Pro tip:

- Tour homes as soon as they’re listed.

- Be ready to submit an offer quickly.

- Have your documents and financing in order.

5. Make a Strong First Offer

In a competitive market, lowballing is a fast track to rejection. Your first offer should be strong enough to grab the seller’s attention.

Consider:

- Offering at or above asking price.

- Including an escalation clause (more on that below).

- Showing flexibility on closing dates.

6. Include an Escalation Clause

An escalation clause automatically increases your offer if another buyer bids higher, up to a maximum amount.

Example:

“If another offer exceeds mine, I will increase my offer by $2,000 increments up to a maximum of $550,000.”

This keeps you competitive without overpaying unnecessarily.

7. Increase Your Earnest Money Deposit

Earnest money is a deposit that shows you’re serious. In hot markets, offering more than the standard 1–2% can make your offer stand out.

Why it works:

- It signals financial strength.

- It reassures the seller you won’t back out.

8. Limit Contingencies

Contingencies protect buyers but can make your offer less attractive. In a hot market, consider minimizing or waiving some contingencies—carefully.

Common contingencies to consider:

- Inspection: You can waive it, limit it to major issues, or do a pre-inspection.

- Appraisal: Offer to cover the difference if the appraisal comes in low.

- Financing: If you’re confident, waive the financing contingency.

Important: Always consult your agent before waiving any protections.

9. Be Flexible With the Seller’s Timeline

Sometimes, it’s not just about price. Sellers may need a quick close—or more time to move out.

How to win:

- Offer a rent-back agreement.

- Match their preferred closing date.

- Be accommodating with move-out terms.

10. Cover Seller Costs

Offering to pay for things like the seller’s transfer tax, title insurance, or even moving costs can sweeten the deal without raising the sale price.

11. Use a Clean, Simple Offer Package

Make your offer easy to accept. Include:

- A clean, well-written contract.

- All necessary disclosures.

- Proof of funds and pre-approval letter.

12. Be Prepared for a Bidding War

If you’re entering a multiple-offer situation, be ready to compete. Know your max budget and stick to it.

Strategy:

- Use your escalation clause.

- Be emotionally prepared to walk away.

- Have a backup plan.

13. Consider a Non-Refundable Option Fee

In some markets, buyers offer a non-refundable fee to show commitment. This is risky but can be persuasive.

14. Stay Positive and Persistent

You might lose a few homes before you win one. Don’t get discouraged.

Keep in mind:

- Every offer is a learning experience.

- The right home will come along.

- Your agent is your best ally.

Conclusion: Winning in a Hot Market Takes Strategy and Heart

Making a competitive offer in a hot market isn’t just about throwing money at the problem. It’s about preparation, timing, and understanding what sellers value most. By following the strategies above, you’ll be in a strong position to stand out—and win.

Ready to Make Your Move?

If you’re serious about buying in today’s competitive market, don’t go it alone. Let’s work together to craft a winning strategy and find your dream home. Contact me today to get started!

#realestate, #homebuying, #hotmarket, #realestatetips, #competitiveoffer, #househunting, #realestate2025, #buyersmarket, #sellersmarket, #dreamhome, #realestateagent, #propertymarket, #realestatenews, #homegoals, #realestatelife

The Ultimate Guide to Mortgage Types in 2025: Pros, Cons & How to Choose the Right One

🏡 The Ultimate Guide to Mortgage Types in 2025: Pros, Cons & How to Choose the Right One

Buying a home is one of the biggest financial decisions you’ll ever make—and choosing the right mortgage can make or break your experience. With interest rates fluctuating and new loan products emerging, understanding your options in 2025 is more important than ever.

In this guide, we’ll explore the most common mortgage types, their advantages and disadvantages, and how to decide which one fits your financial goals. Whether you’re a first-time buyer, a military veteran, or a seasoned investor, this post is for you!

🔍 Why Mortgage Type Matters

Your mortgage type affects:

- Your monthly payments

- How much interest you’ll pay over time

- Your eligibility based on credit and income

- Your financial flexibility in the future

Let’s dive into the most popular mortgage types in 2025 and break down the pros and cons of each.

🧱 1. Fixed-Rate Mortgage (FRM)

✅ Pros:

- Predictable payments: Your interest rate stays the same for the life of the loan.

- Great for long-term planning: Ideal if you plan to stay in your home for 10+ years.

- Protection from rate hikes: No surprises if market rates rise.

❌ Cons:

- Higher initial rates: Compared to ARMs, fixed rates start higher.

- Less flexibility: If rates drop, you’ll need to refinance to benefit.

Best For:

- Buyers who value stability and plan to stay put.

🔗 Learn more about fixed-rate mortgages

🔄 2. Adjustable-Rate Mortgage (ARM)

✅ Pros:

- Lower initial rates: Great for short-term savings.

- Potential to save: If rates stay low, you could pay less over time.

❌ Cons:

- Uncertainty: Rates can rise, increasing your monthly payment.

- Complex terms: Caps, margins, and indexes can be confusing.

Best For:

- Buyers who plan to move or refinance within a few years.

🔗 Explore how ARMs work

🧮 3. Interest-Only Mortgage

✅ Pros:

- Lower payments initially: You only pay interest for a set period.

- Cash flow flexibility: Ideal if your income is expected to rise.

❌ Cons:

- No equity build-up: You’re not paying down the principal.

- Payment shock: Payments jump when the interest-only period ends.

Best For:

- Investors or high-income earners with variable income.

🔗 Interest-only mortgage explained

🏛️ 4. FHA Loan (Federal Housing Administration)

✅ Pros:

- Low down payment: As little as 3.5%.

- Lenient credit requirements: Great for first-time buyers.

❌ Cons:

- Mortgage insurance required: Adds to monthly costs.

- Loan limits: May not cover high-cost areas.

Best For:

- First-time buyers or those with lower credit scores.

🔗 FHA loan eligibility and benefits

🎖️ 5. VA Loan (Veterans Affairs)

✅ Pros:

- No down payment required.

- No private mortgage insurance (PMI).

- Competitive interest rates.

❌ Cons:

- Eligibility restricted: Only for veterans, active-duty service members, and some spouses.

- Funding fee: May apply upfront.

Best For:

- Eligible military personnel and veterans.

🔗 Check VA loan eligibility

💼 6. USDA Loan (U.S. Department of Agriculture)

✅ Pros:

- Zero down payment.

- Low interest rates.

- Flexible credit guidelines.

❌ Cons:

- Location restrictions: Only for rural and some suburban areas.

- Income limits: Based on household size and location.

Best For:

- Buyers in rural areas with moderate income.

🔗 Find eligible USDA areas

💰 7. Jumbo Loan

✅ Pros:

- Higher loan limits: For luxury or high-cost homes.

- Flexible terms: Fixed or adjustable options.

❌ Cons:

- Stricter requirements: Higher credit scores and larger down payments.

- Higher interest rates: Compared to conforming loans.

Best For:

- Buyers purchasing high-value properties.

🔗 Jumbo loan basics

🧾 8. Non-QM Loans (Non-Qualified Mortgages)

✅ Pros:

- Flexible documentation: Great for self-employed or gig workers.

- Alternative income verification.

❌ Cons:

- Higher interest rates.

- Less regulation: May carry more risk.

Best For:

- Buyers with non-traditional income or unique financial situations.

🔗 What is a Non-QM loan?

🧠 How to Choose the Right Mortgage Type

Here are a few questions to ask yourself:

- How long do I plan to stay in the home?

- What’s my credit score and income stability?

- Do I have savings for a down payment?

- Am I eligible for government-backed loans?

- Do I prefer predictable payments or initial savings?

Use tools like mortgage calculators and speak with a licensed mortgage advisor to compare options.

📊 Mortgage Comparison Table

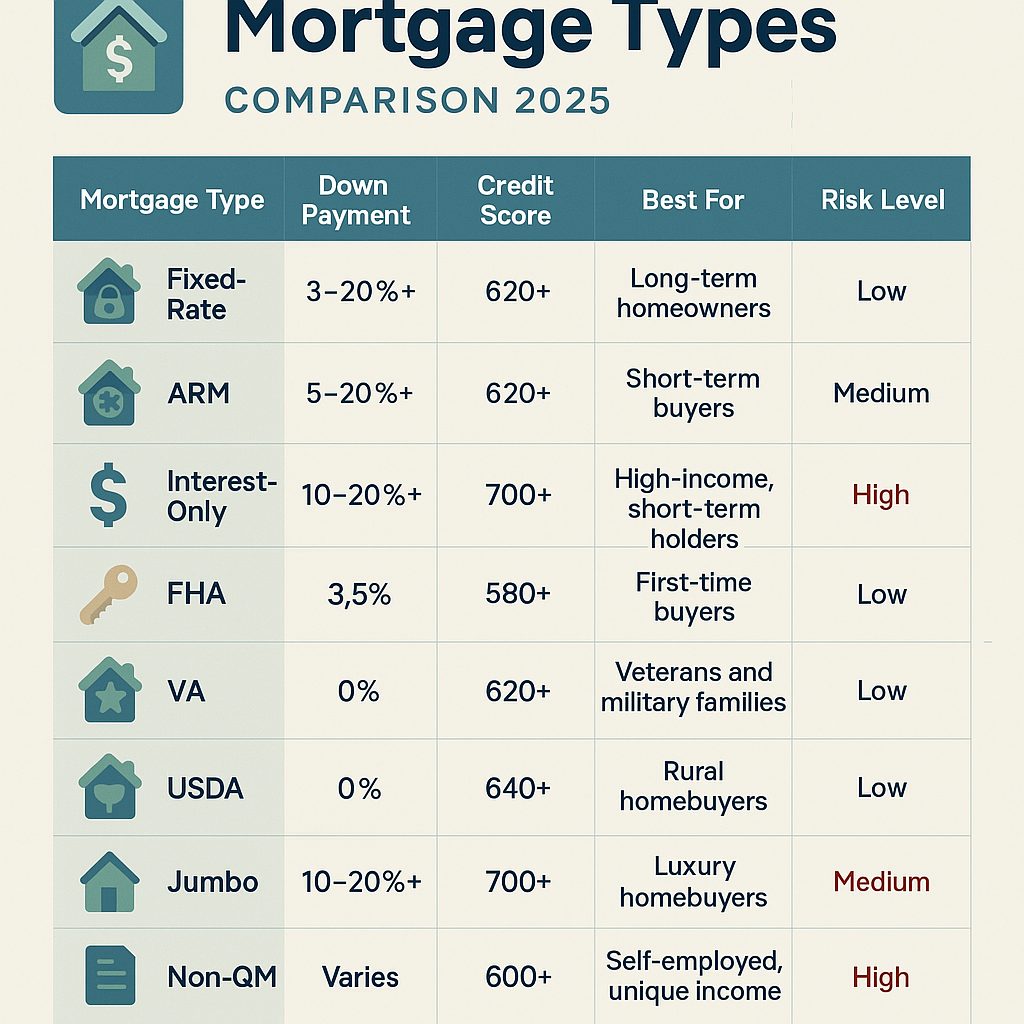

| Mortgage Type | Down Payment | Credit Score | Best For | Risk Level |

|---|---|---|---|---|

| Fixed-Rate | 3–20%+ | 620+ | Long-term homeowners | Low |

| ARM | 5–20%+ | 620+ | Short-term buyers | Medium |

| Interest-Only | 10–20%+ | 700+ | High-income, short-term holders | High |

| FHA | 3.5% | 580+ | First-time buyers | Low |

| VA | 0% | 620+ | Veterans and military families | Low |

| USDA | 0% | 640+ | Rural homebuyers | Low |

| Jumbo | 10–20%+ | 700+ | Luxury homebuyers | Medium |

| Non-QM | Varies | 600+ | Self-employed, unique income | High |

📣 Ready to Take the Next Step?

Whether you’re buying your first home or upgrading to your dream property, choosing the right mortgage is key 🔑. I’m here to help you navigate the process with confidence and clarity.

👉 Let’s talk about your mortgage goals today!

#realestate, #mortgage, #homebuying, #firsttimehomebuyer, #realestateinvesting, #mortgagetips, #homeownership, #realestategoals, #propertyinvestment, #househunting, #realtorlife, #financialfreedom, #realestatemarket, #dreamhome, #mortgagerates

Is Real Estate a Good Investment in 2025? Let’s Break It Down!

🏡 Is Real Estate a Good Investment in 2025? Let’s Break It Down!

Real estate has long been considered one of the most reliable paths to building wealth. But in 2025, with economic shifts, evolving technologies, and changing lifestyles, many are asking: Is real estate still a good investment? 🤔

The short answer? Yes—but with strategy. Let’s dive into the trends, opportunities, and challenges shaping the real estate landscape this year and help you decide if it’s the right move for you.

📈 The 2025 Real Estate Landscape: What’s New?

1. Interest Rates Are Stabilizing

After the aggressive rate hikes of 2023 and 2024, the Federal Reserve is signaling a more balanced approach in 2025. Mortgage rates, while still higher than pre-pandemic levels, are showing signs of stabilization

2. Demand for Rental Properties Is Soaring

With homeownership becoming less affordable for many, rental demand is booming. Millennials and Gen Z are prioritizing flexibility, and many are choosing to rent longer. This trend is especially strong in urban hubs and growing secondary cities.

3. Tech-Driven Real Estate Is on the Rise

From AI-powered property management to virtual tours and blockchain-based transactions, technology is transforming how we buy, sell, and manage real estate. Investors who embrace these tools can gain a competitive edge.

4. Sustainability Is a Must

Eco-conscious buyers and renters are driving demand for green buildings. Properties with energy-efficient features, solar panels, and sustainable materials are not only better for the planet 🌍 but also command higher rents and resale values.

🏘️ Top Real Estate Investment Trends in 2025

According to Forbes, here are some of the most impactful trends this year:

- Increased spending on both new and existing properties

- Diversification across property types and geographies

- A shift away from high-risk climate zones

- Rising demand for flexible, hybrid-friendly spaces

- Focus on resilience and disaster-proof construction

These trends suggest that investors are becoming more strategic and future-focused—a smart move in a dynamic market.

💡 Where Are the Opportunities?

1. Secondary Cities and Suburbs

Markets like Cincinnati, OH, Raleigh, NC, and Boise, ID are seeing strong growth. These areas offer lower entry costs, growing job markets, and high rental demand.

2. Build-to-Rent Communities

These purpose-built rental neighborhoods are gaining traction, especially among families who want the feel of a home without the mortgage.

3. Short-Term Rentals (STRs)

Despite regulatory hurdles in some cities, STRs remain profitable in tourist-heavy areas. Platforms like Airbnb and Vrbo continue to offer lucrative returns for well-managed properties.

4. Commercial Real Estate (CRE) Reimagined

While traditional office spaces are struggling, flex spaces, co-working hubs, and mixed-use developments are thriving. Investors are pivoting to meet the needs of a hybrid workforce.

⚠️ The Risks You Shouldn’t Ignore

No investment is without risk. Here are some to watch in 2025:

- Market Volatility: While more stable than recent years, the market is still sensitive to economic shifts.

- Climate Risk: Properties in flood-prone or wildfire-prone areas may face rising insurance costs or declining value.

- Regulatory Changes: Rent control laws, zoning changes, and STR regulations can impact profitability.

- Affordability Crisis: Skyrocketing home prices in some markets may limit appreciation potential.

Smart investors mitigate these risks by diversifying, doing thorough due diligence, and staying informed.

🧠 Real Estate Investment Strategies That Work in 2025

1. Buy and Hold

This classic strategy remains strong, especially in high-demand rental markets. Look for properties with solid cash flow and long-term appreciation potential.

2. House Hacking

Live in one unit of a multi-family property and rent out the others. It’s a great way to offset your mortgage and build equity.

3. REITs (Real Estate Investment Trusts)

Want exposure without the hassle of property management? REITs offer a hands-off way to invest in real estate through the stock market.

4. Fix and Flip

Still viable in 2025, especially in undervalued neighborhoods. Just be cautious of rising renovation costs and longer holding times.

📊 Real Estate vs. Other Investments in 2025

| Investment Type | Pros | Cons |

|---|---|---|

| Real Estate | Tangible asset, cash flow, tax benefits | Illiquid, management required |

| Stocks | High liquidity, passive | Volatile, no control |

| Crypto | High upside potential | Extremely volatile, speculative |

| Bonds | Stable, predictable | Low returns, inflation risk |

Real estate offers a balanced mix of income and appreciation, making it a strong contender for long-term wealth building.

🧭 Who Should Invest in Real Estate in 2025?

✅ You’re looking for passive income

✅ You want to hedge against inflation

✅ You’re ready to commit to a long-term strategy

✅ You’re comfortable with some level of risk and management

If that sounds like you, real estate could be your next big move.

📣 Ready to Start Your Real Estate Journey?

Whether you’re a first-time investor or looking to expand your portfolio, I’m here to help you navigate the 2025 market with confidence. Let’s talk about your goals, budget, and the best strategy for your situation.

👉 Contact Me Today for a Free Consultation!

Let’s turn your real estate dreams into reality! 🏠💼

🏁 Conclusion: Is Real Estate a Good Investment in 2025?

Absolutely—if you play it smart. The 2025 real estate market is full of opportunities, from booming rental demand to tech-driven efficiencies. But it also requires a strategic mindset, awareness of risks, and a willingness to adapt.

With the right approach, real estate remains one of the most powerful tools for building wealth in today’s economy.

🔖 Top Real Estate Hashtags for 2025

#realestate, #realestateinvesting, #propertyinvestment, #rentalproperty, #realestatetips, #investinrealestate, #realestate2025, #passiveincome, #financialfreedom, #househacking, #REITs, #buildtorent, #shorttermrentals, #realestatewealth, #propertymarket

📊 How to Read the Real Estate Market Like a Pro 🏡

📊 How to Read the Real Estate Market Like a Pro 🏡

Understanding the real estate market can feel like decoding a secret language. But with the right tools and insights, anyone can learn to read the market like a seasoned pro. Whether you’re a first-time homebuyer, an investor, or simply curious, this guide will walk you through the essential steps to mastering market analysis. Let’s dive in! 🔍

1. Know the Market Cycles 🔄

Real estate markets move in predictable cycles:

- Recovery: Prices are low, demand is slowly rising.

- Expansion: Construction increases, prices climb.

- Hyper-supply: Overbuilding occurs, demand slows.

- Recession: Prices drop, activity declines.

📌 Pro Tip: Identify your local market’s phase to time your buying or selling decisions strategically.

2. Analyze Supply and Demand 📈📉

High demand + low supply = rising prices.

Low demand + high supply = falling prices.

Track these indicators:

- Housing inventory

- Days on market

- New construction permits

🧠 Interactive Tip: Check your local MLS or Zillow to see how long homes are staying on the market in your area.

3. Track Interest Rates 💰

Interest rates directly affect mortgage affordability. Lower rates = more buyers = higher prices.

📊 Watch:

- Federal Reserve announcements

- Inflation trends

- Mortgage rate forecasts

💡 Did You Know? A 1% drop in interest rates can increase your buying power by up to 10%!

4. Study Local Economic Indicators 🏙️

A strong local economy = strong housing demand.

Look at:

- Job growth

- Population trends

- Median income levels

📍 Example: If a major employer is moving into town, expect a housing boom!

5. Compare Price Trends Over Time 📊

Use historical data to spot trends:

- Are prices rising steadily?

- Is there a seasonal pattern?

- Are there sudden spikes or drops?

🛠️ Tools: Zillow, Redfin, Realtor.com

📈 Try This: Plot home prices in your zip code over the last 5 years. What do you see?

6. Evaluate Rental Yields and Vacancy Rates 🏘️

For investors, rental yield = key metric.

- High yield + low vacancy = strong rental market

- Low yield + high vacancy = risky investment

📐 Formula:

Rental Yield = (Annual Rent / Property Price) × 100

🔍 Check: Local rent averages, tenant turnover, and occupancy rates.

7. Understand Government Policies and Incentives 🏛️

Policies can make or break a market:

- Tax incentives for buyers/investors

- Zoning changes

- Rent control laws

- First-time buyer programs

🧾 Stay Informed: Follow your city’s housing authority or planning department for updates.

8. Use Technology and Tools 🧠💻

Modern tools make market analysis easier than ever:

- PropStream: Investment analysis

- CoreLogic: Market trends

- Realtor.com: Neighborhood insights

- Mashvisor: Rental property data

🧭 Explore: Use heat maps to find hot neighborhoods!

9.Hire me to take care of all of this!